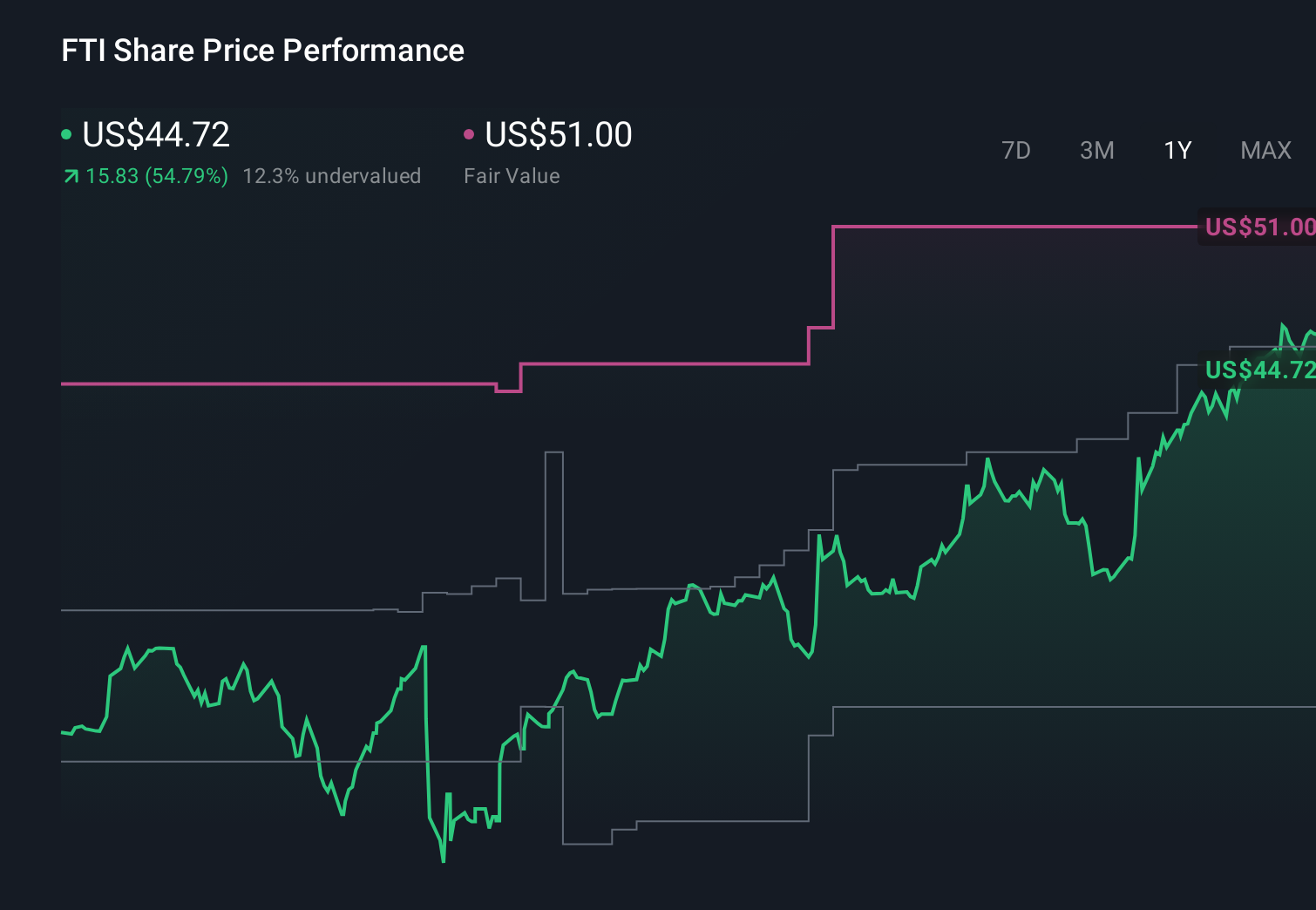

- In the first quarter of 2026, TechnipFMC plc reported higher revenue of US$2,492.7 million and net income of US$260.5 million, while also completing a multi‑year share repurchase program totaling 69,776,247 shares for US$1,887.76 million and affirming a quarterly dividend of US$0.05 per share.

- This combination of earnings growth, substantial buybacks since 2022, and ongoing cash returns through dividends underlines management’s emphasis on capital returns and operating discipline.

- We’ll now examine how the strong first‑quarter earnings and completion of a large buyback program may reshape TechnipFMC’s investment narrative.

Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

TechnipFMC Investment Narrative Recap

To be a TechnipFMC shareholder today, you need to believe that its subsea focused backlog and integrated project model can keep translating into solid earnings and cash generation, despite exposure to oil and gas cycles and geopolitically sensitive regions. The latest quarter’s higher revenue of US$2,492.7 million and net income of US$260.5 million, combined with completion of a sizeable buyback, support the near term earnings and capital return story without materially changing the key risk of long duration project delays.

The most relevant recent announcement is the completion of the multi year share repurchase program, which retired 69,776,247 shares for US$1,887.76 million since 2022. Together with the affirmed US$0.05 quarterly dividend, it reinforces TechnipFMC’s pattern of using improving earnings to support shareholder returns, an important element for those focused on how the existing subsea backlog and services tail convert into per share results while longer dated geopolitical and energy transition risks remain in the background.

But while capital returns look appealing, investors should also be aware that geopolitical project delays could...

Read the full narrative on TechnipFMC (it's free!)

TechnipFMC's narrative projects $11.8 billion revenue and $1.3 billion earnings by 2029. This requires 5.8% yearly revenue growth and about a $0.3 billion earnings increase from $963.9 million today.

Uncover how TechnipFMC's forecasts yield a $65.62 fair value, a 8% downside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were expecting revenue of about US$10.5 billion and earnings near US$936 million by 2028, yet they warned that tariff and commodity price volatility could squeeze subsea margins, so you may want to compare this more cautious view with the recent earnings beat and decide which future feels closer to your own expectations.

Explore 3 other fair value estimates on TechnipFMC - why the stock might be worth 8% less than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your TechnipFMC research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free TechnipFMC research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate TechnipFMC's overall financial health at a glance.

No Opportunity In TechnipFMC?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Outshine the giants: these 15 early-stage AI stocks could fund your retirement.

- Find 47 companies with promising cash flow potential yet trading below their fair value.

- Uncover the next big thing with 26 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com