Over the last 7 days, the United States market has remained flat, yet it is up 29% over the past year with earnings expected to grow by 16% per annum in the coming years. In this environment, identifying stocks that are perceived as undervalued can be particularly appealing, especially when there is insider buying activity signaling potential confidence from those within the company.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| FirstSun Capital Bancorp | 10.9x | 2.6x | 43.38% | ★★★★★★ |

| Financial Institutions | 8.9x | 2.9x | 48.23% | ★★★★★☆ |

| Ribbon Communications | 11.5x | 0.5x | 45.40% | ★★★★★☆ |

| New Peoples Bankshares | 9.4x | 2.2x | 25.75% | ★★★★☆☆ |

| 1st Source | 11.2x | 4.2x | 41.33% | ★★★★☆☆ |

| Aldeyra Therapeutics | NA | NA | 48.36% | ★★★★☆☆ |

| Metropolitan Bank Holding | 13.1x | 3.7x | 40.69% | ★★★☆☆☆ |

| German American Bancorp | 12.0x | 4.4x | 46.04% | ★★★☆☆☆ |

| Eagle Financial Services | 10.9x | 2.6x | 30.75% | ★★★☆☆☆ |

| CEVA | NA | 6.3x | -47.19% | ★★★☆☆☆ |

Here's a peek at a few of the choices from the screener.

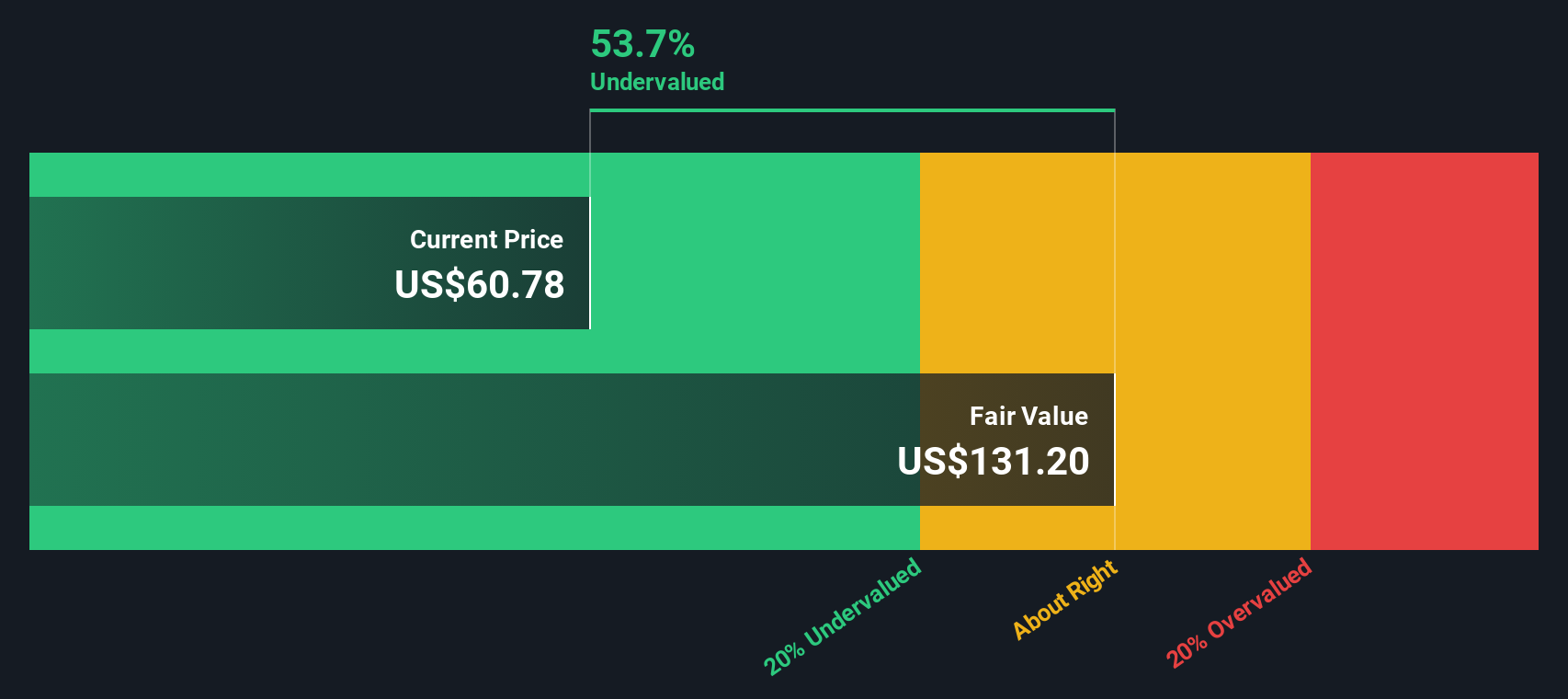

1st Source (SRCE)

Simply Wall St Value Rating: ★★★★☆☆

Overview: 1st Source is a financial institution primarily engaged in commercial banking, with operations focused on providing a range of financial services, and it has a market capitalization of approximately $1.39 billion.

