American International Group (AIG) is drawing investor attention after appointing veteran financier Thomas Stoddard as an independent director, coinciding with Eric Andersen taking over as CEO in a planned leadership transition.

See our latest analysis for American International Group.

The share price has picked up in the very short term, with a 1 day share price return of 2.96% and 7 day share price return of 3.02%, but is still down 7.01% year to date. The 5 year total shareholder return of 69.16% points to a stronger longer run record as the leadership refresh, including Eric Andersen and Thomas Stoddard, shapes expectations about growth and risk.

If this governance shake up has you thinking more broadly about opportunities, it could be a good moment to look at 18 top founder-led companies

With AIG shares down 7.01% year to date, but trading at a discount to a US$88.05 analyst target and an indicated intrinsic value gap of about 53%, investors have to ask: is there still a buying opportunity here, or are markets already pricing in future growth?

Most Popular Narrative: 9.4% Undervalued

With American International Group last closing at $78.36 against a narrative fair value of $86.45, the prevailing view is that the stock trades at a discount that hinges on execution in underwriting, digitalisation and capital use.

The acceleration of digitalization and artificial intelligence initiatives, such as the Gen AI deployment across underwriting and claims, positions AIG to enhance operational efficiency, improve underwriting precision, reduce fraud, and offer more tailored insurance products, supporting improved net margins and sustained earnings growth.

Read the complete narrative. Read the complete narrative.

Want to see how this story gets from today’s earnings to that higher fair value? The narrative leans heavily on compounding revenue, rising margins and a lower future earnings multiple. The exact mix of those three levers may surprise you.

Analysts behind this widely followed narrative are effectively asking you to weigh moderate revenue growth, firmer profitability and ongoing buybacks against a relatively low assumed P/E years from now. The discount rate used is 6.98%, so even small changes in your own growth or margin assumptions could lead you to a very different fair value than $86.45.

Result: Fair Value of $86.45 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that story can change quickly if climate related catastrophe losses or higher legal and claims costs eat into underwriting results and pressure future margins.

Find out about the key risks to this American International Group narrative.

Another Lens On AIG’s Valuation

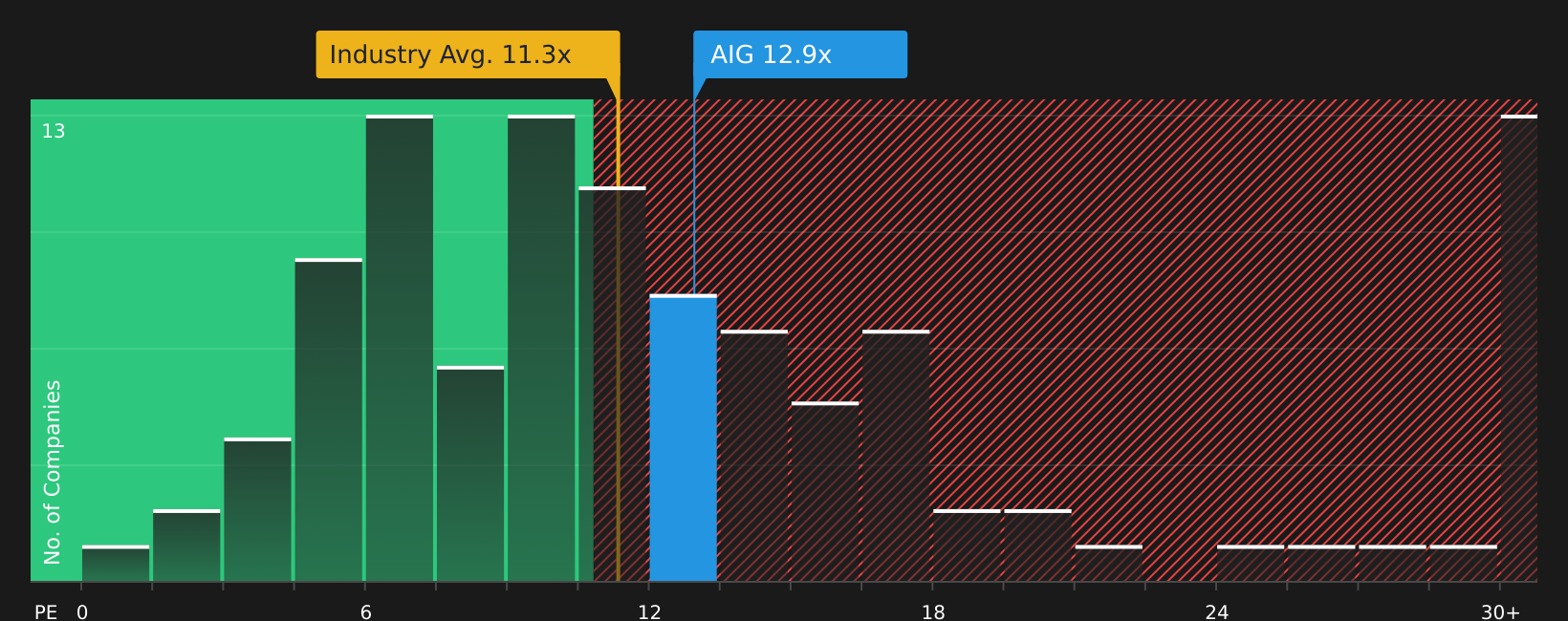

The earlier fair value of $86.45 comes from a narrative built around future earnings and margins, but the current 13.1x P/E is higher than both the US Insurance industry at 11.1x and peers at 9x, and above a 12.7x fair ratio. Does that premium point to confidence, or valuation risk?

To see what the numbers say about this pricing gap and how the fair ratio could shift over time, take a closer look at See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With sentiment mixed across valuation, growth and governance, this is a good time to inspect the details yourself and decide how compelling AIG really looks. To see what is currently exciting investors, review the 3 key rewards

Ready to hunt for your next idea?

If AIG has sharpened your thinking, do not stop here. Broaden your watchlist with focused stock ideas that match how you like to invest.

- Target quality at a discount by scanning 51 high quality undervalued stocks that pair strong fundamentals with prices below their estimated worth.

- Prioritise resilience by checking solid balance sheet and fundamentals stocks screener (45 results) that aim for robust financial footing and fewer balance sheet surprises.

- Get ahead of the crowd by researching screener containing 21 high quality undiscovered gems before they sit on everyone else's radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com