Is Entergy’s Share Price Justified After Grid Modernization News and 28% Rally in 2025?

- If you have ever wondered whether Entergy stock is really worth its current price tag, you are not alone. There are plenty of reasons to dig into its true value right now.

- Entergy’s share price has moved up 3.0% in the last week and is up 28.1% year-to-date, suggesting shifting investor optimism and possible growth re-rating.

- There has also been increased talk about Entergy’s role in the U.S. energy grid after it announced new grid modernization projects and secured regulatory approvals for transmission expansions, making headlines in the utility industry and likely fueling recent investor interest.

- But how does Entergy stack up on valuation? At last check, it scored 0 out of 6 on our valuation checklist, so let’s unpack what this means. Stick around for a perspective on valuation that goes beyond just the usual methods.

Entergy scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Entergy Dividend Discount Model (DDM) Analysis

The Dividend Discount Model, or DDM, is used to estimate a company’s true worth by projecting future dividend payments and discounting them back to today’s value. This method is particularly useful for established companies with reliable dividend histories, such as Entergy.

For Entergy, recent data show an annual dividend per share (DPS) of $2.70, with a payout ratio of 61.3%. The company reports a return on equity (ROE) of 11.16%, and future dividend growth is currently capped at 3.26%, based on both historical patterns and analysts’ expectations. This indicates a moderate and steady rate of dividend growth anticipated over time.

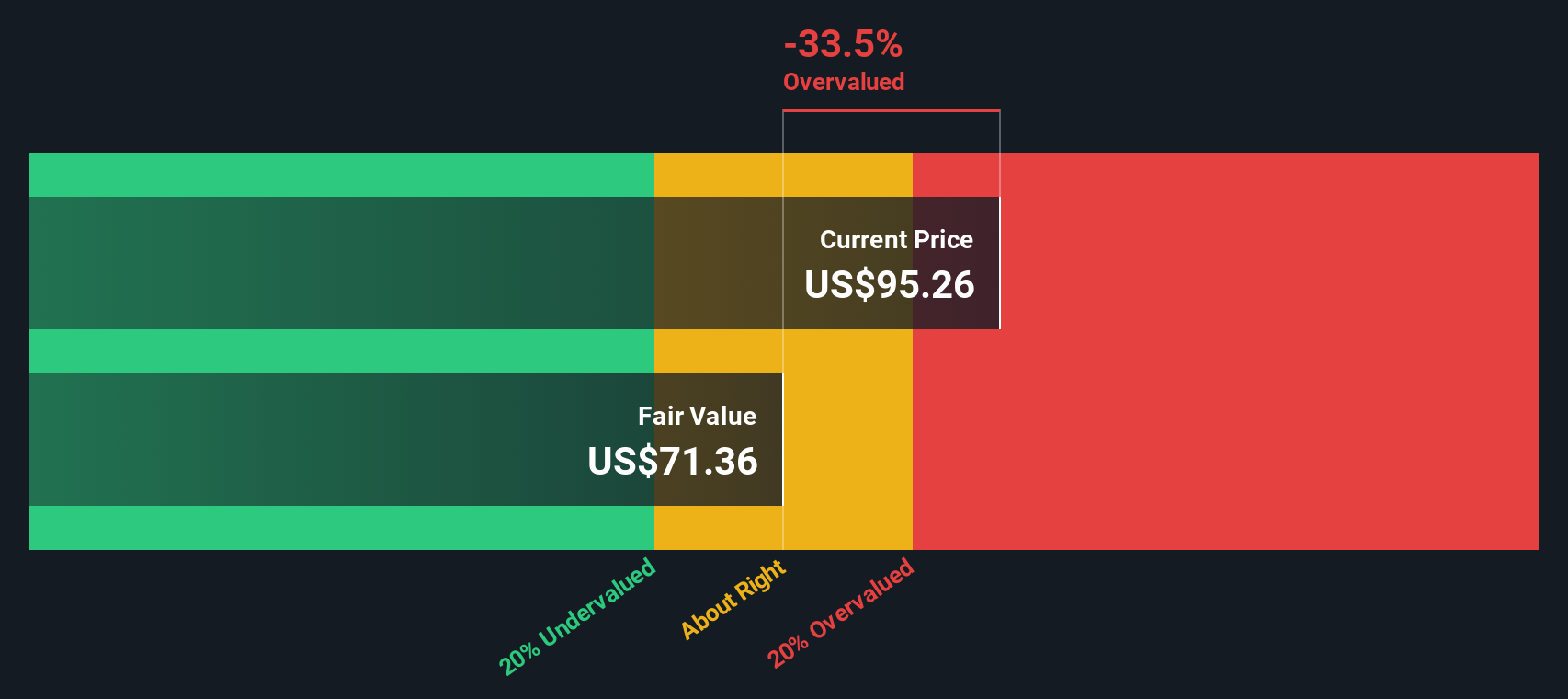

Applying the DDM, Simply Wall St calculates Entergy’s fair value at $73.18 per share. However, with the current share price trading significantly above this level, the model indicates the stock is approximately 31.9% overvalued. This suggests investors may be paying a premium based on projections that already reflect ambitious dividend growth assumptions.

If your priority is sustainable income and stable growth, the numbers suggest caution at these levels.

Result: OVERVALUED

Our Dividend Discount Model (DDM) analysis suggests Entergy may be overvalued by 31.9%. Discover 923 undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Entergy Price vs Earnings

The Price-to-Earnings (PE) ratio is a widely used valuation tool for established, profitable companies like Entergy. It reflects how much investors are willing to pay today for each dollar of earnings generated by the business. The PE ratio is particularly insightful for companies with steady profits, as it helps compare earnings power against both sector peers and the broader market.

