- In late April 2026, Element Solutions Inc reported first-quarter 2026 results showing sales rising to US$840 million from US$593.7 million a year earlier, while net income fell to US$55.9 million from US$98 million and diluted EPS from continuing operations decreased to US$0.23 from US$0.40.

- The quarter was marked by double-digit organic growth in the Electronics segment, strong contributions from the newly acquired Micromax and EFC businesses, and a higher full-year adjusted EBITDA guidance underpinned by demand related to AI infrastructure and high-performance electronics.

- We’ll now examine how the raised full-year adjusted EBITDA guidance and electronics-driven growth could influence Element Solutions’ existing investment narrative.

Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

Element Solutions Investment Narrative Recap

To own Element Solutions, you need to believe that its push into higher value electronics materials, especially for AI infrastructure and data centers, can offset cyclicality and pricing pressure in more traditional end markets. The latest quarter supports that electronics-driven growth story and the raised full-year adjusted EBITDA guidance reinforces the near term catalyst, while the biggest immediate risk remains earnings volatility from cyclical electronics demand and higher leverage after recent acquisitions.

The most relevant development here is the April 2026 guidance increase to US$665 million to US$685 million in adjusted EBITDA for 2026, tied to strong electronics demand and contributions from Micromax and EFC. This directly connects to the thesis that portfolio shifts toward high growth electronics and advanced materials can support better margins and more resilient earnings, while also testing how well the company can manage acquisition related integration and debt in a softer industrial backdrop.

Yet investors should also keep in mind the increased balance sheet risk associated with funding these acquisitions...

Read the full narrative on Element Solutions (it's free!)

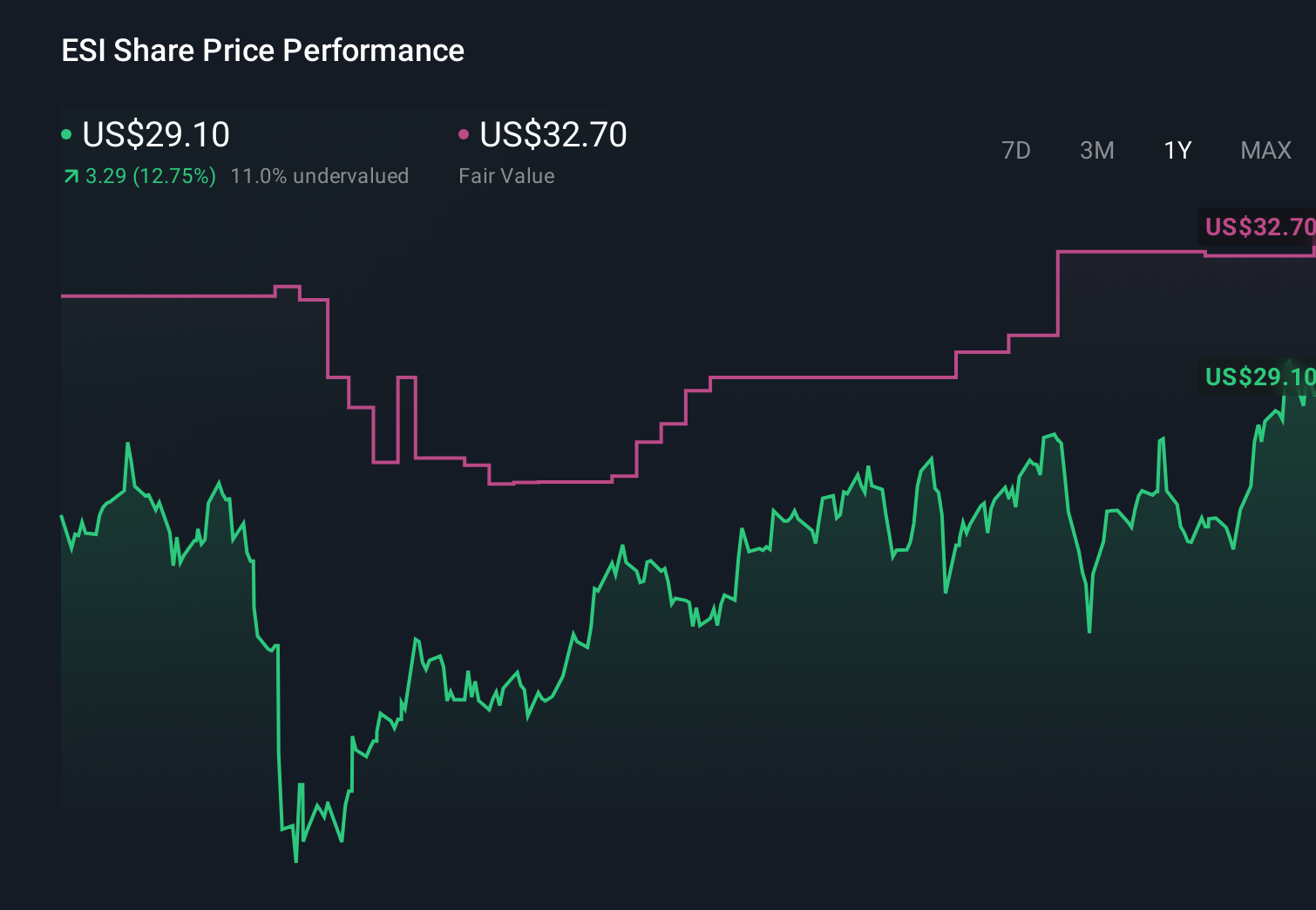

Element Solutions' narrative projects $3.4 billion revenue and $399.8 million earnings by 2029. This requires 10.2% yearly revenue growth and about a $209 million earnings increase from $190.8 million today.

Uncover how Element Solutions' forecasts yield a $40.10 fair value, a 7% downside to its current price.

Exploring Other Perspectives

Simply Wall St Community members currently see fair value for Element Solutions between US$38.04 and US$40.10 across 2 individual models. Against this backdrop, the company’s dependence on cyclical electronics demand could have a significant impact on how those expectations play out over time, so it is worth exploring several contrasting viewpoints before forming your own view.

Explore 2 other fair value estimates on Element Solutions - why the stock might be worth 12% less than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Element Solutions research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

- Our free Element Solutions research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Element Solutions' overall financial health at a glance.

Ready For A Different Approach?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Find 51 companies with promising cash flow potential yet trading below their fair value.

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com