What Sunrun (RUN)'s Return to Profitability and Board Expansion Means For Shareholders

- On November 6, 2025, Sunrun Inc. reported strong third-quarter results, highlighted by substantial revenue growth to US$724.56 million and a return to profitability, and announced the appointment of Craig Cornelius as a new director, expanding the board to nine members.

- Mr. Cornelius brings over a decade of renewable energy leadership experience to Sunrun's board, including key executive roles in solar and storage at Clearway Energy and NRG, which may bolster the company's strategic direction in an evolving market.

- We'll explore how Sunrun's move to profitability and the addition of experienced board leadership influence the company's forward-looking investment case.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Sunrun Investment Narrative Recap

To own Sunrun, an investor needs conviction in the long-term growth of the residential solar and storage market and the company's ability to generate recurring revenues as regulatory support evolves. The recent board addition and return to profitability are positive developments, but do not materially alter the primary short-term catalyst, customer adoption of home energy solutions, nor do they reduce the ongoing exposure to regulatory and tax credit risks impacting near-term demand.

The latest earnings report, showing Sunrun's swing to a US$16.59 million profit in the third quarter and revenue climbing to US$724.56 million, stands out. This financial turnaround provides near-term confidence, yet the largest risk remains the policy-driven contraction in the addressable market as solar investment tax credits phase out after 2025.

However, investors should be aware that while recent results are promising, the potential sunset of key tax credits could leave Sunrun facing...

Read the full narrative on Sunrun (it's free!)

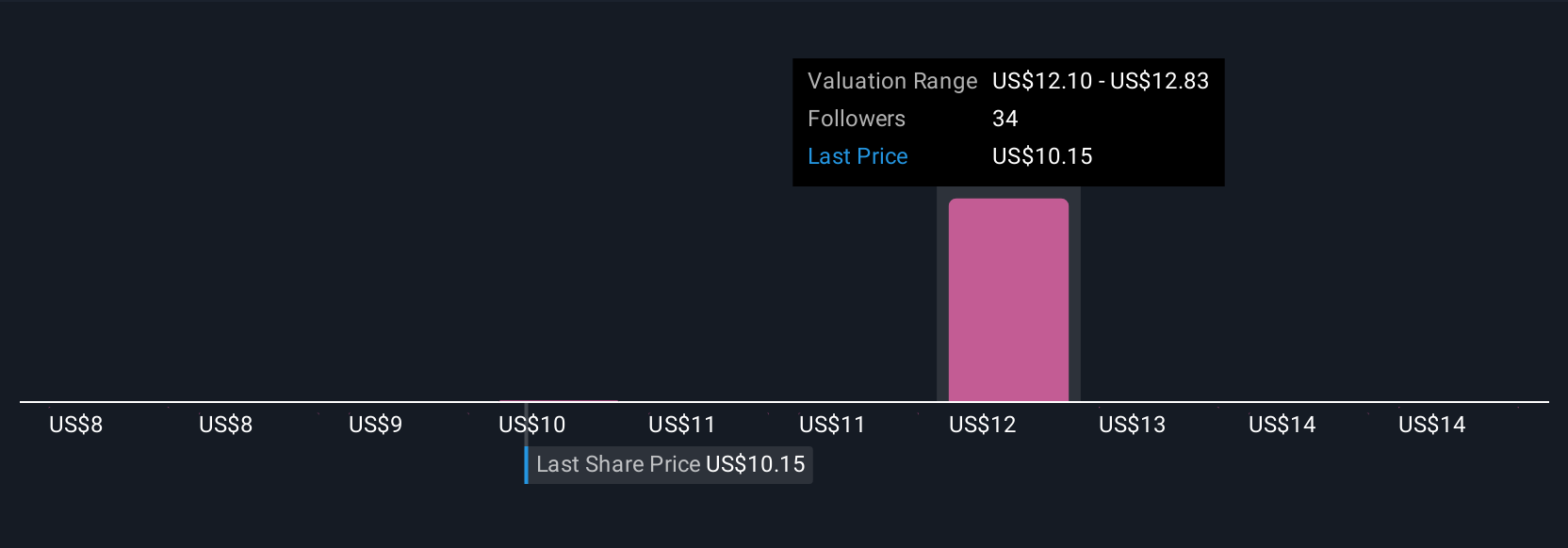

Sunrun's narrative projects $2.9 billion revenue and $465.4 million earnings by 2028. This requires 10.4% yearly revenue growth and an earnings increase of $3.07 billion from current earnings of $-2.6 billion.

Uncover how Sunrun's forecasts yield a $22.38 fair value, a 16% upside to its current price.

Exploring Other Perspectives

Five members of the Simply Wall St Community placed Sunrun’s fair value between US$13.14 and US$23.58 per share. Yet, with policy changes looming, the wide range of opinions reflects how views on risk and reward can significantly differ.

Explore 5 other fair value estimates on Sunrun - why the stock might be worth 32% less than the current price!

Build Your Own Sunrun Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Sunrun research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

- Our free Sunrun research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Sunrun's overall financial health at a glance.

Interested In Other Possibilities?

Our top stock finds are flying under the radar-for now. Get in early:

- Find companies with promising cash flow potential yet trading below their fair value.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

- These 11 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com