Dropbox (DBX) drew fresh investor attention after reporting Q1 2026 results that topped analyst expectations and lifting its full year revenue and unlevered free cash flow guidance, alongside stable customer retention trends.

See our latest analysis for Dropbox.

That stronger Q1 update and higher 2026 guidance came alongside a 10.5% 1 month share price return and a 9.6% 3 month share price return. However, the 1 year total shareholder return declined 6.6%, hinting at improving short term momentum compared with a more muted longer record.

If Dropbox’s results have you looking at productivity and automation trends, it can be useful to widen the lens and review 63 profitable AI stocks that aren't just burning cash for other potential ideas.

With guidance lifted, cash generation running above US$1b and the share price already up in recent months, is Dropbox still trading at a discount, or are markets already pricing in most of its future growth potential?

Most Popular Narrative: 5.2% Overvalued

Analysts following Dropbox currently see fair value at $25.50, a touch below the last close at $26.82. This frames the latest rally in a more cautious light.

Persistent emphasis on operational efficiency via infrastructure optimization, disciplined hiring, and lower marketing spend has resulted in sustained improvements in non-GAAP operating margins and free cash flow, enhancing the company's ability to invest in long-term growth areas while also supporting increasing earnings and cash flow per share.

Want to understand why a flat revenue outlook can still support this valuation? The narrative leans heavily on margin durability, rich cash generation and a future earnings multiple that differs from many peers. The exact mix of earnings, cash flow and required return assumptions is where the story gets interesting.

Result: Fair Value of $25.50 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, it is still worth flagging that revenue and annual recurring revenue are both in decline, and competitive pressure on pricing could keep margins under pressure.

Find out about the key risks to this Dropbox narrative.

Another View: Multiples Paint a Different Picture

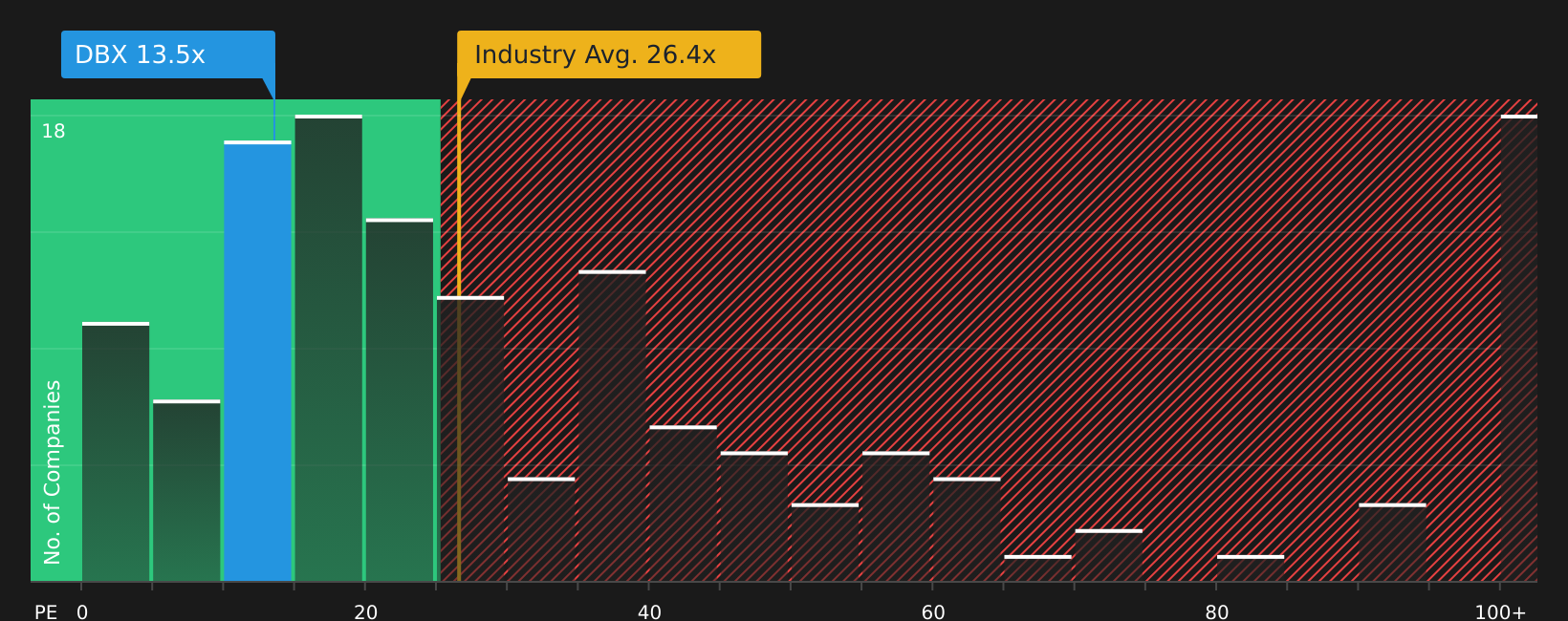

While the popular narrative sees Dropbox as around 5.2% overvalued at $25.50, the current P/E of 13.2x tells a different story. It sits well below both the peer average of 20.4x and the US Software industry at 28.3x, and even below the 19.6x fair ratio the market could move towards. For you, that gap raises a clear question: is this cautious pricing justified by slow growth and high debt, or does it hint at mispriced earnings power?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With mixed signals on value and growth, sentiment around Dropbox is clearly divided, so it makes sense to move quickly and weigh the upside and downside for yourself using our 3 key rewards and 2 important warning signs

Looking for more investment ideas?

If Dropbox has sharpened your thinking, do not stop here. Broaden your watchlist now so you are not relying on a single stock for opportunity.

- Target potential value opportunities by scanning 51 high quality undervalued stocks that combine solid fundamentals with pricing that may appeal to patient investors.

- Strengthen your focus on resilience by reviewing 66 resilient stocks with low risk scores that aim to keep volatility and financial stress in check.

- Hunt for fresh opportunities by using the screener containing 21 high quality undiscovered gems before they appear on everyone else's radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com