- In the first quarter of 2026, Bank OZK reported net interest income of US$385.57 million and net income of US$163.36 million, with both basic and diluted earnings per share from continuing operations at US$1.44, slightly lower than a year earlier.

- Despite softer earnings, management highlighted growing momentum in its Corporate & Institutional Banking segment and expanding fee-based businesses, signaling a shift away from reliance on its Real Estate Specialties Group portfolio.

- We'll now examine how Bank OZK's emphasis on Corporate & Institutional Banking growth could reshape its investment narrative and future earnings mix.

This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

Bank OZK Investment Narrative Recap

To own Bank OZK, you need to be comfortable with a bank that is still heavily tied to commercial real estate while gradually leaning into Corporate & Institutional Banking and fee income. The key short term catalyst is whether CIB growth and fee-based businesses can offset softer earnings and repayment pressure in the Real Estate Specialties Group. The latest quarter modestly trims earnings but does not materially change that near term catalyst or the central risk around CRE concentration and credit quality.

The most relevant recent development is management’s emphasis that Corporate & Institutional Banking is gaining momentum and could match or exceed the RESG portfolio in the next couple of years. Paired with the buildout of trust, wealth, mortgage, and treasury services, this helps frame how Bank OZK might shift its earnings mix toward more diversified and fee-driven revenue, which matters if RESG growth stays muted or repayment headwinds remain a drag on results.

Yet despite this push into CIB, investors should still be aware of how concentrated exposure to commercial real estate could...

Read the full narrative on Bank OZK (it's free!)

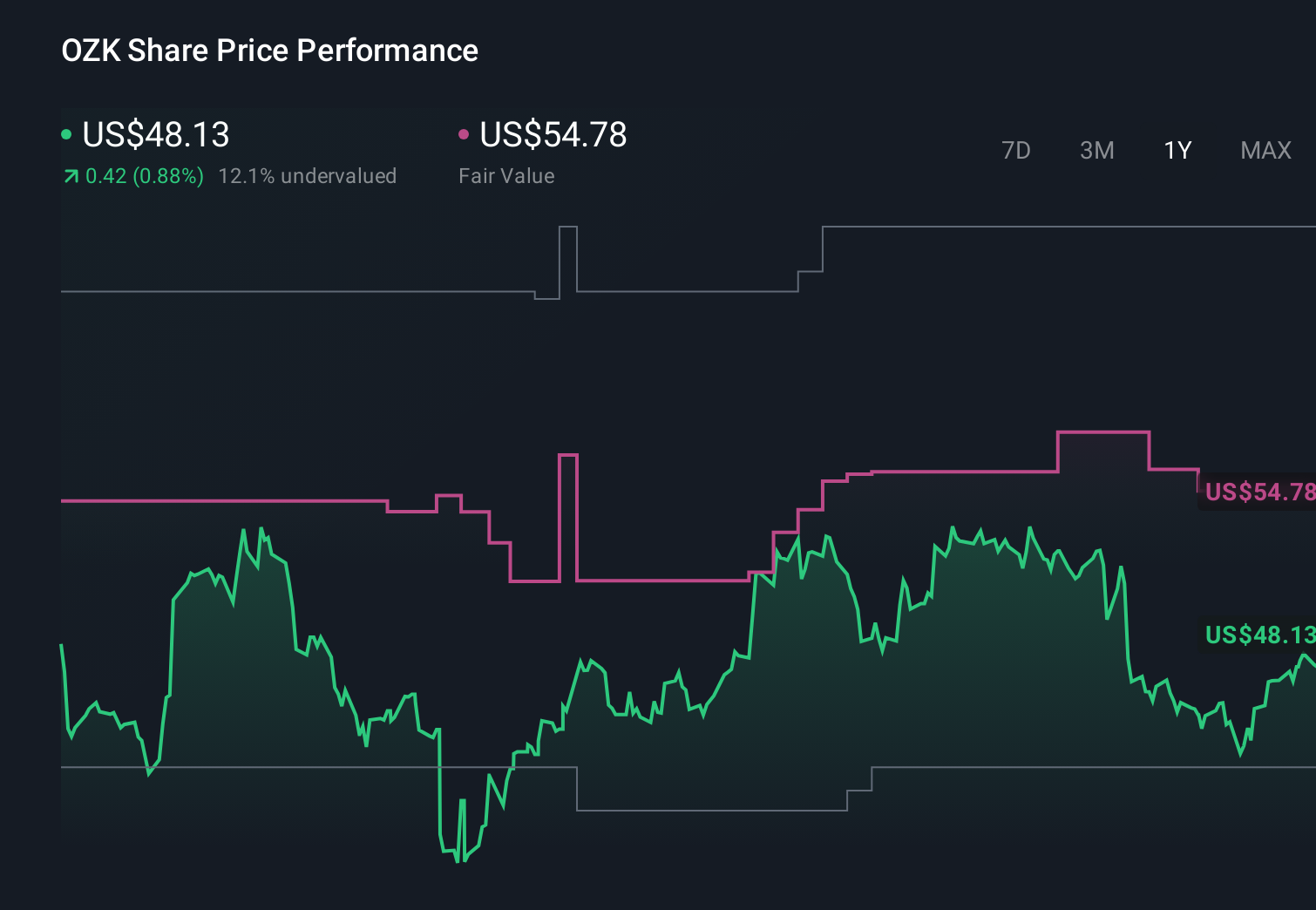

Bank OZK's narrative projects $2.1 billion revenue and $815.7 million earnings by 2028. This requires 10.6% yearly revenue growth and about a $113.6 million earnings increase from $702.1 million today.

Uncover how Bank OZK's forecasts yield a $53.00 fair value, a 9% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts paint a much cooler picture, assuming revenue of about US$1.9 billion and shrinking margins by 2029, so you can compare that more cautious view with the diversification story tied to CIB growth and decide which assumptions feel more realistic after this quarter’s numbers.

Explore 3 other fair value estimates on Bank OZK - why the stock might be worth just $53.00!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Bank OZK research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Bank OZK research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Bank OZK's overall financial health at a glance.

Interested In Other Possibilities?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Uncover the next big thing with 27 elite penny stocks that balance risk and reward.

- Find 54 companies with promising cash flow potential yet trading below their fair value.

- The future of work is here. Discover the 35 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com