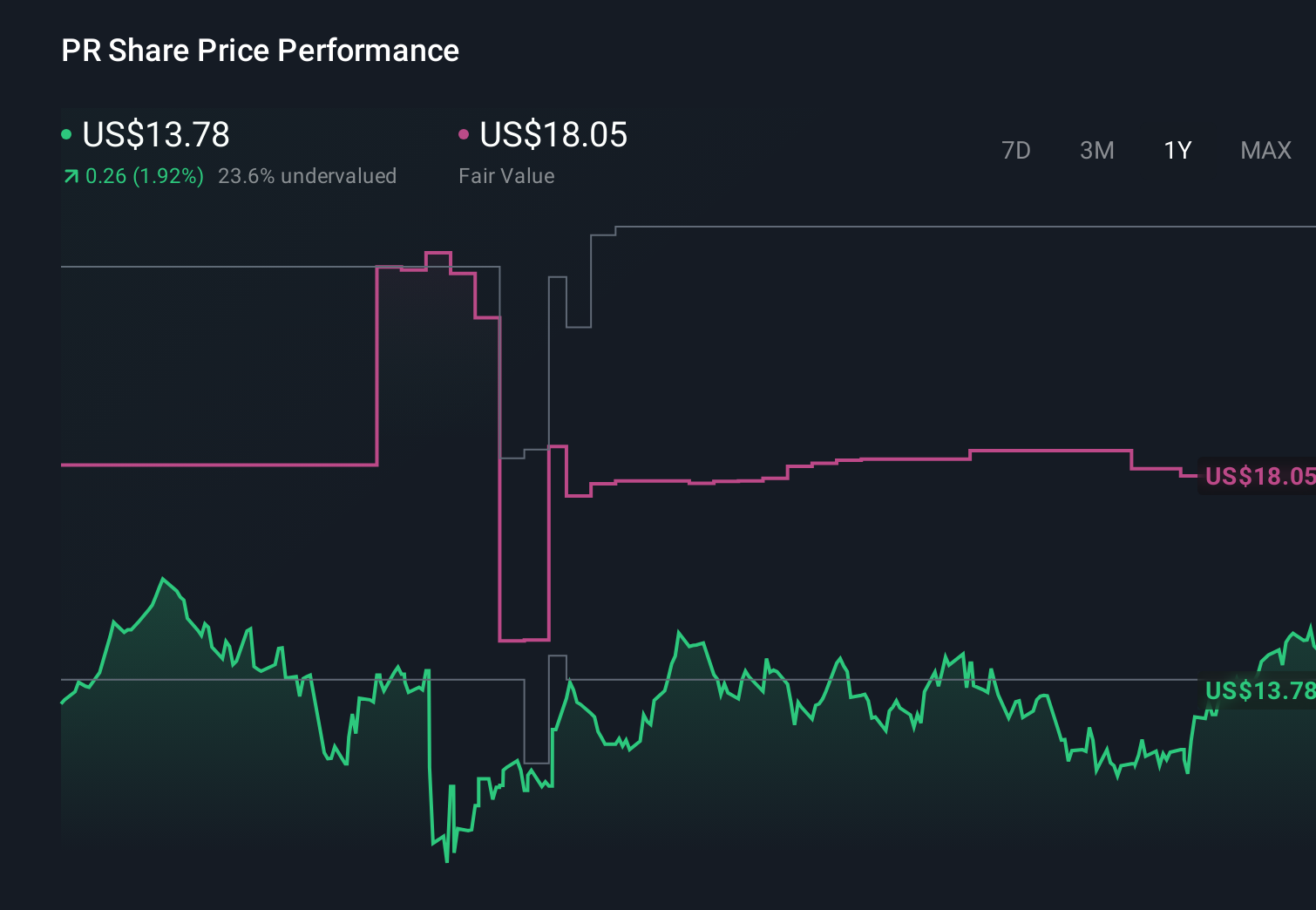

- In early May 2026, Permian Resources Corporation reported first-quarter 2026 results showing net income of US$43.62 million versus US$329.30 million a year earlier, alongside a quarterly base dividend declaration of US$0.16 per Class A share payable on June 30, 2026.

- While earnings and earnings per share fell sharply and revenue missed analyst expectations, management highlighted record-low well costs, more than US$500 million in free cash flow, and ongoing plans to return capital through cost reductions, acquisitions, and organic growth.

- Next, we will examine how weaker Q1 earnings but strong free cash flow and an affirmed dividend affect Permian Resources’ investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 39 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Permian Resources Investment Narrative Recap

To own Permian Resources, you need to believe its low cost Permian footprint and efficiency gains can support attractive cash generation despite commodity and regulatory uncertainty. The sharp Q1 earnings decline and small post‑result share price pullback highlight near term sensitivity to profitability, but the quarter’s strong free cash flow and affirmed dividend do not materially change the core near term catalyst around operational efficiency, or the key risk tied to sustaining cash flows if pricing or well performance weaken.

The most relevant recent announcement is the Board’s decision to maintain a quarterly base dividend of US$0.16 per Class A share (US$0.64 annualized), even after weaker Q1 results. For investors focused on capital returns, this supports the idea that free cash flow remains resilient enough, for now, to fund ongoing payouts while the company pursues cost reductions, integration of past acquisitions, and operational improvements that underpin the main catalysts.

Yet, investors should not overlook the risk that if well productivity or inventory replacement disappoints, especially after such a sharp earnings step down, it could...

Read the full narrative on Permian Resources (it's free!)

Permian Resources' narrative projects $6.4 billion revenue and $1.3 billion earnings by 2029. This implies 7.9% yearly revenue growth and an earnings increase of about $364.8 million from $935.2 million today.

Uncover how Permian Resources' forecasts yield a $23.90 fair value, a 18% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were expecting earnings to reach about US$1.8 billion by 2029, but Q1’s earnings drop and free cash flow strength may both challenge and support that view, so it is worth comparing this upbeat scenario with more conservative takes before you decide which story you believe.

Explore 5 other fair value estimates on Permian Resources - why the stock might be worth over 3x more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Permian Resources research is our analysis highlighting 3 key rewards and 4 important warning signs that could impact your investment decision.

- Our free Permian Resources research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Permian Resources' overall financial health at a glance.

Interested In Other Possibilities?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

- Uncover the next big thing with 28 elite penny stocks that balance risk and reward.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 16 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com