Is Public Service Enterprise Group’s (PEG) Dividend Hike Signaling Confidence in Its Long-Term Investment Plan?

- On November 18, 2025, Public Service Enterprise Group’s Board of Directors declared a US$0.63 per share dividend for the fourth quarter of 2025, with payment scheduled on or before December 31, 2025 to shareholders of record as of December 10.

- The dividend affirmation accompanied quarterly results that surpassed expectations, supported by new electric and gas base rate increases and a reaffirmed long-term growth outlook underpinned by a multi-billion dollar capital investment program.

- We’ll explore how the reaffirmed earnings growth outlook and continued capital investments shape Public Service Enterprise Group’s investment narrative.

Rare earth metals are the new gold rush. Find out which 36 stocks are leading the charge.

Public Service Enterprise Group Investment Narrative Recap

If you believe in stable regulated utilities with multi-decade infrastructure growth, Public Service Enterprise Group’s story hinges on converting new large-load inquiries into future revenue while balancing heavy capital commitments. The recent dividend affirmation supports income-focused strategies but does not materially move the dial on the all-important risk: whether data center pipeline conversion rates will be high enough to sustain robust long-term earnings growth.

Of the recent company announcements, the Board’s move earlier this year to increase the quarterly dividend by $0.03 per share aligns closely with the current dividend update and underscores their ongoing commitment to shareholder returns. With sustained dividend payouts amid rising base rates, the short-term catalyst remains regulatory cost recovery on those investments, but investors should remain mindful that ...

Read the full narrative on Public Service Enterprise Group (it's free!)

Public Service Enterprise Group is projected to reach $12.4 billion in revenue and $2.5 billion in earnings by 2028. This outlook assumes a 3.5% annual revenue growth rate and a $0.5 billion increase in earnings from the current level of $2.0 billion.

Uncover how Public Service Enterprise Group's forecasts yield a $90.61 fair value, a 10% upside to its current price.

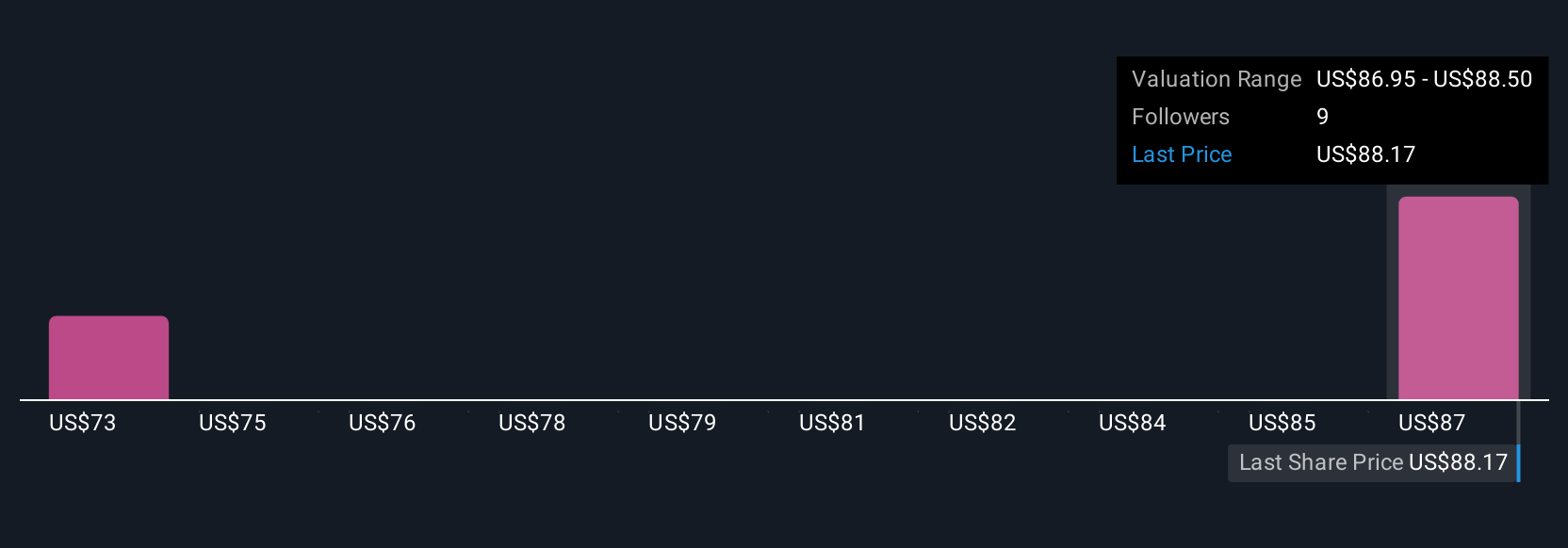

Exploring Other Perspectives

Three Simply Wall St Community member valuations for PSEG range from US$73.03 to US$90.61 per share. While individuals see varied value potential, ongoing revenue growth is still tethered to customer conversion rates for new data center load inquiries, which could influence long-term outlooks quite differently.

Explore 3 other fair value estimates on Public Service Enterprise Group - why the stock might be worth as much as 10% more than the current price!

Build Your Own Public Service Enterprise Group Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Public Service Enterprise Group research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Public Service Enterprise Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Public Service Enterprise Group's overall financial health at a glance.

Searching For A Fresh Perspective?

Our top stock finds are flying under the radar-for now. Get in early:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 26 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- These 12 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com