- If you are wondering whether Ladder Capital is a bargain at around US$10.34, the key question is not just where the share price is today, but what that price actually implies about the business.

- The stock has moved only slightly over the past week with a 0.4% decline, yet it has returned 10.3% over the last year and 42.3% over three years. This provides useful context before comparing that performance to what the current valuation suggests.

- No major company specific headlines have recently reset the story for Ladder Capital. This makes its 3.5% gain over the past month and year to date decline of 6.8% more about shifting investor sentiment than a single news shock. For long term holders, the 31.2% return over five years sits in the background as the market continually reassesses what the shares are worth today.

- Simply Wall St currently assigns Ladder Capital a valuation score of 0 out of 6. The rest of this article will break down the usual valuation tools such as the P/E ratio, asset based measures and discounted cash flow. It will then finish with a way to read all those numbers together that can give you a clearer view of what the market might be pricing in.

Ladder Capital scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Ladder Capital Excess Returns Analysis

The Excess Returns model looks at how much profit a company generates on its equity after covering the required return that shareholders expect. If returns comfortably clear that hurdle, the stock can justify trading above book value. If not, the equity may be priced too richly.

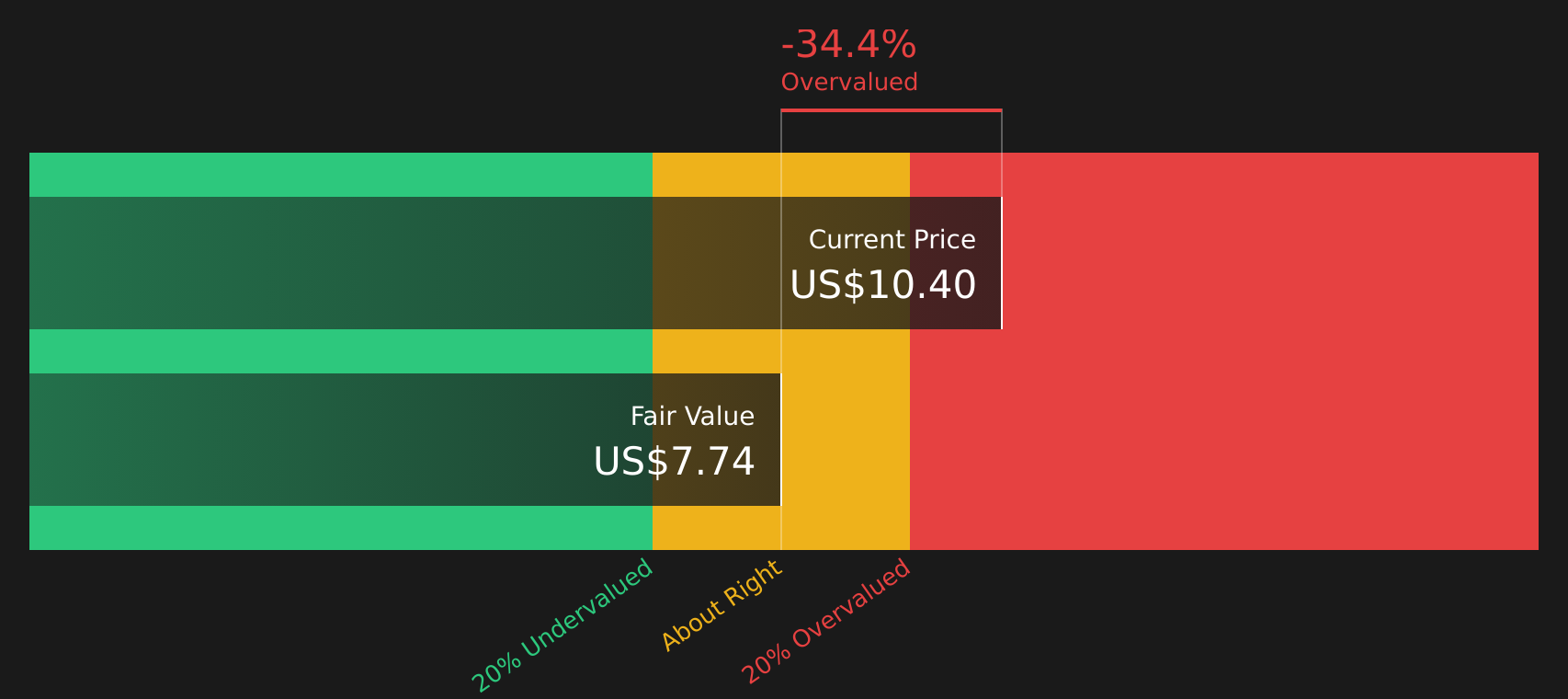

For Ladder Capital, the model uses a Book Value of $11.33 per share and a Stable EPS of $0.72 per share, based on the median return on equity from the past 5 years. The implied Cost of Equity is $0.82 per share, so the estimated Excess Return is $0.10 per share short of that hurdle. The Average Return on Equity stands at 6.46%, and analysts point to a Stable Book Value of $11.12 per share, based on weighted future book value estimates from 2 analysts.

