Varonis Systems (VRNS) has drawn investor attention after recent trading left the stock at a last close of US$27.84. Its performance over the past month contrasts sharply with results over the past year.

See our latest analysis for Varonis Systems.

Recent trading has been mixed, with a 30-day share price return of 37.89% contrasting with a year-to-date share price decline of 13.11% and a 1-year total shareholder return that fell 39.32%. This combination suggests short term momentum but longer term pressure on sentiment.

If you are comparing Varonis with other opportunities in data security and AI driven software, it could be useful to scan the market using the 60 profitable AI stocks that aren't just burning cash

With Varonis trading at a reported 31% discount to its analyst price target and an indicated 31% intrinsic discount, the key question is whether this points to undervaluation or whether the market is already pricing in future growth.

Most Popular Narrative: 16.7% Undervalued

With Varonis trading at $27.84 against a narrative fair value of $33.43, the most followed view in the market points to meaningful upside potential, anchored in a detailed set of growth and profitability assumptions.

Rapid proliferation of enterprise data and increased AI adoption are materially boosting demand for automated, comprehensive data protection, positioning Varonis to capture higher revenue growth and expand its total addressable market as organizations prioritize data security for both compliance and risk mitigation.

Want to see what sits behind that confidence in higher revenue and future margins? The narrative leans on specific growth rates, margin shifts, and a premium earnings multiple that only make sense when viewed together.

Result: Fair Value of $33.43 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that upside story runs into two key risks, including ongoing losses of US$130.4 million and uncertainty around the SaaS transition’s impact on growth and margins.

Find out about the key risks to this Varonis Systems narrative.

Another View on Valuation

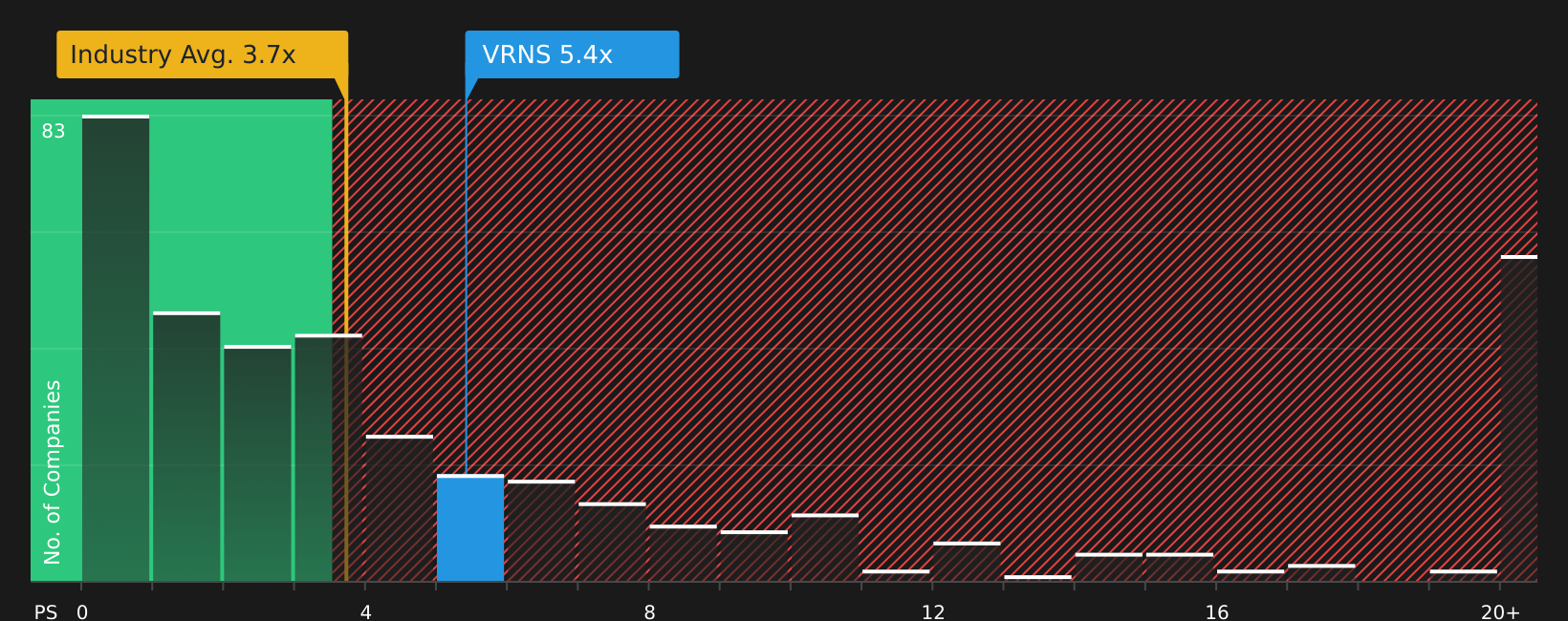

While the narrative fair value of $33.43 points to upside, the current P/S of 4.8x paints a different picture. It is higher than the US Software industry at 3.6x and above peers at 4.0x, and even matches the 4.8x fair ratio, which limits any clear margin of safety. So is the market already paying up for the story here?

For a closer look at how this pricing stacks up against fundamentals over time, it is worth checking See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Mixed signals on price, growth expectations, and risk can be hard to reconcile. Act while the data is fresh, review the numbers yourself, and weigh the 3 key rewards and 1 important warning sign.

Looking for more investment ideas?

Do not stop at a single stock. Use powerful screeners to spot other opportunities that match your goals, or you could miss ideas that better fit your portfolio.

- Target potential mispricings by scanning for companies trading below their assessed value using the 45 high quality undervalued stocks.

- Focus on stability and resilience by filtering for companies with stronger finances and lower risk profiles via the 69 resilient stocks with low risk scores.

- Get ahead of the crowd by uncovering lesser known opportunities with solid fundamentals using the screener containing 22 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com