- Wondering whether Compañía de Minas BuenaventuraA is still good value after its strong share price run, or if recent moves are already pricing in the story? This article walks through what the numbers actually say about the stock.

- The share price closed at US$32.87, and while it is up 15.0% year to date and has delivered 129.5% over the last year, it has recently pulled back, declining 13.7% over the past week and 8.0% over the past month.

- Recent headlines around metals and mining stocks, including discussions about gold, silver and copper producers, help frame these moves because sentiment toward commodity producers can shift quickly when expectations change. For Buenaventura, these broader sector conversations are a useful backdrop when you look at how sharply the share price has moved over the last three years and over the long term, where the total return over five years is a little more than double.

- The company currently has a value score of 3/6, which means it screens as undervalued on half of the checks used here. Next you will see how different valuation methods line up on that score, along with a broader framework for thinking about value that goes beyond any single model.

Approach 1: Compañía de Minas Buenaventura A Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a stock could be worth by projecting future cash flows and then discounting them back to today using a required return. It is essentially asking what Buenaventura's future cash generation is worth in today's dollars.

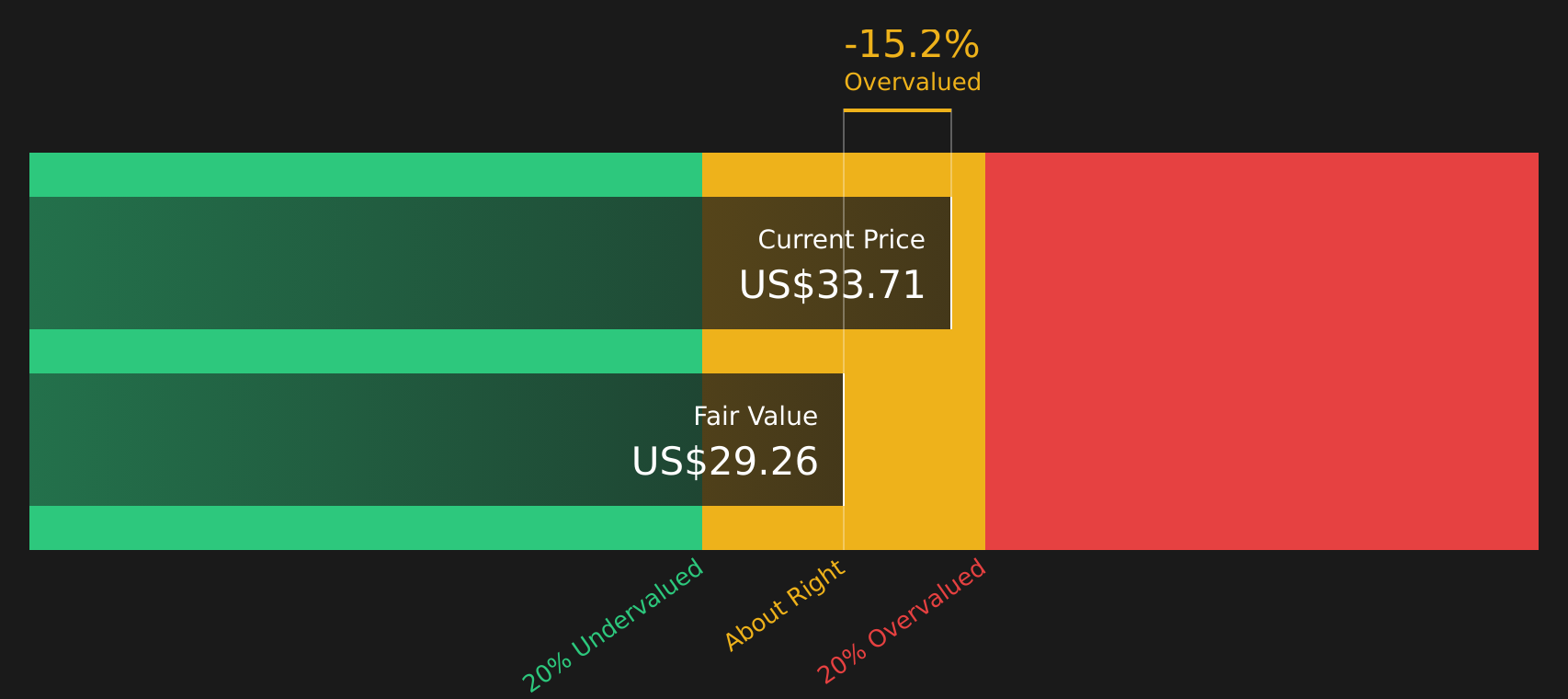

For Compañía de Minas BuenaventuraA, the model used is a 2 Stage Free Cash Flow to Equity approach. The latest twelve month free cash flow is about $350 million, and forecasts used here include an estimated free cash flow of $423.34 million in 2026 and $416 million in 2027, with further years extrapolated out to 2035 using Simply Wall St assumptions. By adding these discounted cash flows together, the DCF model arrives at an estimated intrinsic value of $29.22 per share.

