- At its April 21, 2026 Annual Shareholders’ Meeting, Banco Latinoamericano de Comercio Exterior, S.A. approved changing its name to Bladex Inc., elected new Class “A” and Class “E” directors, reported higher net interest income and net income for the first quarter of 2026, affirmed a US$0.6875 quarterly dividend, and announced a MXN 4.27 billion floating-rate note due 2029.

- This combination of a refreshed corporate identity, board changes, solid quarterly results, and new funding issuance highlights how Bladex is reshaping its capital structure and governance while continuing to return cash to shareholders.

- We’ll now examine how the first-quarter earnings strength and dividend affirmation influence Bladex’s existing investment narrative and risk‑reward profile.

Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

Banco Latinoamericano de Comercio Exterior S. A Investment Narrative Recap

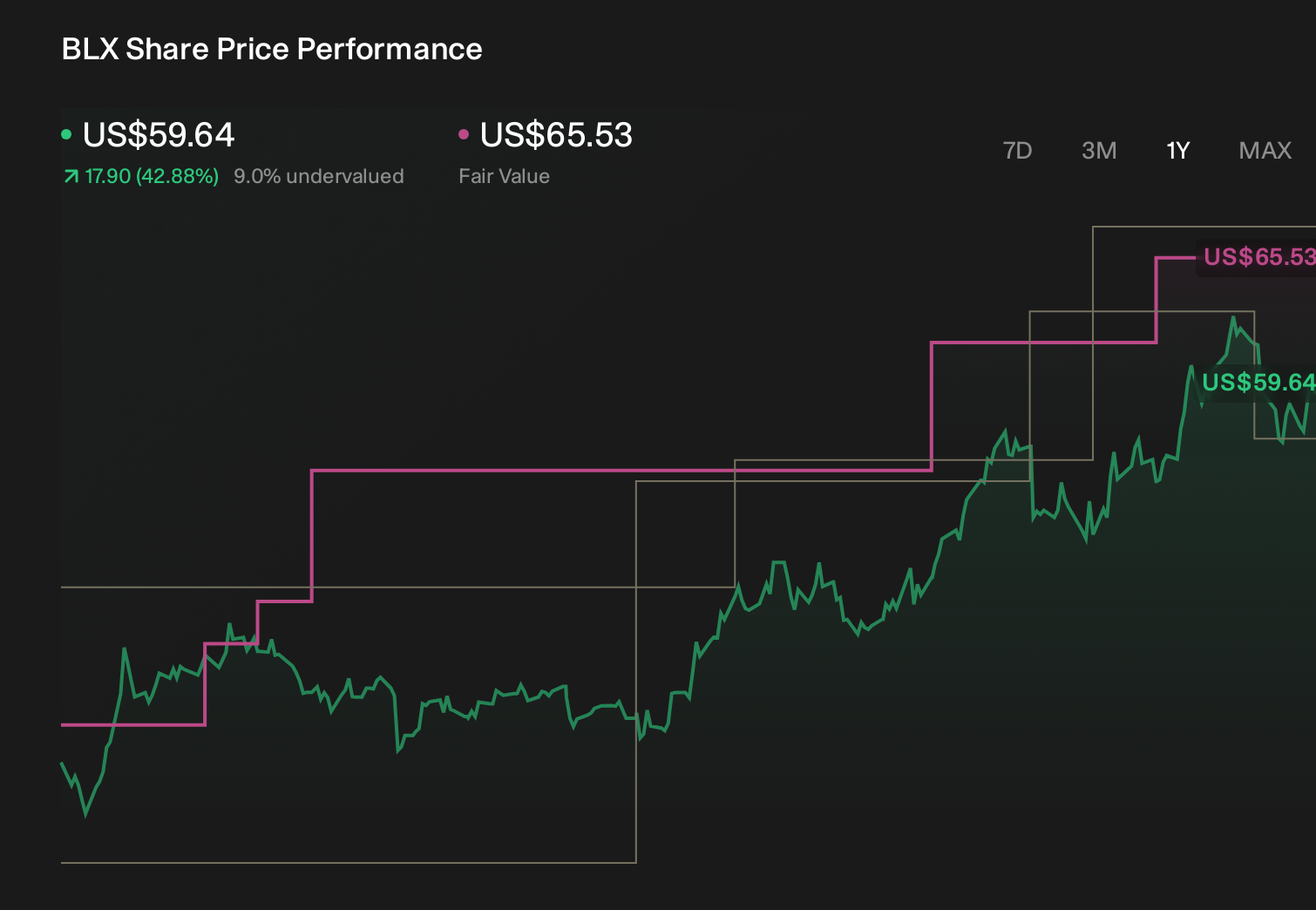

To own Bladex, you need to believe in its role as a specialist trade bank for Latin America, using a growing digital platform, solid asset quality, and deposit-based funding to support fee and interest income. The latest name change, board refresh, and Q1 2026 results slightly reinforce that narrative but do not meaningfully change the key near term catalyst of scaling transactional fees, or the main risk around regional macro and sovereign exposure.

The most relevant update here is the Q1 2026 earnings print, with net interest income at US$70.21 million and net income at US$56.36 million. That income backdrop, together with the affirmed US$0.6875 dividend, matters because it underpins confidence in Bladex’s ability to fund growth in its trade platform while still returning capital, even as investors weigh the risk that regional volatility or concentrated sovereign exposure could pressure those figures.

Yet investors should be aware that heavy exposure to Latin American sovereign and quasi sovereign risk means that if a single key market stumbles...

Read the full narrative on Banco Latinoamericano de Comercio Exterior S. A (it's free!)

Banco Latinoamericano de Comercio Exterior S. A's narrative projects $436.7 million revenue and $276.7 million earnings by 2029. This requires 11.2% yearly revenue growth and about a $49.8 million earnings increase from $226.9 million today.

Uncover how Banco Latinoamericano de Comercio Exterior S. A's forecasts yield a $61.53 fair value, a 15% upside to its current price.

Exploring Other Perspectives

Before this news, the most optimistic analysts were counting on earnings reaching about US$279.2 million by 2028, but if higher regulatory and ESG costs rise faster than expected, that upbeat view could diverge sharply from the more cautious focus on sovereign concentration risk.

Explore 4 other fair value estimates on Banco Latinoamericano de Comercio Exterior S. A - why the stock might be worth as much as 82% more than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Banco Latinoamericano de Comercio Exterior S. A research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Banco Latinoamericano de Comercio Exterior S. A research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Banco Latinoamericano de Comercio Exterior S. A's overall financial health at a glance.

Looking For Alternative Opportunities?

Our top stock finds are flying under the radar-for now. Get in early:

- Find 51 companies with promising cash flow potential yet trading below their fair value.

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 18 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com