How UGI’s (UGI) Strong Earnings and Capital Returns May Shape Investor Sentiment

- In the past week, UGI Corporation reported fourth-quarter earnings that surpassed analyst expectations, alongside recently affirming its quarterly dividend and completing a share repurchase program totaling 4,650,000 shares for US$194.64 million. Operational improvements at AmeriGas and the commissioning of a new LNG facility in Pennsylvania were also highlighted, while the company's President of a subsidiary sold 15,000 shares.

- These developments underscore UGI's ongoing focus on infrastructure upgrades, proactive balance sheet management, and maintaining shareholder returns despite ongoing challenges in revenue and evolving energy markets.

- We'll examine how UGI's combination of better-than-expected earnings and sustained capital returns may influence its future investment outlook.

We've found 14 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

UGI Investment Narrative Recap

To be a UGI shareholder, you need to believe that the company can successfully balance infrastructure investment and operational efficiency programs against ongoing demand declines in its traditional LPG and propane markets. The recent quarter’s improved net loss and active capital return policies are supportive in the near term, but they do not fundamentally change the challenge of structural volume declines or regulatory risk. The main short-term catalyst remains regulatory approval for higher Pennsylvania utility rates, while secular demand erosion in Europe and AmeriGas is the biggest risk; the news flow this week does not materially alter these dynamics.

Among recent announcements, UGI’s affirmation of its quarterly dividend at US$0.375 per share is especially relevant as it reinforces the company’s historical commitment to shareholder returns, even in the face of margin and volume pressures. This regular payout, now sustained for 141 consecutive years, ties closely to management’s ongoing efforts to reassure investors and support the stock during periods of transition, especially as future performance hinges on the outcome of planned infrastructure upgrades and regulatory decisions.

However, in contrast, one factor investors should be aware of is that despite these reassuring dividend affirmations, persistent structural demand declines in core markets could...

Read the full narrative on UGI (it's free!)

UGI's narrative projects $9.0 billion revenue and $794.3 million earnings by 2028. This requires 7.0% yearly revenue growth and a $376.3 million earnings increase from $418.0 million today.

Uncover how UGI's forecasts yield a $43.00 fair value, a 9% upside to its current price.

Exploring Other Perspectives

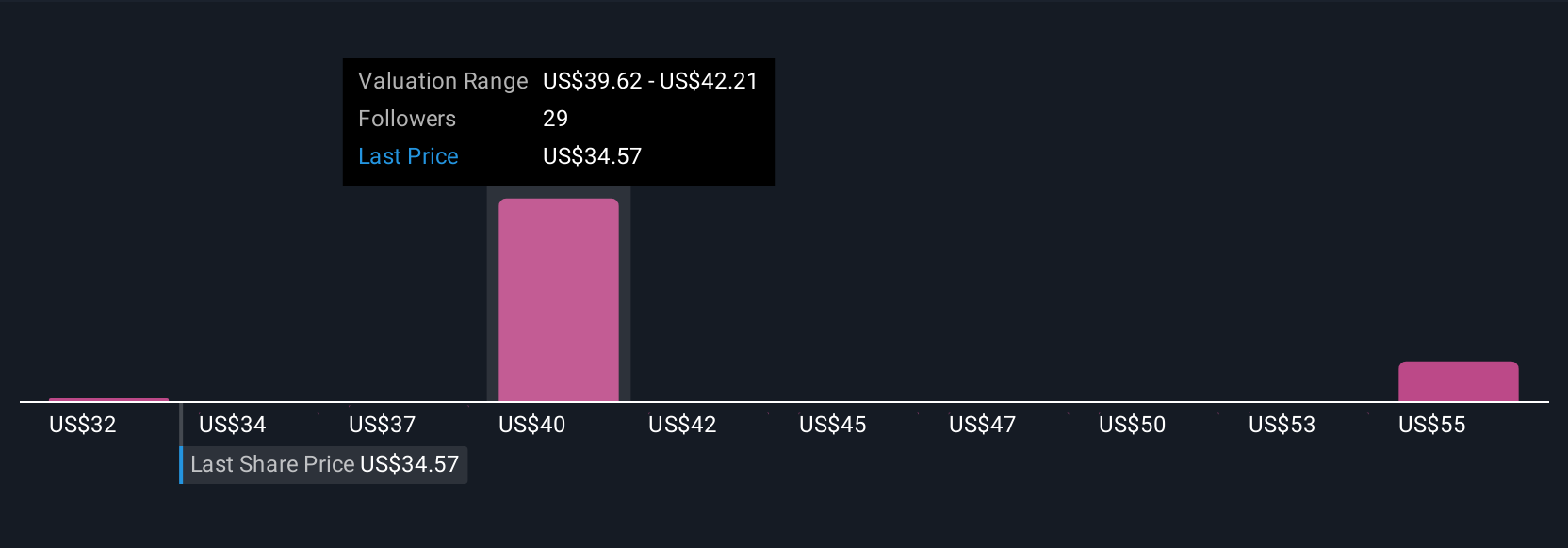

Simply Wall St Community members estimate UGI’s fair value range widely between US$31.87 and US$54.99, with five recent independent analyses. As you consider these varied opinions, remember that ongoing customer attrition at AmeriGas may affect the company’s ability to meet future growth expectations.

Explore 5 other fair value estimates on UGI - why the stock might be worth 19% less than the current price!

Build Your Own UGI Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your UGI research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

- Our free UGI research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate UGI's overall financial health at a glance.

Contemplating Other Strategies?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- These 11 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com