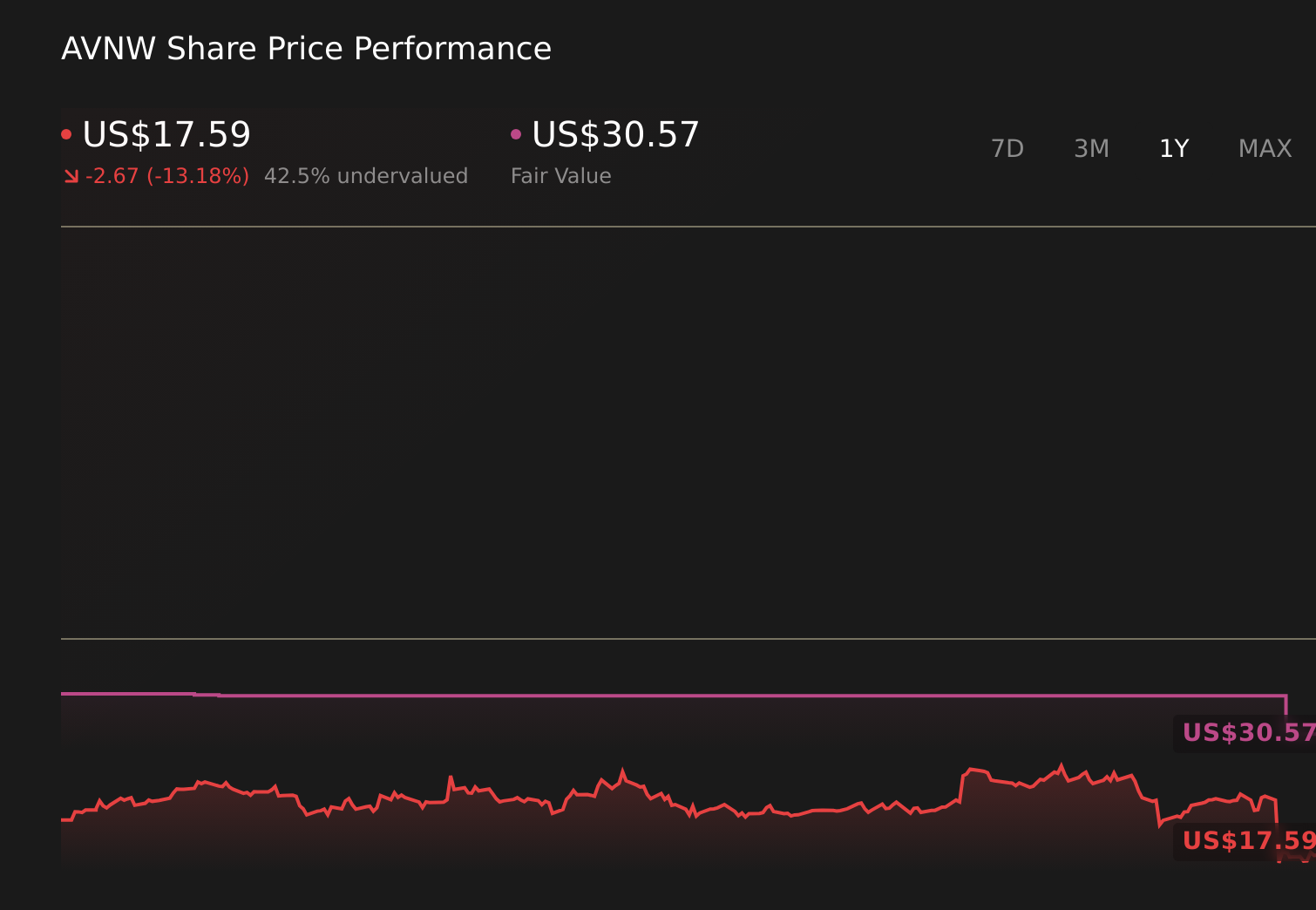

- Aviat Networks, Inc. reported past third-quarter 2026 results showing revenue of US$100.0 million versus US$112.64 million a year earlier, swinging from net income of US$3.53 million to a net loss of US$2.07 million.

- Despite this weaker quarter, Aviat’s nine-month results showed relatively steady revenue at US$318.8 million and a move from a net loss of US$3.86 million to net income of US$3.82 million, alongside updated full-year 2026 revenue guidance of US$428.0 million to US$440.0 million.

- Next, we’ll examine how the latest quarterly loss alongside reaffirmed full-year revenue guidance affects Aviat Networks’ longer-term investment narrative.

Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

Aviat Networks Investment Narrative Recap

To own Aviat Networks, you need to believe its microwave and wireless backhaul niche can translate into consistent earnings, despite volatility in quarterly results and customer spending. The latest quarter’s loss and softer revenue do not appear to alter the nearer term catalyst of integrating Pasolink and ramping newer products, but they do highlight execution risk around margins and reliance on large service provider demand.

The most relevant recent update is Aviat’s revised full year 2026 revenue guidance to US$428.0 million to US$440.0 million, trimmed from earlier guidance but still implying a solid second half relative to the third quarter. How effectively Aviat aligns this outlook with its product roll out and supply chain plans will matter for how investors weigh those catalysts against risks such as tariff exposure and regional weakness.

Yet behind this updated guidance, investors should be aware that Aviat’s dependence on U.S. Tier 1 projects and exposure to shifting telecom technologies could...

Read the full narrative on Aviat Networks (it's free!)

Aviat Networks' narrative projects $505.8 million revenue and $33.4 million earnings by 2028. This requires 5.1% yearly revenue growth and a $35.7 million earnings increase from -$2.3 million today.

Uncover how Aviat Networks' forecasts yield a $34.43 fair value, a 109% upside to its current price.

Exploring Other Perspectives

Before this weaker quarter, the most pessimistic analysts still assumed revenue reaching about US$516.8 million and earnings of US$36.4 million by 2028, yet they stressed that Aviat’s heavy microwave focus could struggle if fiber and newer architectures gain more ground, so this latest loss may prompt you to weigh those downside scenarios even more carefully.

Explore 2 other fair value estimates on Aviat Networks - why the stock might be worth just $16.50!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Aviat Networks research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Aviat Networks research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Aviat Networks' overall financial health at a glance.

Seeking Other Investments?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Find 44 companies with promising cash flow potential yet trading below their fair value.

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com