Assessing Wabtec’s Valuation After Rail Contracts and a 5.6% Weekly Price Dip

- Wondering if Westinghouse Air Brake Technologies is worth a closer look? Many investors are asking the same question as they consider the stock's current price and long-term prospects.

- The share price has dipped 5.6% in the past week but managed a modest 4.7% gain year-to-date, adding to impressive returns of 101.2% over three years and 174.8% in the past five years.

- Recent headlines have focused on the company's continued push into rail technology innovations, including securing notable contracts for modernizing freight locomotives and expanding its digital services. These moves have caught the attention of analysts and frame recent price swings in the context of fresh growth opportunities and evolving market sentiment.

- Currently, Westinghouse Air Brake Technologies has a valuation score of 2 out of 6, showing there is more to dig into around the stock's value. Next, we will break down several valuation approaches to see how the numbers add up, then explore an even more insightful way to judge what Wabtec might really be worth.

Westinghouse Air Brake Technologies scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Westinghouse Air Brake Technologies Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates a company's intrinsic value by projecting future cash flows and discounting them back to present value. This approach attempts to calculate what all of the company’s incoming cash flows in the years ahead are worth in today’s dollars.

For Westinghouse Air Brake Technologies, the latest reported Free Cash Flow stands at $1.28 billion. Analyst estimates suggest this figure will continue to grow, reaching approximately $1.87 billion by the end of 2027. Looking even further ahead, extended projections forecast Free Cash Flow rising to over $2.66 billion by 2035, although these longer-term numbers rely on systematic estimates beyond what analysts have officially published.

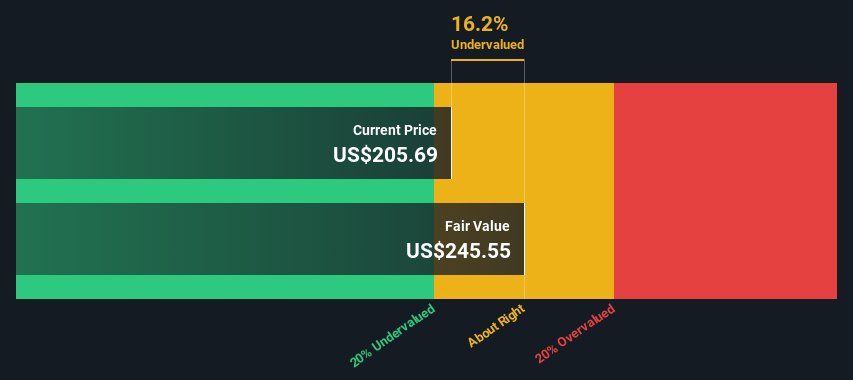

Based on these projections and using a 2 Stage Free Cash Flow to Equity model, the fair value per share is estimated at $211.21. With the current trading price sitting about 6.3% below this value, the stock is considered to be very close to its intrinsic value. While there appears to be some room for upside, the difference is not dramatic.

Result: ABOUT RIGHT

Westinghouse Air Brake Technologies is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

