- PJT Partners Inc. recently reported first-quarter 2026 results, with net income rising to US$60.5 million and diluted earnings per share from continuing operations increasing to US$2.21, while also affirming a quarterly dividend of US$0.25 per share and completing a multi-year buyback tranche of 3,742,763 shares.

- Alongside these results, the Board authorized a fresh share repurchase program of up to US$800 million, signaling continued emphasis on returning capital to shareholders through both buybacks and ongoing dividends.

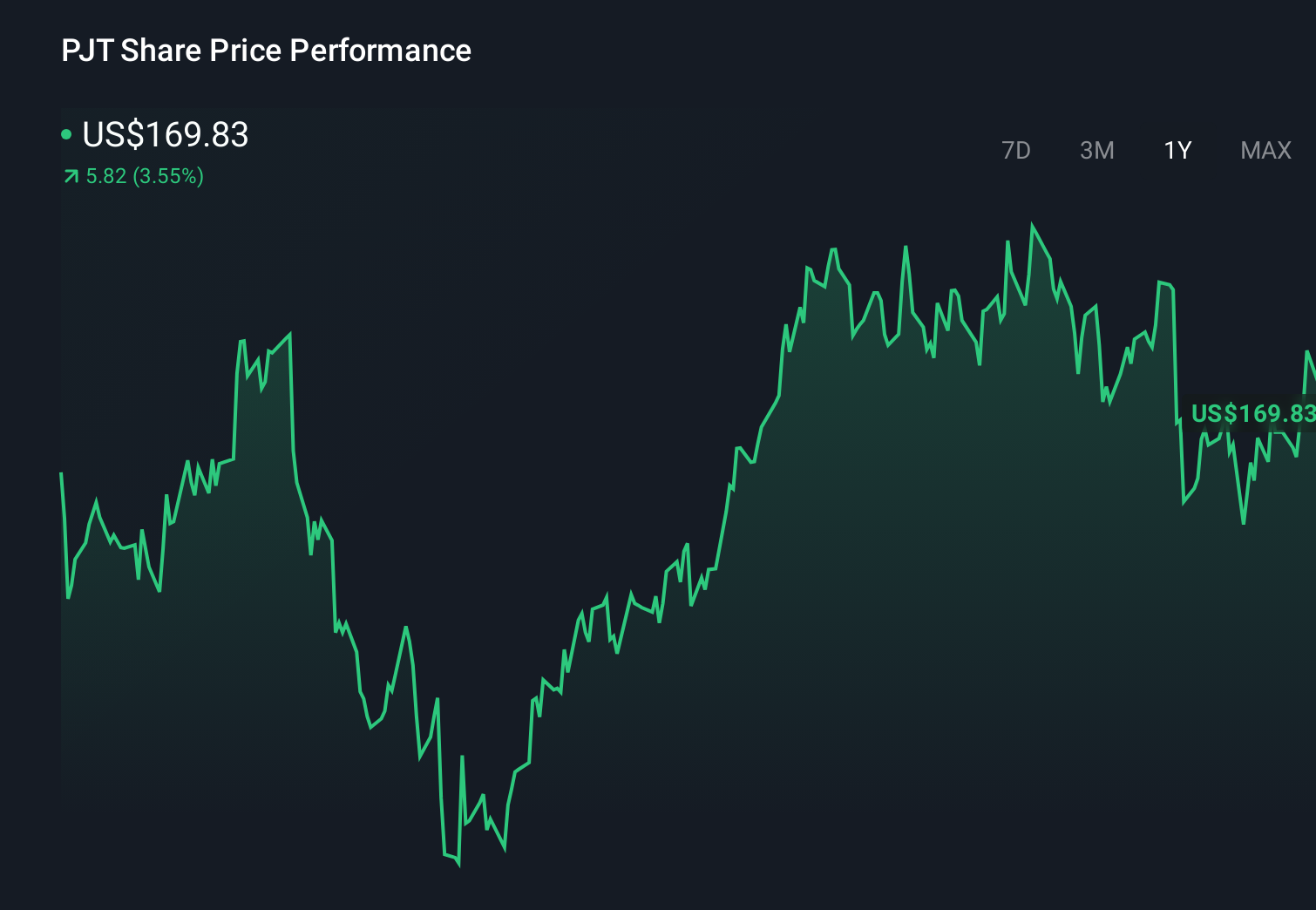

- Next, we’ll examine how the stronger-than-expected earnings and newly authorized US$800 million repurchase shape PJT Partners’ investment narrative.

Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

What Is PJT Partners' Investment Narrative?

To own PJT Partners, you really have to believe in its ability to convert advisory talent and a lean balance sheet into consistently healthy profitability, while returning a lot of cash to shareholders. The latest quarter fits that story: earnings came in ahead of expectations, net income edged higher, and the Board paired a steady US$0.25 dividend with completion of a sizable multi‑year buyback and a new US$800 million authorization. In the near term, that kind of capital return and earnings surprise can be a supportive catalyst, particularly after a softer share price performance year‑to‑date. But the biggest risk has not gone away: PJT still depends on transaction activity, and a slowdown in deal volumes or restructuring mandates would matter more to the business than one strong quarter or a larger buyback.

However, one key risk could easily catch new shareholders off guard. Despite retreating, PJT Partners' shares might still be trading 18% above their fair value. Discover the potential downside here.Exploring Other Perspectives

Explore 2 other fair value estimates on PJT Partners - why the stock might be worth as much as 22% more than the current price!

Decide For Yourself

Disagree with this assessment? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your PJT Partners research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free PJT Partners research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate PJT Partners' overall financial health at a glance.

Curious About Other Options?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Outshine the giants: these 18 early-stage AI stocks could fund your retirement.

- Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

- Find 51 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com