- Earlier in 2026, EMCOR Group reported a sharp increase in data center infrastructure revenues tied to AI-related demand, prompting management to raise full-year 2026 revenue and EPS guidance while also scheduling multiple investor conference appearances and disclosing further insider share sales.

- This combination of AI-fueled data center growth, higher guidance, and active investor outreach underscores how central digital infrastructure has become to EMCOR’s project mix and future workload visibility.

- We’ll now examine how this AI-driven data center strength and upgraded outlook could influence EMCOR’s broader investment narrative and risk profile.

Uncover the next big thing with 29 elite penny stocks that balance risk and reward.

EMCOR Group Investment Narrative Recap

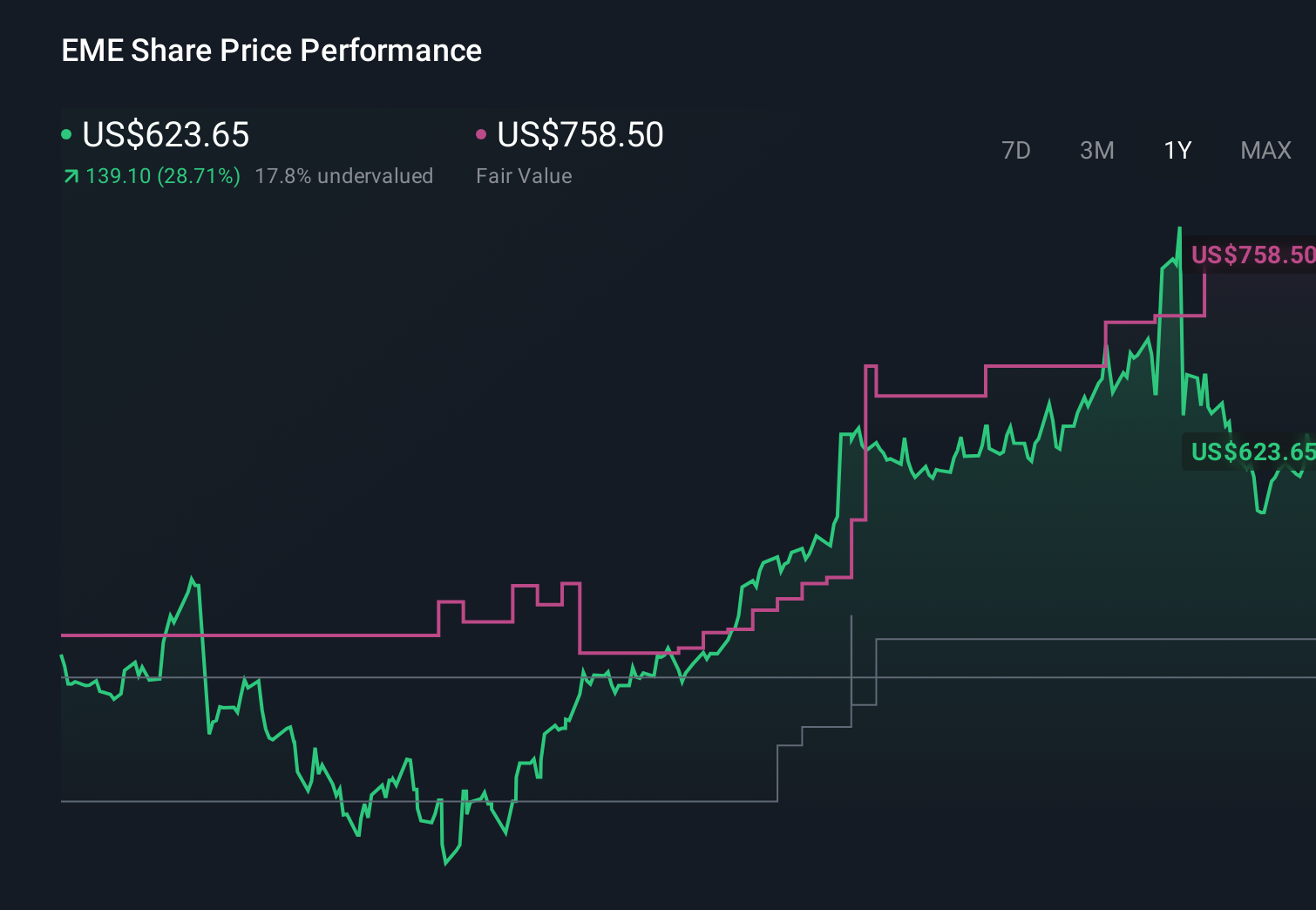

To own EMCOR, you need to believe its core strengths in complex electrical and mechanical projects will remain in demand as data centers, healthcare, and industrial customers keep investing in infrastructure. The recent AI-driven spike in data center work and raised 2026 guidance appears to reinforce the near term growth catalyst of a strong backlog in digital infrastructure, while also sharpening the key risk that EMCOR becomes more exposed to cyclical swings in a few large, project based end markets.

Among recent announcements, the April 2026 guidance hike stands out as most relevant. Management lifted full year revenue expectations to US$18.50 billion to US$19.25 billion and raised EPS guidance after reporting strong Q1 2026 results, which included higher data center related revenues. For investors focused on catalysts, this upgraded outlook ties directly to the AI and cloud driven demand surge, but it also raises the bar for future execution and consistency across other segments.

Yet behind the upbeat AI and data center story, investors should also be aware of the risk that growing automation and prefabrication could eventually reshape EMCOR’s core service model and...

Read the full narrative on EMCOR Group (it's free!)

EMCOR Group's narrative projects $21.5 billion revenue and $1.6 billion earnings by 2029.

Uncover how EMCOR Group's forecasts yield a $983.50 fair value, a 12% upside to its current price.

Exploring Other Perspectives

Some of the lowest analysts were already cautious, assuming revenue of about US$19.5 billion and earnings of roughly US$1.4 billion by 2028, and seeing automation and prefabrication as long term threats to EMCOR’s service model, so this latest AI driven data center surge could either challenge or reinforce their more pessimistic view depending on how sustainable you think this demand really is.

Explore 6 other fair value estimates on EMCOR Group - why the stock might be worth 25% less than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your EMCOR Group research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free EMCOR Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate EMCOR Group's overall financial health at a glance.

Interested In Other Possibilities?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Capitalize on the AI infrastructure supercycle with our selection of the 43 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 29 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com