However, what qualifies as a “fair” PE ratio depends on more than just past performance. Growth prospects and risk levels play a crucial role. Companies anticipating faster earnings growth or perceived as lower risk typically command higher PE ratios. In contrast, those facing uncertainty or slower growth trade at lower multiples.

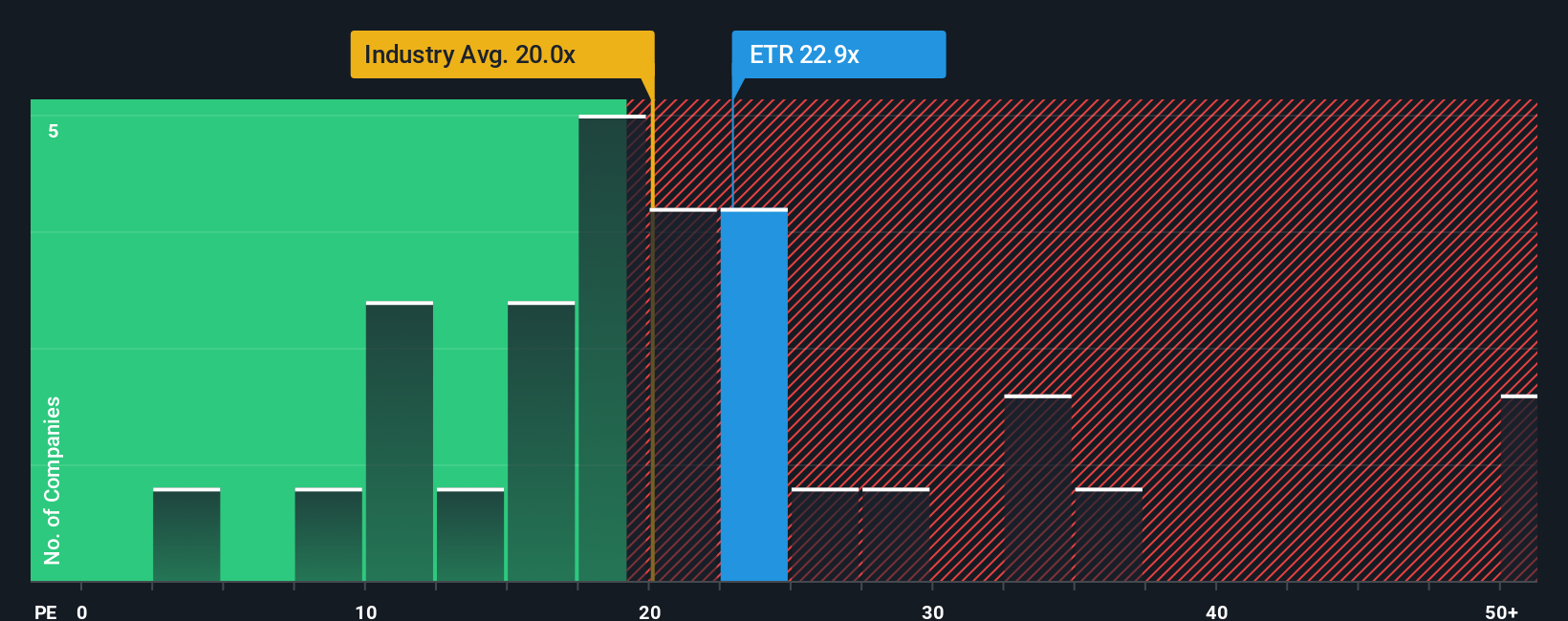

Currently, Entergy trades at a PE ratio of 24.1x. This is above the Electric Utilities industry average of 20.9x and also higher than the average among similar peers, which sits at 19.7x. Importantly, Simply Wall St calculates a proprietary “Fair Ratio” of 23.9x for Entergy, factoring in not only the company’s growth forecasts and profit margins, but also sector dynamics and its overall risk profile. This makes the Fair Ratio a more holistic benchmark than comparing strictly with peers or industry averages, as those can overlook the nuance of company-specific growth and risk conditions.

Comparing Entergy’s actual PE with its Fair Ratio shows virtually no difference. This suggests the shares are priced about right relative to what investors might reasonably expect given the company’s circumstances.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1439 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Entergy Narrative

Earlier, we mentioned that there is an even better way to understand valuation, so let’s introduce you to Narratives. Narratives are Simply Wall St’s innovative tool that lets you tell the story behind the numbers by combining your own fair value, assumptions of future revenue, earnings, and margins into a clear investment “story.” In simple terms, a Narrative links your view of Entergy’s business, whether you see it thriving thanks to strong demand for corporate energy or challenged by regulatory risks, to dynamic forecasts and a resulting fair value estimate.

Within Simply Wall St’s Community page, millions of investors use Narratives to easily organize their thinking, compare perspectives, and make transparent, real-time decisions as new information arrives. Instead of relying solely on static valuation models, Narratives help you decide when to buy or sell by showing how your fair value compares to the current market price and update instantly as news or earnings are released.

For example, some Entergy investors believe robust long-term demand justifies a fair value as high as $109 per share, while others see more risk and place it closer to $67. Narratives let you capture your unique perspective, sense-check it against the consensus, and invest with confidence based on your own story.

Do you think there's more to the story for Entergy? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com