- Earlier this week, Teradata Corporation reported Q1 2026 results with revenue of US$444 million and GAAP diluted EPS of US$3.47, lifted by a very large US$480 million settlement from SAP and solid recurring revenue growth.

- Teradata also unveiled its new Autonomous Knowledge Platform, aiming to unify AI, analytics, and data across cloud and on-premises environments to support governed, production-scale AI agents for large enterprises.

- We’ll now examine how the launch of the Autonomous Knowledge Platform may reshape Teradata’s investment narrative around AI-driven workloads.

Outshine the giants: these 16 early-stage AI stocks could fund your retirement.

Teradata Investment Narrative Recap

To own Teradata today, you need to believe that its hybrid data platform can become a credible home for enterprise AI workloads, with recurring, cloud-centric revenue offsetting pressure in legacy services. The Autonomous Knowledge Platform sharpens that AI narrative, but near term the key catalyst remains execution on cloud ARR growth, while the biggest risk is still competitive pressure from hyperscalers and open-source alternatives. The SAP settlement materially boosts earnings but does not resolve those structural challenges.

The Autonomous Knowledge Platform announcement is most relevant here because it directly targets AI-driven, multi-cloud, and sovereign data use cases that underpin Teradata’s growth story. By bringing AI Studio, Tera, and Teradata Cloud/Factory under one governed architecture, the company is positioning its platform for production-grade AI agents rather than pilots, which ties closely to the consensus catalyst of AI adoption and could influence how investors weigh that against ongoing revenue headwinds and competitive risk.

Yet even with this AI push, investors should be aware that intensifying price competition and Teradata’s legacy reputation could still...

Read the full narrative on Teradata (it's free!)

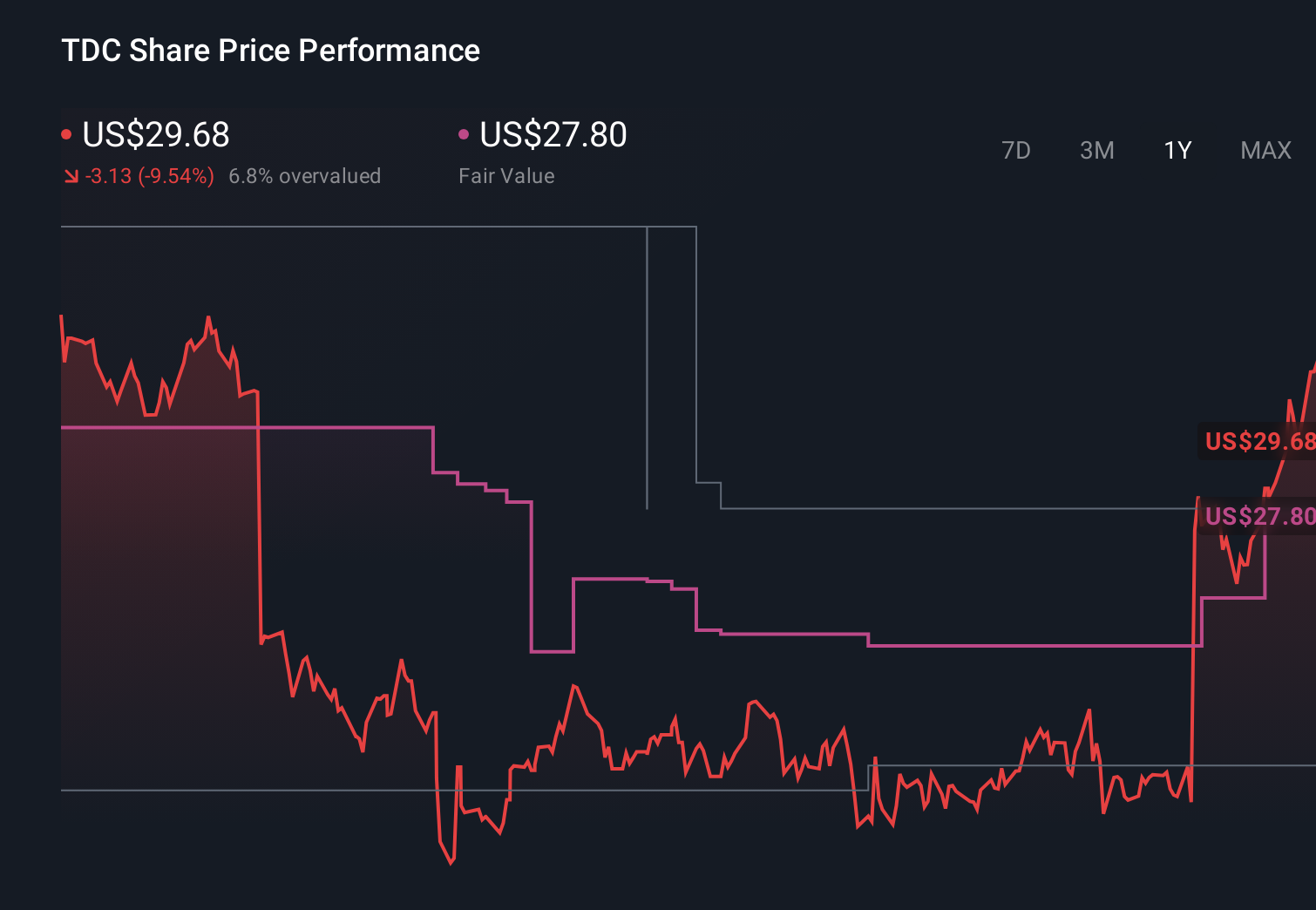

Teradata's narrative projects $1.7 billion revenue and $173.0 million earnings by 2029. This assumes fairly flat yearly revenue growth and an earnings increase of about $43 million from $130.0 million today.

Uncover how Teradata's forecasts yield a $33.78 fair value, a 14% upside to its current price.

Exploring Other Perspectives

Before this launch, the most pessimistic analysts were modeling Teradata’s revenue to shrink about 2% a year and earnings to fall to roughly US$87 million, so if you are weighing this news against those concerns about rapid cloud consolidation and price pressure, it is worth considering how far apart reasonable views on the stock can be and how new AI products might shift that spread over time.

Explore 5 other fair value estimates on Teradata - why the stock might be worth 29% less than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Teradata research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Teradata research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Teradata's overall financial health at a glance.

Seeking Other Investments?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

- AI is about to change healthcare. These 35 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Rare earth metals are the new gold rush. Find out which 33 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com