Operations: Revenue primarily comes from commercial banking, with a recent figure of $426.31 million. Operating expenses are significant, with general and administrative expenses accounting for a substantial portion at $189.19 million. The net income margin has shown an upward trend, reaching 37.35% in the latest period.

PE: 11.2x

Insider confidence in 1st Source is evident with recent share purchases, reflecting trust in its potential. Between January and March 2026, the company repurchased 338,356 shares for US$23.14 million, completing a buyback of 571,389 shares. In Q1 2026, net interest income rose to US$90.14 million from US$80.94 million a year ago, while net income increased to US$39.96 million from US$37.52 million—a promising sign amidst broader market challenges for small companies like this one.

- Click here to discover the nuances of 1st Source with our detailed analytical valuation report.

Gain insights into 1st Source's past trends and performance with our Past report.

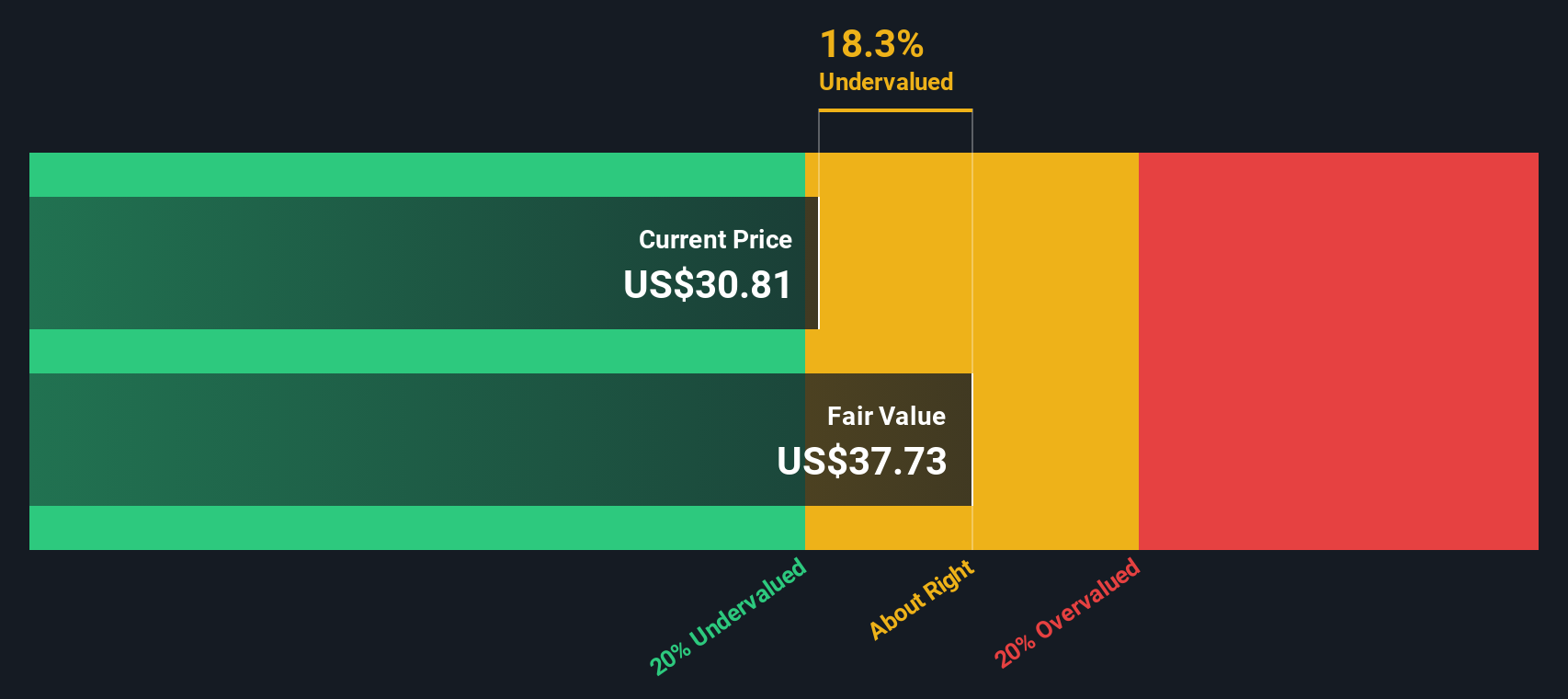

Washington Trust Bancorp (WASH)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Washington Trust Bancorp is a financial holding company that provides a range of banking and wealth management services, with a market cap of approximately $0.68 billion.

Operations: The company's revenue model is characterized by consistent gross profit margins of 100% over the observed periods. Operating expenses, primarily driven by general and administrative costs, have shown a gradual increase, impacting net income margins which have fluctuated between 24.80% and 35.76%.

