Why HCA Healthcare (HCA) Is Up 7.0% After ACA Subsidy Optimism and Expansion Moves

- HCA Healthcare recently presented at the Stephens Annual Investment Conference in Nashville, while expanding with new facilities and leadership appointments across Florida and Texas.

- Investor optimism toward HCA Healthcare has grown following reports that the Trump administration may extend Affordable Care Act subsidies, reducing policy uncertainty for the sector.

- We’ll explore how potential stability in ACA policies could reshape HCA Healthcare’s investment outlook and longer-term risk profile.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

HCA Healthcare Investment Narrative Recap

At the core, HCA Healthcare shareholders need to believe in consistent healthcare demand and the company’s ability to efficiently expand capacity while managing costs. The recent shift in policy sentiment, given news of the potential ACA subsidy extension, addresses the sector’s primary near-term catalyst by reducing federal regulatory uncertainty. However, larger risks such as fluctuating professional fee costs and supply chain expenses remain prominent and are unaffected by these specific policy developments.

Among the company's latest announcements, HCA Florida’s plan to open a new hospital in Gainesville stands out. This expansion fits squarely with ongoing regional healthcare demand and could support near-term volume growth, which is a key catalyst when regulatory stability is in focus for investors.

By contrast, investors should be aware that continued increases in professional fee expenses could still pressure HCA’s margins unless...

Read the full narrative on HCA Healthcare (it's free!)

HCA Healthcare's narrative projects $85.4 billion in revenue and $6.9 billion in earnings by 2028. This requires 5.5% yearly revenue growth and a $0.9 billion earnings increase from the current $6.0 billion level.

Uncover how HCA Healthcare's forecasts yield a $477.70 fair value, a 7% downside to its current price.

Exploring Other Perspectives

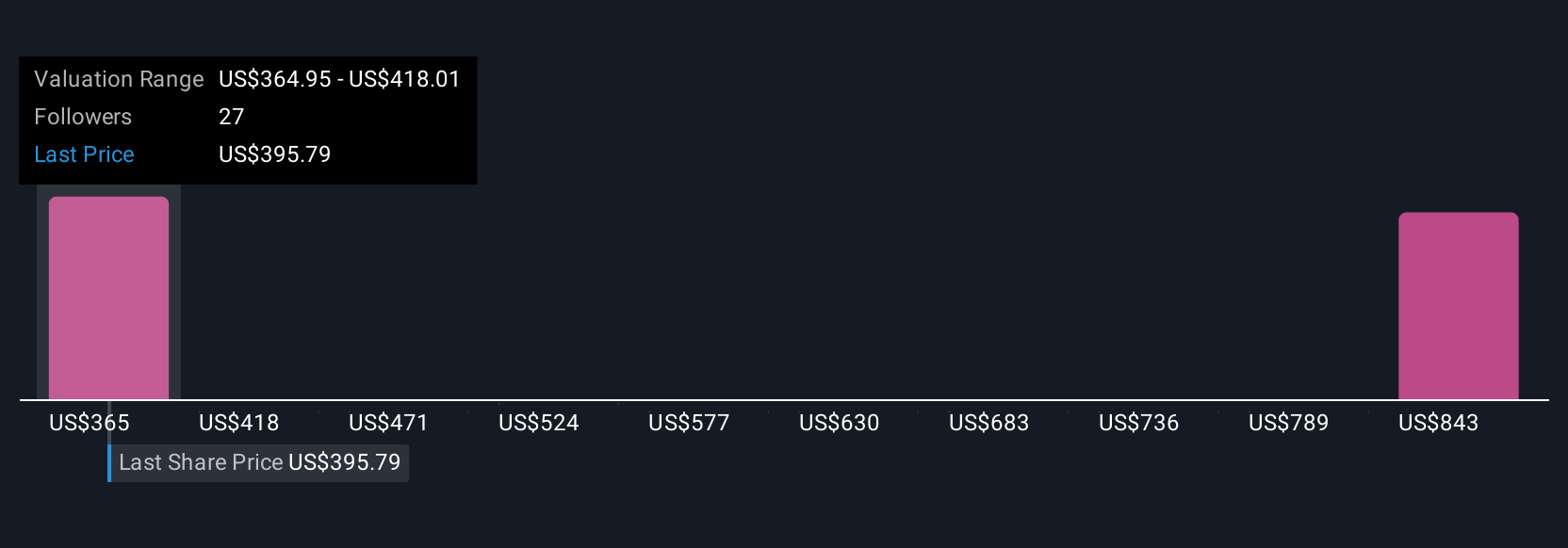

Five Simply Wall St Community fair value estimates for HCA Healthcare range widely from US$369.18 to US$899.69. While opinions differ, regulatory uncertainty remains a central concern that could affect revenue consistency and future outlooks.

Explore 5 other fair value estimates on HCA Healthcare - why the stock might be worth as much as 75% more than the current price!

Build Your Own HCA Healthcare Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your HCA Healthcare research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free HCA Healthcare research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate HCA Healthcare's overall financial health at a glance.

Seeking Other Investments?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- These 12 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 25 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com