Approach 2: Westinghouse Air Brake Technologies Price vs Earnings

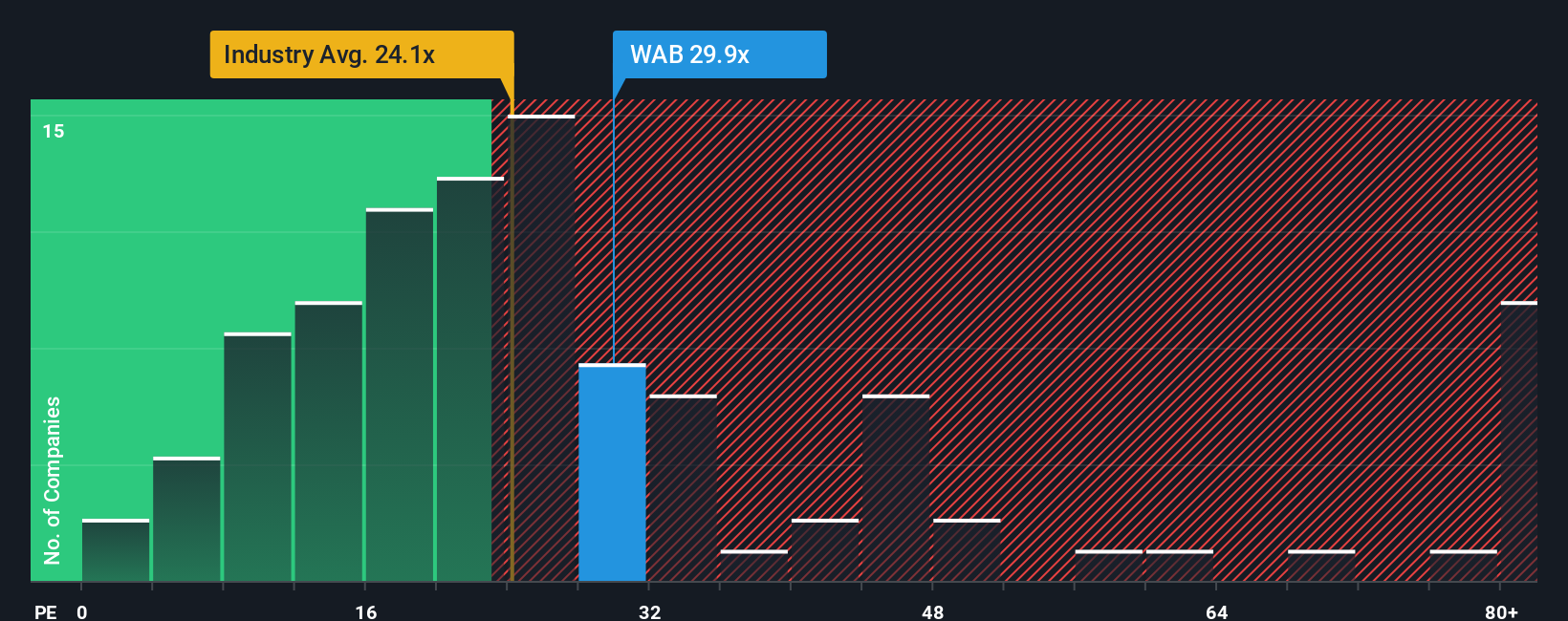

For companies like Westinghouse Air Brake Technologies that consistently generate profits, the Price-to-Earnings (PE) ratio is a go-to valuation method. It’s straightforward: the PE ratio tells investors how much they’re paying for each dollar of earnings. Growth prospects and business risks shape what a “normal” PE should look like. A company with high expected growth or lower risk typically deserves a higher PE, while slower or riskier firms sit at the lower end.

Currently, Westinghouse Air Brake Technologies is trading at a PE ratio of 28.77x. This is notably higher than both the average for machinery industry peers at 16.14x and the broader industry average of 23.26x. On first glance, that might seem expensive, but context is key.

Enter Simply Wall St’s Fair Ratio, an assessment that goes beyond basic comparison by factoring in elements like the company’s future earnings growth, profit margins, risk profile, industry trends, and market cap. This approach is more nuanced, helping investors judge value more accurately than looking at broad averages, which may not capture the whole story.

For Westinghouse Air Brake Technologies, the Fair Ratio is 29.90x. That is extremely close to the current PE of 28.77x, signaling the stock is priced about where it should be given its unique growth and risk profile.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1416 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Westinghouse Air Brake Technologies Narrative

Earlier, we mentioned there is an even better way to understand valuation, so let’s introduce you to Narratives. A Narrative is a simple yet powerful tool that lets you put your own story behind the numbers. It connects your perspective on a company’s future growth, margins, and fair value to a dynamic financial forecast.

With Narratives, investors can move beyond static ratios and models. You outline your expectations for Westinghouse Air Brake Technologies, turning industry changes, company-specific strengths, and risks into actionable insights. Narratives link the company’s story, such as new locomotive contracts, digital service expansion, or exposure to international markets, directly to the financial numbers. This helps you estimate a fair value and see how it compares to today’s price.

Millions of investors use Narratives on Simply Wall St’s Community page, where each one is updated automatically when key news or earnings arrive, ensuring your valuation reflects the most current conditions. They are accessible, easy to use, and enable smarter investment decisions by comparing your Fair Value to the live market Price.

For example, one investor’s bullish Narrative could highlight booming international demand and set a Fair Value of $250 per share, while a more cautious peer might emphasize North American headwinds and land at $200. Your own Narrative helps you make decisions that fit your unique view.

Do you think there's more to the story for Westinghouse Air Brake Technologies? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com