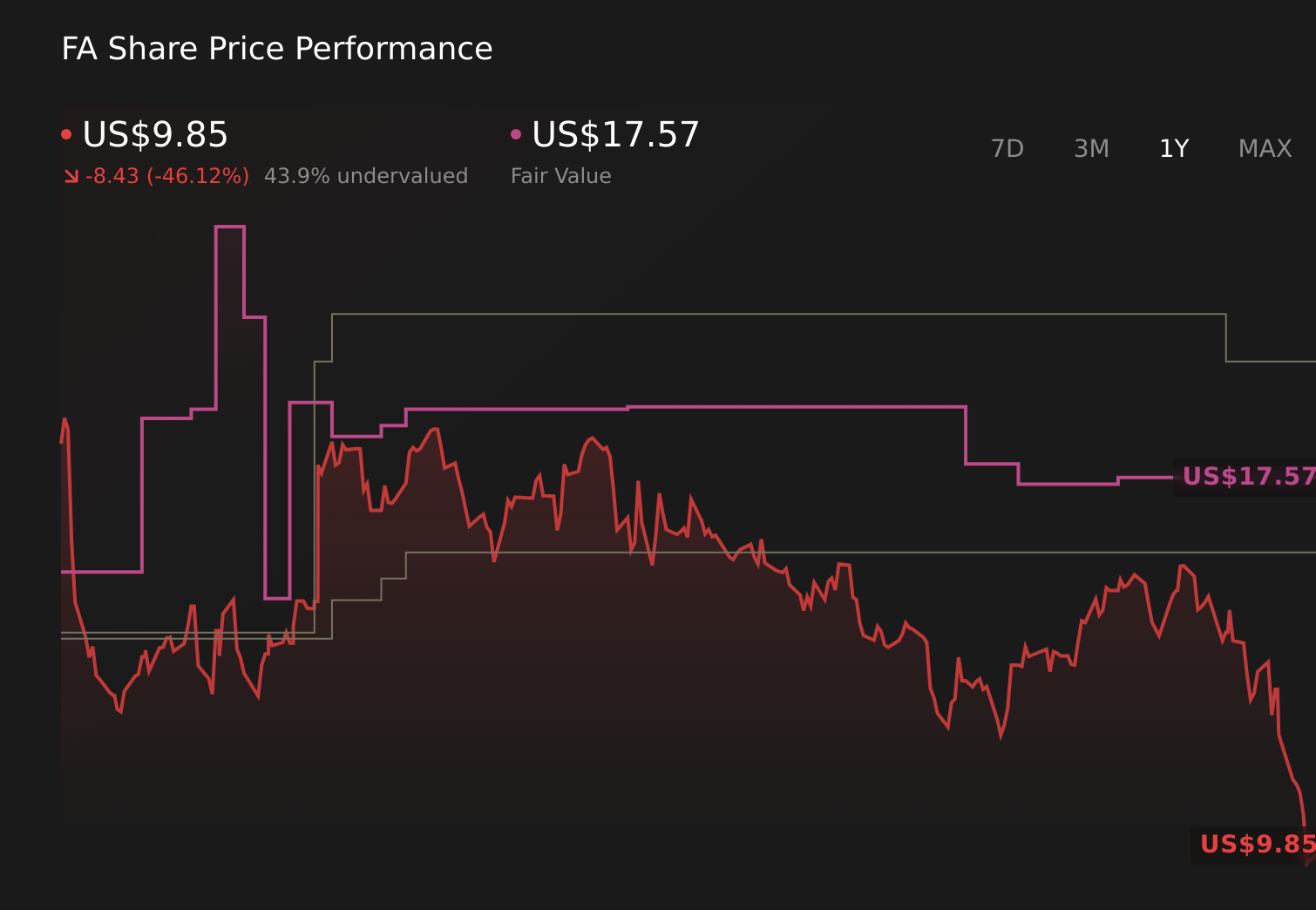

- First Advantage Corporation reported past first-quarter 2026 results with revenues of US$385.2 million, turning last year’s US$41.19 million net loss into a US$2.17 million net profit and delivering earnings modestly above break-even.

- The company also reaffirmed its 2026 revenue outlook of US$1.63 billion to US$1.70 billion while emphasizing high customer retention, international expansion, and ongoing share repurchases and debt reduction.

- Next, we’ll examine how reaffirmed 2026 guidance and improving profitability shape First Advantage’s existing investment narrative and future expectations.

This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

First Advantage Investment Narrative Recap

To own First Advantage, you need to believe that high customer retention, growing screening demand, and its integrated platform can translate into steadier profitability over time. The main near term catalyst is management’s ability to turn recent revenue growth into consistent earnings, while the biggest risk remains pressure on hiring volumes and pricing in a fragmented market. The latest quarter confirms improving profitability but does not materially change those core drivers or risks.

Against that backdrop, the reaffirmed 2026 revenue outlook of US$1.63 billion to US$1.70 billion is especially relevant. It connects directly to the key catalyst of converting international expansion and strong enterprise relationships into predictable top line performance, while the ongoing share repurchases and debt reduction highlight management’s focus on capital discipline as it works through integration and margin pressures.

Yet, even with guidance intact, investors should still watch how competitive pricing and hiring volumes could suddenly pressure margins and cash flow...

Read the full narrative on First Advantage (it's free!)

First Advantage's narrative projects $1.9 billion revenue and $168.3 million earnings by 2029. This requires 7.1% yearly revenue growth and a $203.1 million earnings increase from -$34.8 million today.

Uncover how First Advantage's forecasts yield a $15.00 fair value, a 6% downside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were assuming around US$2.0 billion of revenue and US$169.8 million of earnings by 2029, which is far more cautious than the consensus. When you compare those expectations with the latest quarter's modest profit and reaffirmed guidance, it highlights how differently you might weigh risks like weaker margins in the Sterling business versus the potential benefits of cost efficiencies and technology improvements, and why it can be helpful to examine several viewpoints before deciding where you stand.

Explore another fair value estimate on First Advantage - why the stock might be worth 6% less than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your First Advantage research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free First Advantage research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate First Advantage's overall financial health at a glance.

Contemplating Other Strategies?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Capitalize on the AI infrastructure supercycle with our selection of the 38 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 33 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com