Howard Hughes Holdings (HHH) is back in focus after first quarter 2026 results showed revenue of US$235.92 million and net income of US$8.23 million, alongside updates on residential land activity and the pending Vantage acquisition.

See our latest analysis for Howard Hughes Holdings.

The first quarter revenue update and progress on the Vantage acquisition come against a weaker backdrop for the stock, with the share price down 22.92% over 90 days and the 1 year total shareholder return declining 8.74%, suggesting momentum has cooled despite recent operational news.

If this kind of real estate story has your attention, it can be useful to see how other companies are shaping up too. Now could be a good time to broaden your search and discover 18 top founder-led companies

With the stock down sharply over the past year, even as revenue and net income figures sit in the black, the real question for you is whether Howard Hughes is now trading below its underlying value or if the market is already pricing in future growth.

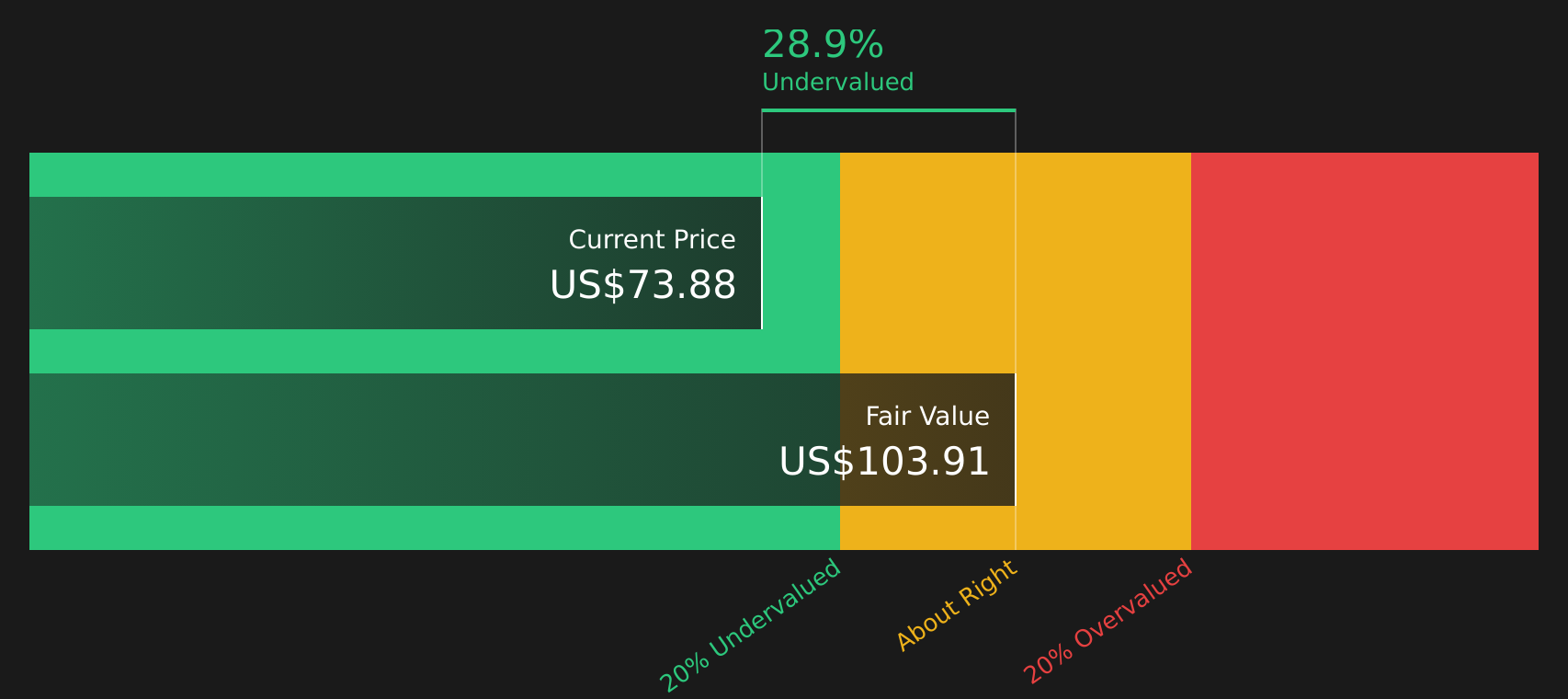

Most Popular Narrative: 32.6% Undervalued

With Howard Hughes Holdings last closing at $63.79 against a narrative fair value of $94.67, the current pricing sits well below the central long term story analysts are using.

The company's substantial undeveloped land bank in highly desirable markets positions it to capture long-term price appreciation and incremental cash flow as demand for premium, amenity-rich suburban and town-center communities intensifies, enhancing long-term revenue growth and intrinsic asset value.

The fair value hinges on how this land bank is converted into earnings, how much margins can expand, and which future profit multiple investors might ultimately accept.

Result: Fair Value of $94.67 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this story could change quickly if the planned move into insurance stumbles, or if debt refinancing becomes more expensive and pressures future flexibility.

Find out about the key risks to this Howard Hughes Holdings narrative.

Another Way To Look At The Valuation

The SWS DCF model also points to value, with an estimated future cash flow value of $97.50 per share compared with the current $63.79 price. That is a sizeable gap in favor of the stock, so the key question is whether the underlying cash flow assumptions feel realistic to you.

Look into how the SWS DCF model arrives at its fair value.

Next Steps

Given the mix of optimism and caution in this story, it makes sense to move quickly, review the full data, and weigh both sides for yourself with 3 key rewards and 2 important warning signs.

Looking for more investment ideas?

If Howard Hughes has sharpened your focus on opportunities, do not stop here. Use the screener to uncover fresh stocks that could suit your approach.

- Hunt for quality at a discount by scanning 51 high quality undervalued stocks that combine strong fundamentals with prices that sit below their estimated worth.

- Prioritize resilience by checking 66 resilient stocks with low risk scores that score well on stability so sharp drawdowns are less likely to catch you off guard.

- Spot potential future standouts early by searching the screener containing 21 high quality undiscovered gems before they appear on every investor's radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com