Why Polaris is on investors’ radar now

Polaris (PII) has drawn fresh attention after a year total return of 98.47% along with a recent month gain of 24.79%, prompting investors to reassess the stock’s valuation and risk profile.

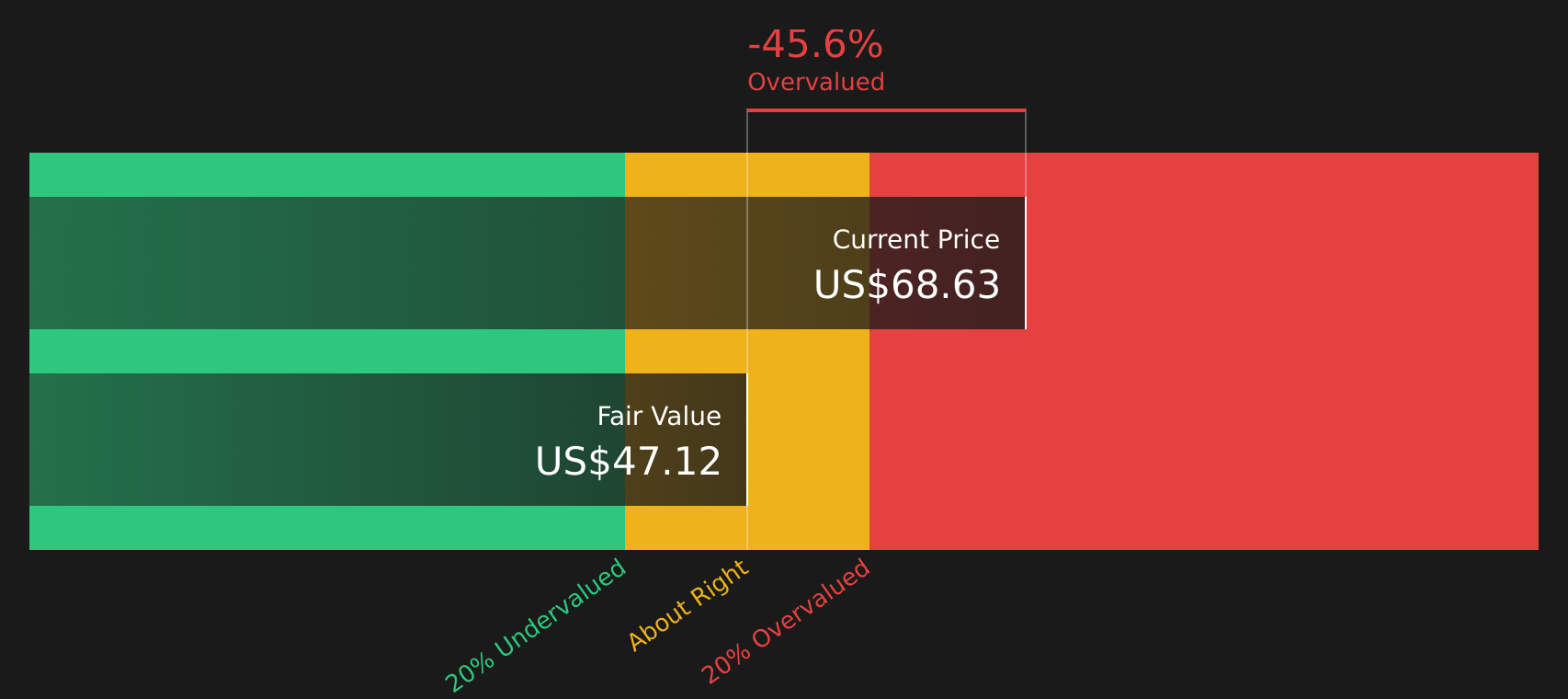

See our latest analysis for Polaris.

With the share price at US$67.06, Polaris has seen a strong 30 day share price return of 24.79% and a 1 year total shareholder return of 98.47%. However, the 3 and 5 year total shareholder returns remain negative, which suggests that recent momentum contrasts with a weaker longer term track record.

If Polaris’s rebound has caught your eye, it can be useful to see what else is moving in related areas of the market through 18 top founder-led companies

With Polaris trading near its analyst price target and an estimated 15% intrinsic discount, the recent rally raises a key question: is there still a buying opportunity here, or are markets already pricing in future growth?

Most Popular Narrative: 1.6% Overvalued

Polaris closed at $67.06, just above the most followed fair value estimate of $66.00 that applies an 8.17% discount rate to future cash flows.

Polaris is focused on a strategic approach to mitigate the impact of tariffs through supply chain adjustments and cost control initiatives, which could potentially preserve net margins and improve earnings over time.

The core of this narrative is not the recent share price move; it is a detailed earnings rebuild that leans on efficiency gains, steadier demand and a reset profit multiple. Curious which revenue path and margin level this story assumes to land on that fair value, and how long earnings would need to compound to get there.

Result: Fair Value of $66.00 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this story can unravel if tariff costs near the forecast US$320 million to US$370 million, hit margins harder than expected, or if powersports demand stays weak.

Find out about the key risks to this Polaris narrative.

Another way to look at Polaris’s value

The narrative above leans on future earnings and a fair value of $66.00, which suggests the stock is 1.6% overvalued. Yet our DCF model presents a different perspective, with Polaris at $67.06 trading 15.5% below an estimated future cash flow value of $79.34.

This split view, slightly overvalued on earnings assumptions but undervalued on cash flows, leaves you to decide which set of expectations appears more realistic for margins, tariffs and demand over the next few years.

Look into how the SWS DCF model arrives at its fair value.

Next Steps

If this mix of risks and rewards feels finely balanced, do not wait too long to check the underlying data and form your own stance. You can start with 3 key rewards and 3 important warning signs.

Looking for more investment ideas?

Polaris might be front of mind today, but the real edge comes from lining up a few fresh ideas so you are ready before the next move.

- Target value first and sort through companies that combine quality fundamentals with attractive pricing using 51 high quality undervalued stocks.

- Prioritise resilience and focus on companies with stronger finances through the solid balance sheet and fundamentals stocks screener (44 results).

- Cast a wider net and hunt for under-followed opportunities with the screener containing 23 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com