- In April 2026, Huntington Bancshares reported first-quarter net income of US$523 million, maintained its US$0.155 quarterly common dividend, detailed a series of preferred stock dividends, and launched a new up-to-US$3.00 billion share repurchase program after completing US$250 million of an earlier buyback.

- The quarter highlighted how the Cadence and Veritex acquisitions drove strong revenue growth and a larger balance sheet while integration costs and higher credit provisions limited earnings progress, all while capital ratios remained above well-capitalized levels.

- We’ll now examine how Huntington’s acquisition-driven revenue growth, tempered by integration expenses and supported by a new buyback, affects its investment narrative.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 18 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Huntington Bancshares Investment Narrative Recap

To own Huntington, you need to believe that its larger, acquisition-fueled footprint in faster-growing markets can offset near-term integration costs and credit provisioning, while digital investments and core relationship banking support steady earnings power. The latest results and capital actions do not materially change that near-term picture: the key catalyst remains clean execution on Cadence and Veritex integration, while the biggest immediate risk is that acquisition-related costs and credit trends weigh on profitability longer than expected.

The new up-to-US$3.0 billion share repurchase authorization is the most relevant recent announcement here, as it sits alongside ongoing common and preferred dividends after US$250 million of buybacks under the prior plan. For investors focused on the integration and margin story, this capital return framework matters because it signals how much financial flexibility Huntington retains while absorbing Cadence and Veritex and managing credit costs.

Yet even with these positives, investors should be aware that concentrated exposure to slower growth Midwest markets could still...

Read the full narrative on Huntington Bancshares (it's free!)

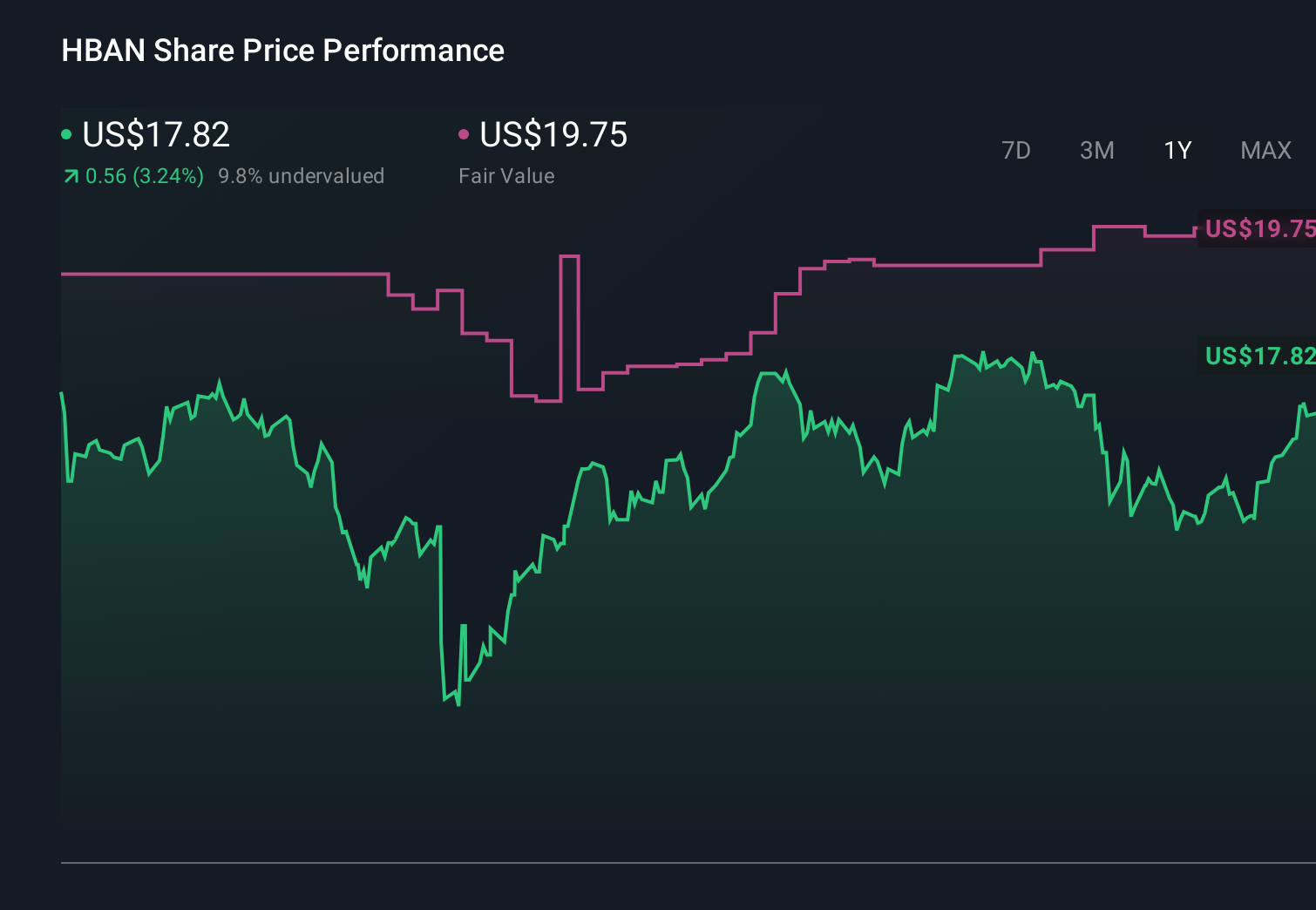

Huntington Bancshares' narrative projects $13.1 billion revenue and $3.7 billion earnings by 2029.

Uncover how Huntington Bancshares' forecasts yield a $19.69 fair value, a 22% upside to its current price.

Exploring Other Perspectives

Three members of the Simply Wall St Community see Huntington’s fair value between US$19.69 and US$33.59, underscoring how far opinions can spread. You should weigh those views against the risk that integration costs and higher provisions continue to pressure reported earnings, which could influence how the larger franchise ultimately performs over time.

Explore 3 other fair value estimates on Huntington Bancshares - why the stock might be worth over 2x more than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Huntington Bancshares research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Huntington Bancshares research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Huntington Bancshares' overall financial health at a glance.

Contemplating Other Strategies?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- The future of work is here. Discover the 34 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Find 48 companies with promising cash flow potential yet trading below their fair value.

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com