Putting those inputs together, the Excess Returns valuation points to an intrinsic value of about $8.54 per share. Against a current share price around $10.34, that suggests the stock is roughly 21.1% overvalued on this model.

Result: OVERVALUED

Our Excess Returns analysis suggests Ladder Capital may be overvalued by 21.1%. Discover 56 high quality undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Ladder Capital Price vs Earnings

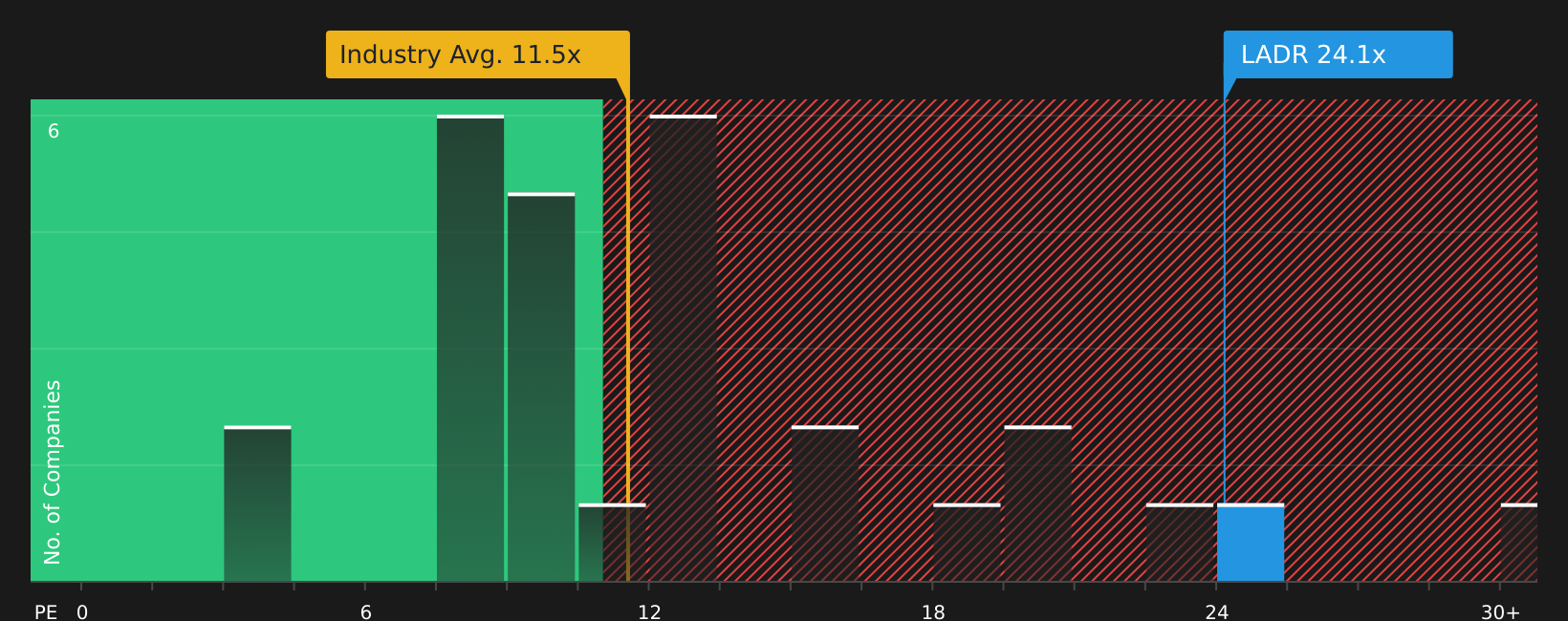

For profitable companies, the P/E ratio is a useful way to check what you are paying for each dollar of earnings, which makes it a natural tool for cross checking Ladder Capital’s valuation. A higher or lower P/E often reflects what the market thinks about a company’s growth prospects and risk profile, so there is no single “right” number, just a range that tends to make sense given those factors.

Ladder Capital currently trades on a P/E of 24.0x. That sits above the Mortgage REITs industry average of about 10.0x and also above the peer group average of 13.4x. On the surface, that points to investors placing a richer price on its earnings than on many sector peers.

Simply Wall St’s Fair Ratio for Ladder Capital is 15.0x. This is a proprietary estimate of what the P/E might be based on earnings growth expectations, risk profile, profit margins, industry, and market cap, rather than a simple comparison with a rough industry or peer average. Because it tries to align the multiple with company specific drivers, it can be a more nuanced benchmark. With the actual P/E at 24.0x versus a Fair Ratio of 15.0x, the shares look expensive on this metric.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Upgrade Your Decision Making: Choose your Ladder Capital Narrative

Earlier the article mentioned that there is an even better way to understand valuation. Narratives on Simply Wall St give you a clear story behind the numbers by letting you set your own view on Ladder Capital’s future revenue, earnings and margins. You can then link that story to a forecast and a fair value on the Community page, and compare that fair value with the current price. The system updates automatically when new earnings or news arrive. One investor might build a Narrative that lines up with the higher US$14.00 analyst target, while another might anchor closer to the lower US$11.50 target. Both perspectives are visible, comparable and easy to track in one place.

Do you think there's more to the story for Ladder Capital? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com