Over the last 7 days, the United States market has risen by 4.4%, contributing to a remarkable 32% increase over the past year, with earnings expected to grow by 16% annually. In this thriving environment, identifying stocks that combine solid fundamentals with growth potential can uncover promising opportunities for investors seeking undiscovered gems.

Top 10 Undiscovered Gems With Strong Fundamentals In The United States

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Security Federal | 17.59% | 5.51% | 0.13% | ★★★★★★ |

| Tri-County Financial Group | 70.32% | -2.03% | -13.70% | ★★★★★★ |

| Southern Michigan Bancorp | 110.47% | 7.93% | 2.26% | ★★★★★★ |

| Oakworth Capital | 26.12% | 15.98% | 13.01% | ★★★★★★ |

| Sound Financial Bancorp | 16.27% | 0.75% | -13.28% | ★★★★★★ |

| Anbio Biotechnology | NA | -30.09% | -3.45% | ★★★★★★ |

| First Northern Community Bancorp | NA | 7.53% | 11.34% | ★★★★★★ |

| Affinity Bancshares | 42.51% | 1.82% | 1.11% | ★★★★★★ |

| Winchester Bancorp | 121.44% | 49.13% | 3283.33% | ★★★★★★ |

| Oxford Bank | 12.42% | 14.34% | 4.14% | ★★★★☆☆ |

Here's a peek at a few of the choices from the screener.

Nature's Sunshine Products (NATR)

Simply Wall St Value Rating: ★★★★★★

Overview: Nature's Sunshine Products, Inc. is a natural health and wellness company that manufactures and sells nutritional and personal care products internationally, with a market cap of $468.33 million.

Operations: NATR generates revenue primarily from Asia ($221.78 million), North America ($143.61 million), and Europe ($93.13 million). The company sees additional sales from Latin America amounting to $21.62 million.

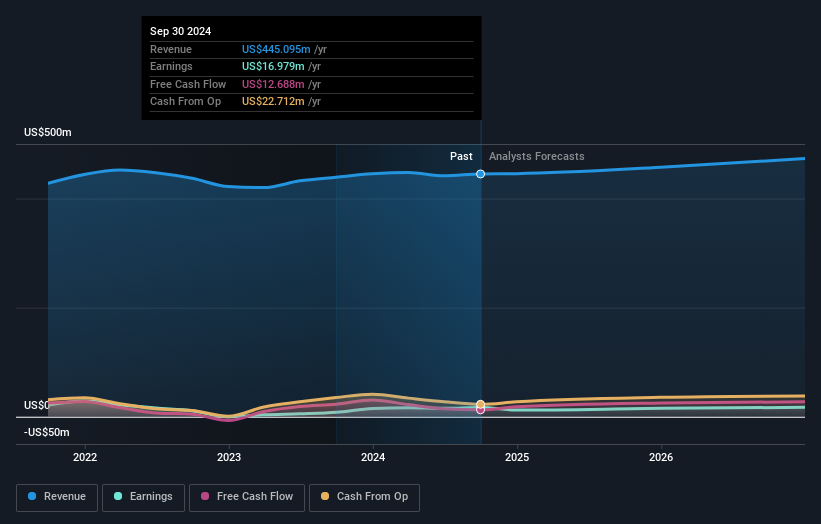

Nature's Sunshine Products, a player in the natural health and wellness sector, has shown impressive growth with earnings surging by 153.7% over the past year, outpacing industry peers. The company is debt-free now compared to five years ago when its debt-to-equity ratio was 3.1%, indicating improved financial health. Trading at 21.4% below estimated fair value, it seems undervalued given its strong digital sales increase of 34% in North America and a successful Autoship program launch. However, significant insider selling recently could indicate some internal caution despite robust financial performance and strategic initiatives driving current momentum.

Xunlei (XNET)

Simply Wall St Value Rating: ★★★★★★

Overview: Xunlei Limited, with a market cap of $378.39 million, operates an internet platform for digital media content in the People's Republic of China through its subsidiaries.

Operations: Xunlei generates revenue primarily from the operation of its online media platform, amounting to $460.43 million.