Compared with the recent share price of $32.87, this DCF output implies the stock trades at about a 12.5% premium to the model's estimate. On this metric the shares screen as overvalued right now.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Compañía de Minas BuenaventuraA may be overvalued by 12.5%. Discover 54 high quality undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Compañía de Minas BuenaventuraA Price vs Earnings

For a profitable company, the P/E ratio is a helpful way to relate what you pay per share to the earnings that each share generates. It gives you a quick sense of how many years of current earnings the market is effectively pricing in.

What counts as a “normal” or “fair” P/E depends on how the market views a company’s growth prospects and risk. Higher expected growth and lower perceived risk can support a higher P/E, while slower growth or higher risk tends to justify a lower one.

Compañía de Minas BuenaventuraA currently trades on a P/E of 8.46x. That is well below the Metals and Mining industry average of 19.64x and also below the peer group average of 63.42x, which suggests the stock is priced more cautiously than many competitors. Simply Wall St’s Fair Ratio for the company is 17.78x, which is a proprietary estimate of what the P/E could be given factors such as earnings growth, industry, profit margin, market cap and specific risks.

Because the Fair Ratio folds these fundamentals into a single number, it can be more tailored than a simple comparison with broad industry or peer averages. Setting 17.78x against the actual 8.46x implies the stock trades below that Fair Ratio benchmark.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Upgrade Your Decision Making: Choose your Compañía de Minas BuenaventuraA Narrative

Earlier it was mentioned that there is an even better way to understand valuation, so Narratives are introduced here as a simple way for you to attach a clear story about Compañía de Minas BuenaventuraA to the numbers you care about. This links your view of its future revenue, earnings and margins to a forecast and then to a Fair Value that can be compared with the current price to help you decide whether to buy, hold or sell. All of this is available within an easy tool on Simply Wall St’s Community page that updates automatically when fresh information like news or earnings arrives. One investor might set a Narrative closer to the more optimistic US$42.00 Fair Value, while another aligns with a more cautious US$24.00 view, both using the same framework but different assumptions about how projects like San Gabriel, copper output and costs will shape the company’s financials over time.

For Compañía de Minas BuenaventuraA, however, we will make it really easy for you with previews of two leading Compañía de Minas BuenaventuraA Narratives:

🐂 Compañía de Minas BuenaventuraA Bull Case

Fair value in this upbeat narrative: US$39.58 per share.

At the recent share price of US$32.87, this narrative views the stock as about 17% below that fair value estimate.

Implied revenue growth assumption: 2.32% a year.

- San Gabriel, El Brocal and Cerro Verde are central, with higher gold and copper output plus more diversified revenue all linked to the thesis.

- Cost control, capital discipline and deleveraging are key, with bond redemption and stable CapEx guidance used to support the case for stronger future cash flow.

- The narrative relies on analyst assumptions for 2029 revenues of US$2.2b, earnings of US$874.1m and a future P/E of 15.6x, and it encourages you to test whether those inputs match your own expectations.

🐻 Compañía de Minas BuenaventuraA Bear Case

Fair value in this cautious narrative: US$24.00 per share.

At the recent share price of US$32.87, this narrative views the stock as about 37% above that fair value estimate.

Implied revenue growth assumption: 8.90% a year.

- San Gabriel is treated as a key operational risk, with remaining permits, commissioning and complex tailings management all seen as possible sources of delay or higher costs.

- Lower copper, silver and gold volumes and pressure on grades at several mines, together with higher commercial deductions on silver, sit at the center of the weaker earnings outlook.

- The narrative ties its US$24.00 target to assumptions for 2029 revenues of US$1.8b, earnings of US$337.6m and a P/E of 24.2x, and asks whether the current valuation already prices in more optimistic outcomes than those figures imply.

If you want to see how other investors are framing these stories around their own assumptions, you can use the Community Narratives tool as a starting point and then adjust the inputs to suit your view of projects, metals prices and execution risk over time. To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Compañía de Minas BuenaventuraA on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for Compañía de Minas BuenaventuraA? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com