Materion’s Buyback and Fusion Deal Could Be a Game Changer for MTRN

- Materion Corporation recently reported third quarter 2025 results, showing year-over-year growth in both sales and net income, and announced a new US$50 million share repurchase program authorized by its Board of Directors.

- In addition, Commonwealth Fusion Systems announced an agreement for Materion to supply beryllium fluoride for use in fusion power plants, highlighting Materion’s entry into the expanding clean energy materials market.

- We’ll assess how Materion’s strong quarterly results and buyback initiative shape its investment narrative moving forward.

We've found 20 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Materion Investment Narrative Recap

To be a long-term Materion shareholder, you need to believe in the company's ability to capitalize on advanced materials demand in semiconductors, defense, and clean energy while navigating risks around customer concentration and commodity pricing. While the Q3 2025 results were solid, posting moderate sales and earnings growth, they do not significantly alter the most important short-term catalyst, which remains a recovery in global semiconductor and electronics demand, or the risk of potential market share losses in China from local competition.

Of the recent announcements, the US$50 million share repurchase program is most relevant as it reflects management’s confidence and supports shareholder returns. However, this move does not address the underlying risk of profit compression from sustained margin pressure, particularly as Materion’s exposure to price competition in Asian semiconductor markets remains a key factor for the business outlook.

In contrast, investors should also be mindful of ongoing risks tied to the company’s reliance on specialty metals and potential supply chain disruptions...

Read the full narrative on Materion (it's free!)

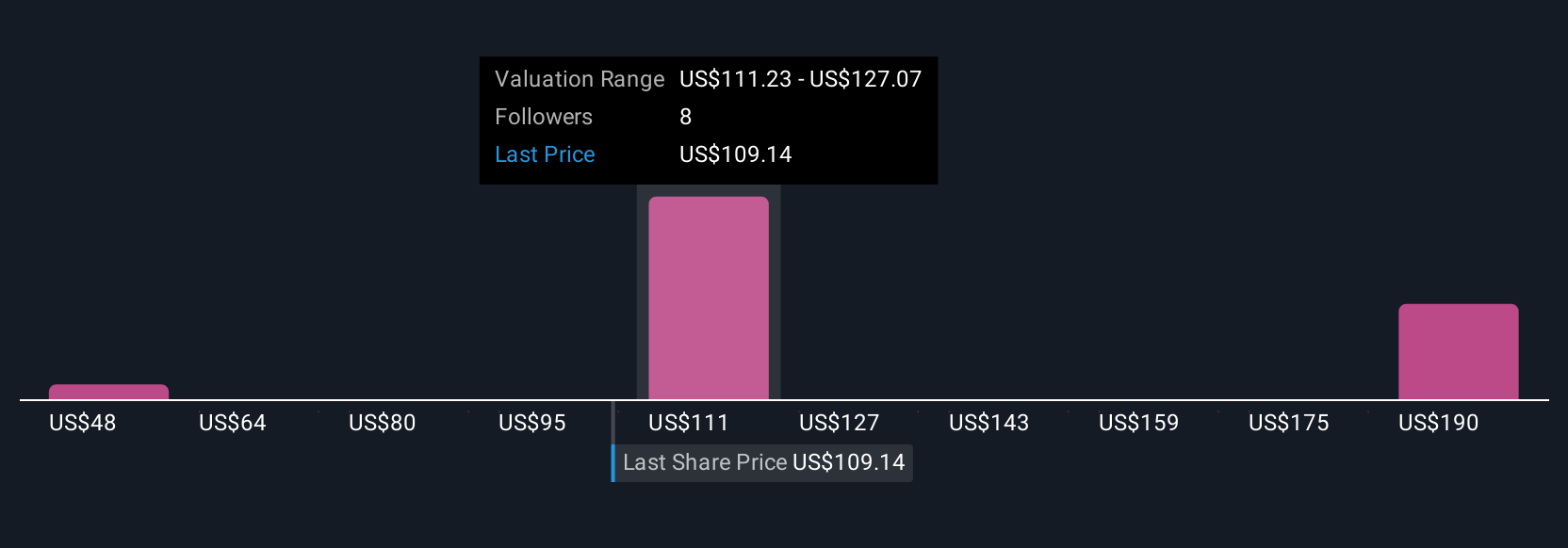

Materion's narrative projects $2.1 billion revenue and $355.2 million earnings by 2028. This requires 7.2% yearly revenue growth and a $338.9 million increase in earnings from $16.3 million today.

Uncover how Materion's forecasts yield a $143.67 fair value, a 24% upside to its current price.

Exploring Other Perspectives

Four individual fair value estimates from the Simply Wall St Community span a wide US$47.87 to US$179.48 range. Some see strong potential as global electronics demand emerges as a crucial theme, but you’ll find many alternate viewpoints to compare.

Explore 4 other fair value estimates on Materion - why the stock might be worth as much as 55% more than the current price!

Build Your Own Materion Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Materion research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Materion research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Materion's overall financial health at a glance.

Contemplating Other Strategies?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- These 12 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com