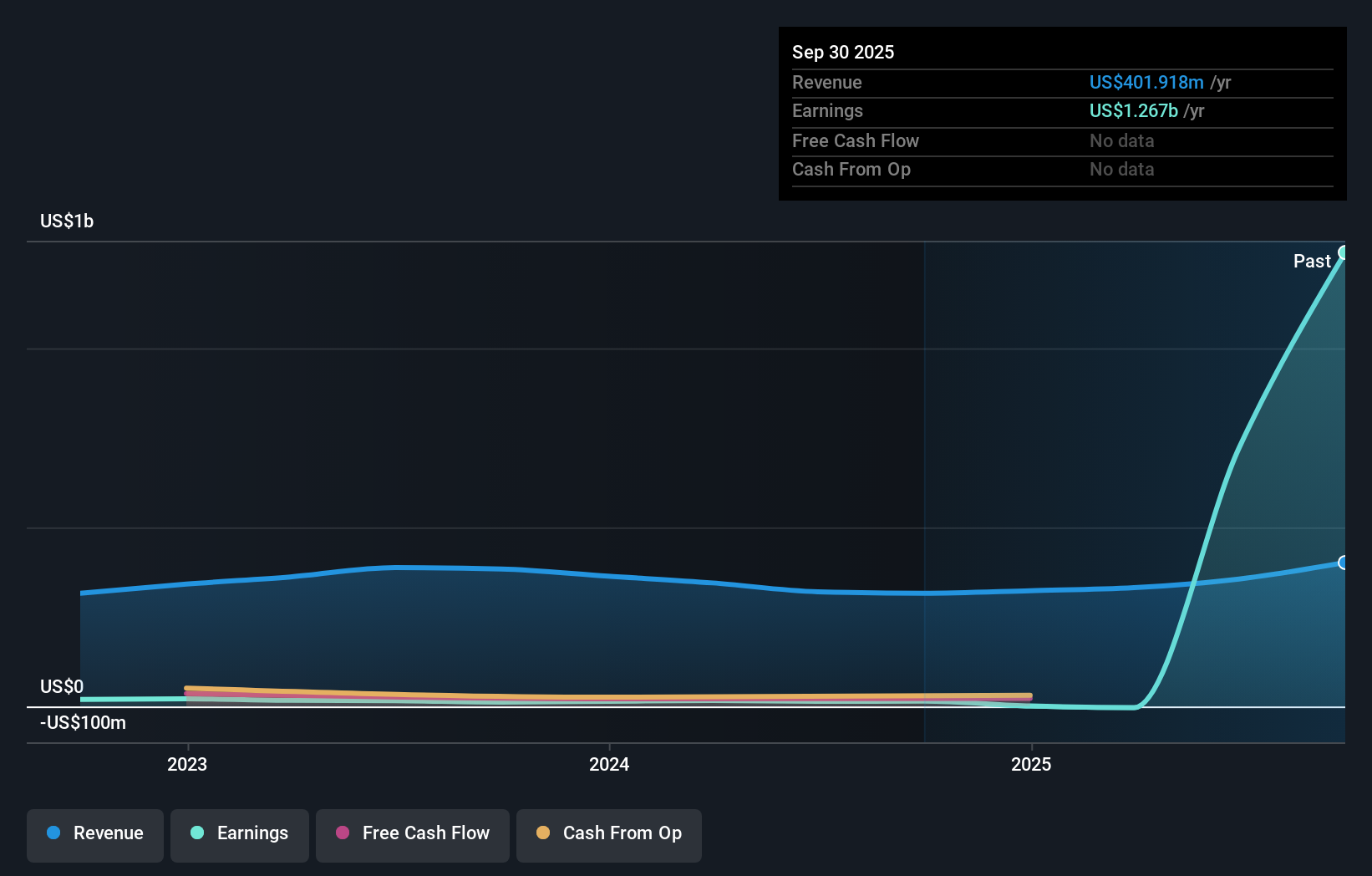

Xunlei's recent performance reveals a company with intriguing dynamics. Its earnings skyrocketed by 86,177% over the past year, significantly outpacing the software industry's growth of 18.3%. The stock trades at 18.7% below its estimated fair value, indicating potential undervaluation. Despite this impressive earnings surge, Xunlei reported a net loss of US$228.78 million for Q4 2025 compared to US$9.77 million previously, highlighting volatility in its financials. Over five years, their debt-to-equity ratio improved from 6.9% to 5.5%, suggesting better financial management amid rapid changes in revenue and profit figures.

- Take a closer look at Xunlei's potential here in our health report.

Examine Xunlei's past performance report to understand how it has performed in the past.

Central Pacific Financial (CPF)

Simply Wall St Value Rating: ★★★★★★

Overview: Central Pacific Financial Corp. is the bank holding company for Central Pacific Bank, offering various commercial banking products and services to businesses, professionals, and individuals in the United States with a market cap of $895.94 million.

Operations: Central Pacific Financial generates revenue primarily from its banking operations, amounting to $276.99 million. The company focuses on providing commercial banking services, which contribute significantly to its financial performance.

