Recent share performance and business snapshot

West Pharmaceutical Services (WST) has drawn fresh attention after recent share price moves, with the stock flat over the past day but recording gains over the past week, month and past 3 months.

Against this backdrop, investors are revisiting the company’s role in drug containment and delivery systems, its US$3.2b revenue base and US$542.7m net income, and how these fundamentals compare with recent market enthusiasm.

See our latest analysis for West Pharmaceutical Services.

Recent share price strength is hard to ignore, with West Pharmaceutical Services posting a 29.56% 3 month share price return and a 54.42% 1 year total shareholder return, which suggests momentum has been building around its US$316.42 stock.

If this kind of momentum has you thinking about where else growth stories could emerge, it may be worth scanning opportunities across 34 healthcare AI stocks

With West Pharmaceutical Services trading at US$316.42, supported by US$3.2b in revenue and US$542.7m in net income, the key question remains: is the stock still undervalued, or is the market already pricing in future growth?

Most Popular Narrative: 10% Undervalued

On the most followed narrative, West Pharmaceutical Services' fair value sits at $349.85 compared with the last close of $316.42. This frames a modest valuation gap that hinges on specific earnings and margin assumptions.

The introduction of an automated line for HVP delivery devices later in 2025 to early 2026 is expected to improve margins by driving operational efficiencies and scale, enhancing net margins. The strategic focus on expanding the contract manufacturing business into drug handling, which is expected to be higher margin and require lower capital intensity, could improve net margins and earnings after the initial ramp-up phase.

Want to see what kind of revenue mix, margin uplift and earnings profile are baked into that fair value and P/E path? The narrative spells out a detailed glide path that leans on higher value components, richer contract work and a specific discount rate to tie it all back to today.

Result: Fair Value of $349.85 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there are still pressure points to watch, including potential margin impact from tariffs and the risk that product pricing or mix ends up weaker than modeled.

Find out about the key risks to this West Pharmaceutical Services narrative.

Another angle on valuation

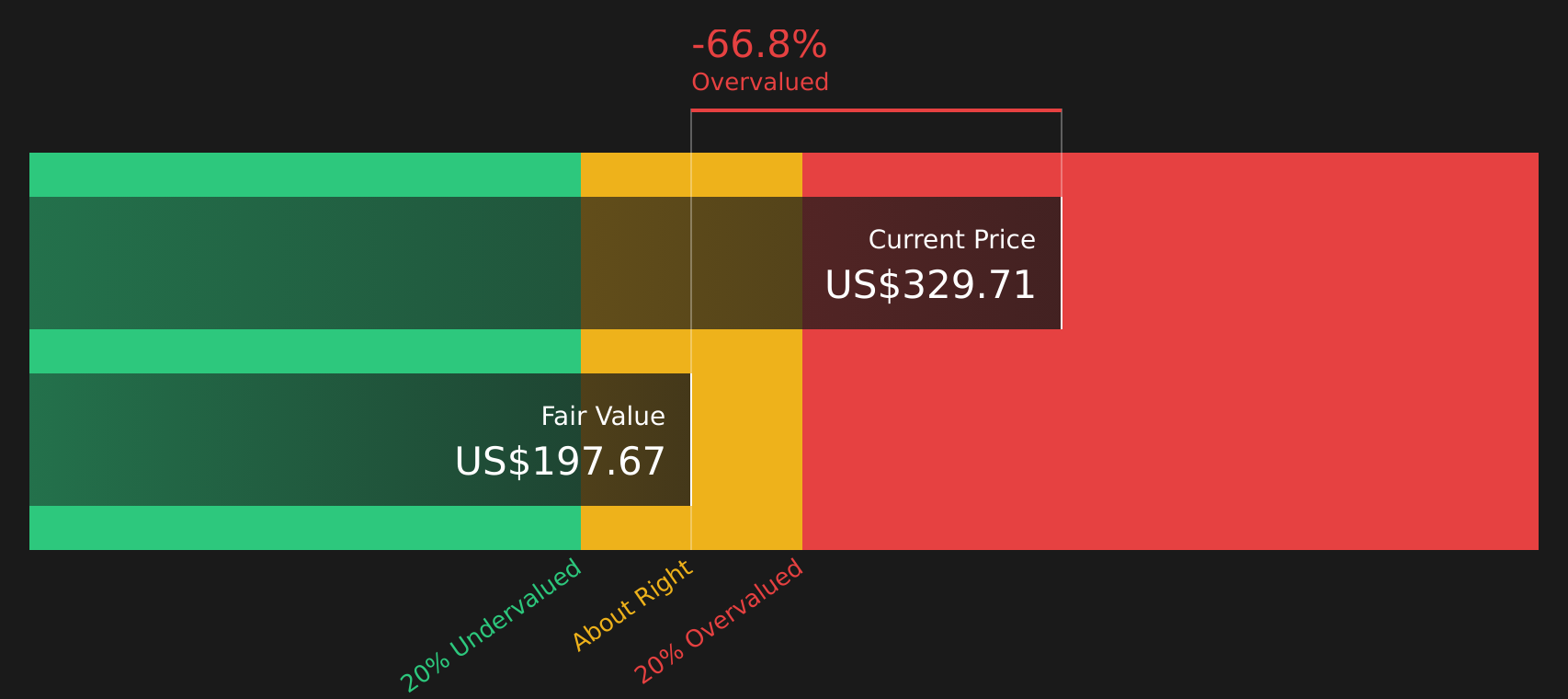

While the most popular narrative points to a fair value of $349.85, our DCF model presents a different perspective. On that view, West Pharmaceutical Services at $316.42 is trading above an estimated future cash flow value of $207.20, which appears more overvalued than undervalued. Which interpretation seems more realistic to you?

Look into how the SWS DCF model arrives at its fair value.

Next Steps

If the mixed signals in this article leave you unsure, that is a useful starting point. You can now pressure test the assumptions yourself by checking the 2 key rewards.

Looking for more investment ideas?

If this has sharpened your thinking on West Pharmaceutical Services, do not stop here. Broader ideas can help you stress test your portfolio and uncover fresh possibilities.

- Spot potential value by reviewing companies that screen well on price and fundamentals using the 49 high quality undervalued stocks.

- Strengthen your income stream by focusing on businesses that feature in the 10 dividend fortresses.

- Reduce overall portfolio swings by checking companies that appear in the 66 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com