- Earlier in May 2026, Goldman Sachs added DoorDash to its U.S. Conviction List, citing strong Marketplace Gross Order Value growth, expanding restaurant, grocery and retail engagement, and upbeat guidance for Q2 2026 Marketplace GOV and adjusted EBITDA.

- This endorsement highlights how DoorDash’s push beyond core restaurant delivery into broader local commerce, underpinned by Deliveroo integration and DashPass growth, is increasingly central to how analysts view the business.

- We’ll now examine how Goldman Sachs’ Conviction List endorsement, grounded in DoorDash’s broad-based platform growth, affects the company’s existing investment narrative.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 13 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

DoorDash Investment Narrative Recap

To own DoorDash, you need to believe its shift from restaurant delivery to a broader local commerce platform can justify a premium valuation while managing rising complexity and regulation. The key near term catalyst remains execution on multi-vertical growth and Deliveroo integration, with regulatory and labor costs still the biggest overhang. Goldman Sachs adding DoorDash to its U.S. Conviction List reinforces this growth narrative but does not fundamentally change those core risks in the short term.

The news around Goldman’s endorsement lines up closely with DoorDash’s nationwide partnership with Urban Outfitters, which showcases how retail and lifestyle categories are becoming more important to the story than just food. For investors focused on catalysts, deals like Urban Outfitters help illustrate how DoorDash could keep expanding order frequency and basket size beyond restaurants, while also testing the company’s ability to execute efficiently as it stretches into more complex retail fulfillment.

Yet against this upbeat backdrop, investors should also be aware of the pressures that could build if regulatory scrutiny of gig work were to...

Read the full narrative on DoorDash (it's free!)

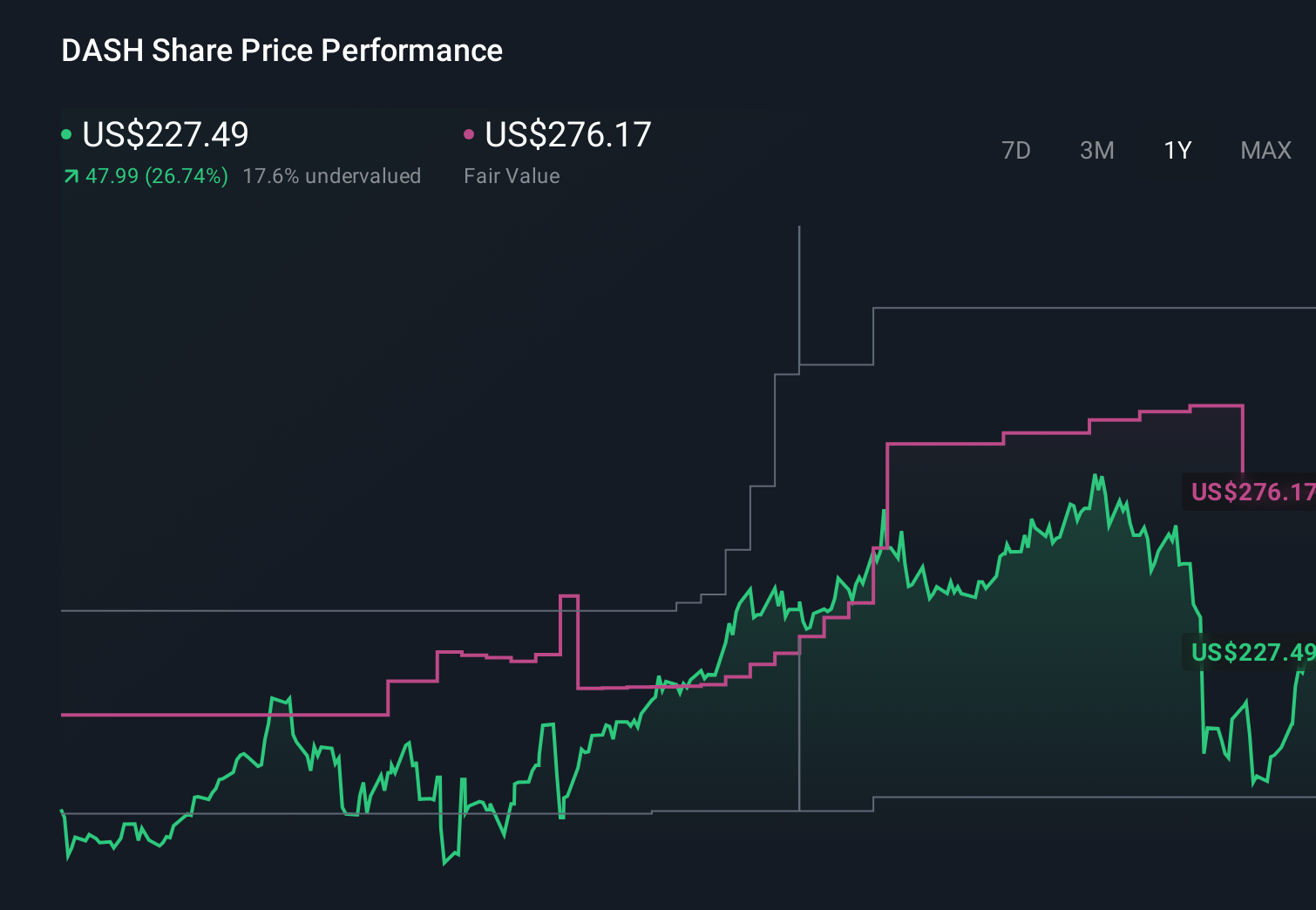

DoorDash’s narrative projects $25.2 billion revenue and $3.0 billion earnings by 2029. This requires 22.4% yearly revenue growth and a roughly $2.1 billion earnings increase from $935.0 million today.

Uncover how DoorDash's forecasts yield a $250.93 fair value, a 57% upside to its current price.

Exploring Other Perspectives

The most bullish analysts were already modeling revenue of about US$21.9 billion and earnings around US$4.8 billion by 2028, so this new push into broader commerce could either reinforce that optimistic view or, if execution or regulatory costs bite harder than expected, highlight why those forecasts were always more ambitious than the consensus you are comparing them to.

Explore 11 other fair value estimates on DoorDash - why the stock might be worth over 2x more than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your DoorDash research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free DoorDash research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate DoorDash's overall financial health at a glance.

Seeking Other Investments?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Rare earth metals are the new gold rush. Find out which 27 stocks are leading the charge.

- Capitalize on the AI infrastructure supercycle with our selection of the 46 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com