Kinsale Capital Group (KNSL) stock has been under pressure after investors reacted to concerns about slowing growth in property and casualty insurance and a short seller report questioning its profit margins and policy structure.

See our latest analysis for Kinsale Capital Group.

The recent short seller report and concerns about moderating property and casualty growth have come on top of a weaker trend, with a 30 day share price return of 10.55% and a year to date share price return decline of 21.31%. The 1 year total shareholder return decline of 32.39% contrasts with a 5 year total shareholder return of 98.98%, suggesting long term holders have still seen meaningful gains even as momentum has recently faded.

If the volatility around Kinsale has you reassessing your watchlist, it can help to broaden your search and uncover 18 top founder-led companies

With the stock trading at $308.83 after a 32.39% 1-year total return decline, yet still showing a 5-year total return of 98.98%, you have to ask: is this a reset that creates a buying opportunity, or is the market already factoring in whatever growth lies ahead?

Most Popular Narrative: 13.5% Undervalued

At a last close of $308.83 compared with a narrative fair value of $356.89, the widely followed view frames Kinsale as undervalued while still incorporating more muted growth.

The secular shift of risks from standard markets into the E&S channel, particularly for homeowners and catastrophe-exposed lines (e.g., in California, Texas, and coastal regions), is broadening Kinsale's long-term premium base and enabling sustainable top-line growth even as competition intensifies in select lines.

Want to see what sits behind that valuation gap? The narrative leans heavily on slower premium growth, tighter margins and a re-rated earnings multiple. Curious which assumptions matter most?

Result: Fair Value of $356.89 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that gap relies on assumptions that could be tested if competition keeps pressuring premiums or if catastrophe-exposed homeowners lines drive higher than expected losses.

Find out about the key risks to this Kinsale Capital Group narrative.

Another Angle On The Valuation

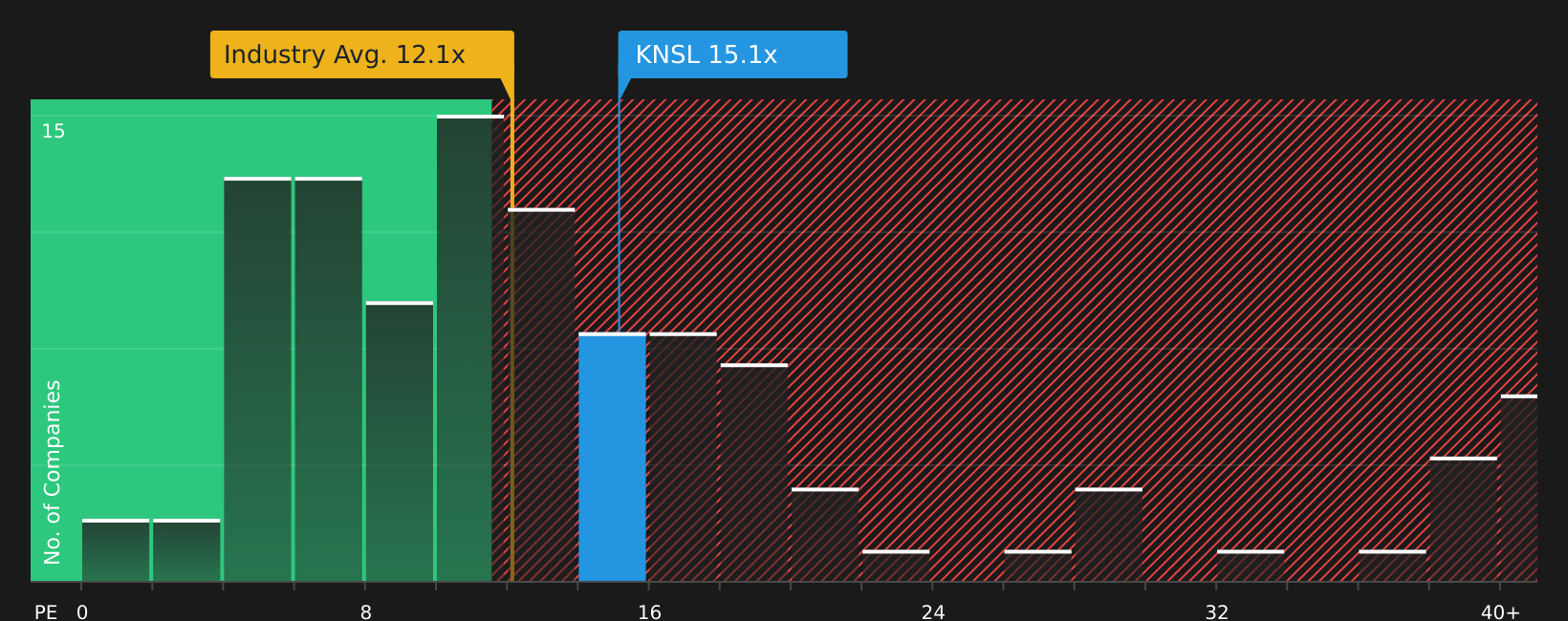

The narrative fair value points to Kinsale as undervalued, yet the current P/E of 13.5x sits above both the US Insurance industry at 11.4x and peers at 7.3x, and above a fair ratio of 11.1x. That premium can signal quality, but also raises the question of how much good news is already in the price.

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Seeing mixed signals on Kinsale so far? Use the current data to move quickly, refine your investment thesis, and evaluate 2 key rewards and 1 important warning sign.

Looking for more investment ideas?

If Kinsale has sharpened your thinking, do not stop here. Use the Simply Wall St Screener to quickly surface fresh opportunities before the crowd focuses on them.

- Target steadier compounders by reviewing companies highlighted in the 72 resilient stocks with low risk scores for potential resilience when conditions change.

- Hunt for value by checking the 51 high quality undervalued stocks and see which stocks combine strong fundamentals with prices that differ from underlying metrics.

- Get ahead of the market by searching the screener containing 23 high quality undiscovered gems that pair solid business quality with lower visibility among investors.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com