PE: 11.6x

Washington Trust Bancorp, a small cap financial institution, recently announced the appointment of Jeffrey M. Wilhelm to its board, bringing over 25 years of digital transformation expertise. First-quarter results showed net interest income rising to US$40.53 million from US$36.42 million a year ago, with net income at US$12.6 million compared to US$12.18 million previously. Insider confidence is evident with recent share purchases by executives, indicating positive sentiment towards future growth prospects in the banking sector.

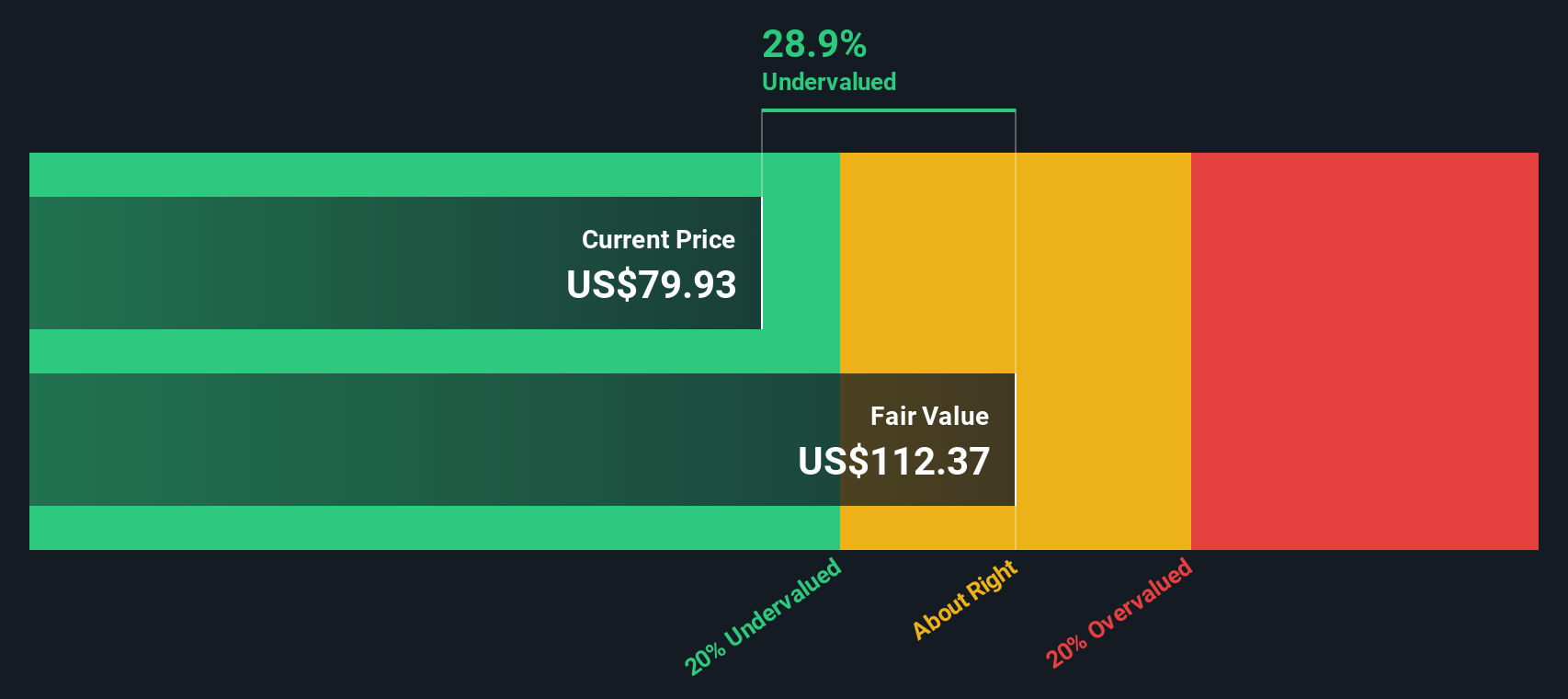

Metropolitan Bank Holding (MCB)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Metropolitan Bank Holding operates as a commercial bank providing a range of banking products and services, with a market cap of approximately $0.56 billion.

Operations: MCB generates revenue primarily from its banking segment, with the latest reported revenue at $302.22 million. The company consistently reports a gross profit margin of 100%, indicating no cost of goods sold data is available or applicable. Operating expenses, including general and administrative costs, significantly impact net income margins, which have shown fluctuations over time but recently stood at 28.51%.

PE: 13.1x

Metropolitan Bank Holding recently showcased strong financial performance, with net interest income rising to US$85.91 million in Q1 2026 from US$66.95 million a year earlier, and net income nearly doubling to US$31.43 million. The company increased its quarterly dividend by $0.05 to $0.25 per share, reflecting confidence in future growth prospects as earnings are forecasted to grow 24% annually. Insider confidence is evident through recent insider purchases, highlighting potential value recognition within this small-cap entity’s stock dynamics.

Make It Happen

- Reveal the 62 hidden gems among our Undervalued US Small Caps With Insider Buying screener with a single click here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com