The United States market has shown robust performance, rising 3.1% over the last week and climbing 27% in the past year, with anticipated annual earnings growth of 16% in the years ahead. In this thriving environment, identifying stocks that offer unique value propositions and strong potential for growth can be key to uncovering hidden opportunities.

Top 10 Undiscovered Gems With Strong Fundamentals In The United States

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| First Bancorp | 68.18% | 1.28% | -2.88% | ★★★★★★ |

| Security Federal | 17.59% | 5.51% | 0.13% | ★★★★★★ |

| Tri-County Financial Group | 70.32% | -2.03% | -13.70% | ★★★★★★ |

| Southern Michigan Bancorp | 110.47% | 7.93% | 2.26% | ★★★★★★ |

| Cashmere Valley Bank | 31.17% | 5.25% | 1.74% | ★★★★★★ |

| ASA Gold and Precious Metals | NA | 12.65% | 41.20% | ★★★★★★ |

| Oakworth Capital | 26.12% | 15.98% | 13.01% | ★★★★★★ |

| Sound Financial Bancorp | 16.27% | 0.75% | -13.28% | ★★★★★★ |

| Union Bankshares | 374.44% | 1.11% | -7.71% | ★★★★★☆ |

| NameSilo Technologies | 12.63% | 14.48% | 3.12% | ★★★★★☆ |

We're going to check out a few of the best picks from our screener tool.

FirstSun Capital Bancorp (FSUN)

Simply Wall St Value Rating: ★★★★★★

Overview: FirstSun Capital Bancorp is the bank holding company for Sunflower Bank, National Association, offering commercial and consumer banking and financial services to small and medium-sized companies in the United States, with a market cap of $1.05 billion.

Operations: FirstSun Capital Bancorp generates revenue primarily through its Banking segment, which contributes $322.60 million, and Mortgage Operations, adding $76.56 million. The Corporate segment shows a negative contribution of -$4.49 million.

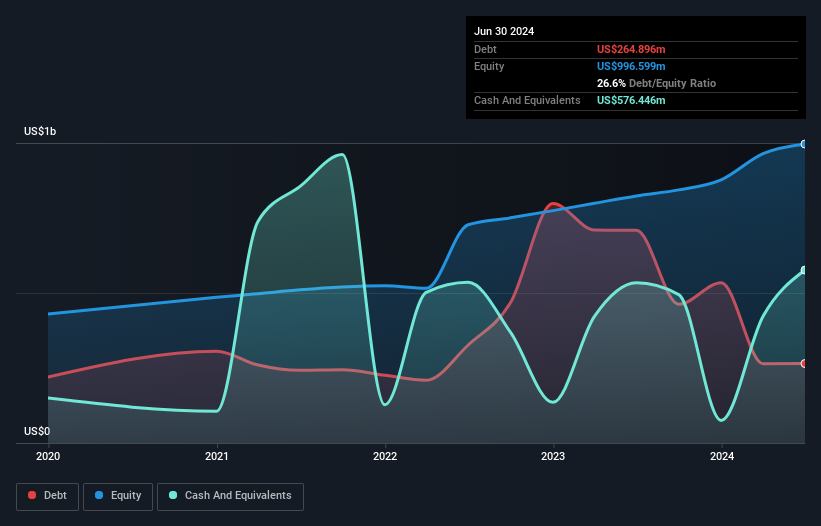

FirstSun Capital Bancorp, with total assets of US$8.5 billion and equity of US$1.2 billion, stands out in the banking sector for its strategic expansion into Southwestern and California markets. The bank's robust deposit base of US$7.1 billion and loans totaling US$6.6 billion reflect its growth potential, supported by a sufficient allowance for bad loans at 140%. Trading at 46% below estimated fair value suggests it might be undervalued relative to peers. Despite being dropped from several Russell indexes recently, FirstSun's focus on relationship banking and fee-based services could drive future profitability amidst industry challenges like digital disruption and fintech competition.

Enerpac Tool Group (EPAC)

Simply Wall St Value Rating: ★★★★★★

Overview: Enerpac Tool Group Corp. is a company that manufactures and sells industrial products and solutions across various international markets, with a market capitalization of approximately $1.88 billion.

Operations: The primary revenue stream for Enerpac Tool Group comes from its Industrial Tool & Services segment, generating $601.42 million. The company's market capitalization is approximately $1.88 billion.

Enerpac Tool Group, a compact player in the machinery sector, recently reported Q2 2026 sales of US$154.81 million, up from US$145.53 million the prior year, though net income dipped to US$16.31 million from US$20.9 million. The firm has a satisfactory net debt to equity ratio of 21.7%, reflecting prudent financial management over time as it reduced debt levels from 55.1% to 45.9% in five years and executed share buybacks worth US$50.49 million for over a quarter-million shares recently repurchased, suggesting strategic capital allocation amid ongoing M&A considerations and robust growth forecasts at 15.77%.

Vitesse Energy (VTS)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Vitesse Energy, Inc. focuses on acquiring, developing, and producing non-operated oil and natural gas properties in the United States, with a market capitalization of approximately $765.01 million.

Operations: With revenue from the acquisition, development, and production of oil and natural gas assets amounting to $250.64 million, Vitesse Energy's financial performance is primarily driven by its activities in these sectors.

Vitesse Energy has shown a robust performance with earnings growing 20% over the past year, outpacing the Oil and Gas industry's -3.5%. The net debt to equity ratio stands at a satisfactory 19.6%, indicating manageable leverage. Recent production results highlight an increase in oil output to 4,133 MBbls from 3,291 MBbls last year, with natural gas production also rising significantly. However, significant insider selling in recent months raises some concerns about internal confidence. Despite trading at an attractive valuation of 48% below estimated fair value, future earnings are projected to decline sharply by an average of 159.4% annually over the next three years due to potential volatility and reliance on Lucero's assets post-acquisition.

Where To Now?

- Unlock more gems! Our US Undiscovered Gems With Strong Fundamentals screener has unearthed 328 more companies for you to explore.Click here to unveil our expertly curated list of 331 US Undiscovered Gems With Strong Fundamentals.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com