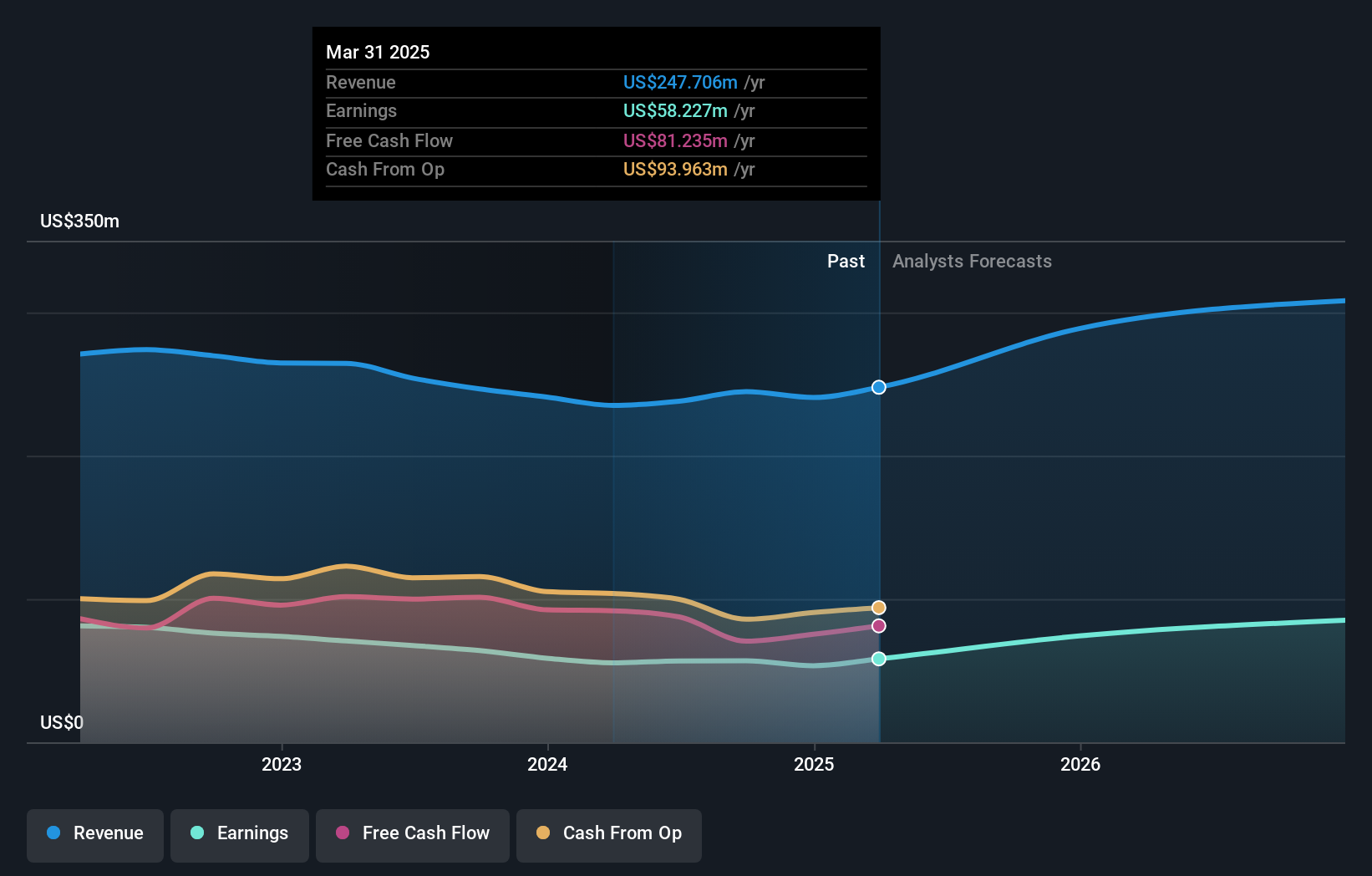

Central Pacific Financial, a financial institution with assets totaling US$7.4 billion and equity of US$592.6 million, is making strides in the banking sector. With total deposits of US$6.6 billion and loans amounting to US$5.2 billion, it maintains a net interest margin of 3.5%. The bank's focus on high-quality earnings is evident as its bad loan allowance stands at 0.3% of total loans, underscoring prudent risk management practices. Recent strategic moves include expanding digital banking services and wealth management operations in Hawaii to diversify income streams amidst rising competition from local banks and fintech companies.

Where To Now?

- Investigate our full lineup of 332 US Undiscovered Gems With Strong Fundamentals right here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com