Why NCR Atleos (NATL) is on investors’ radar

NCR Atleos (NATL) has caught investor attention after its latest reported figures, showing revenue of US$4.4b and net income of US$170.0m, alongside a value score of 1 and recent share price moves.

See our latest analysis for NCR Atleos.

At a share price of US$44.25, NCR Atleos has seen an 18.86% year to date share price return and a 60.73% total shareholder return over the past year. This suggests momentum has been building as investors reassess growth prospects and risks.

If this kind of move has you thinking about what else is out there, it could be a good moment to scan for other opportunities using our 18 top founder-led companies

With NCR Atleos trading at US$44.25, carrying a value score of 1 and a price target of about US$50, the key question is simple: is the stock cheap, or is the market already pricing in future growth?

Most Popular Narrative: 12% Undervalued

With NCR Atleos last closing at $44.25 against a narrative fair value of about $50.27, the current pricing sits below what this widely followed view considers reasonable based on its long term potential.

High recurring revenue mix (over 70% in Q2), significant productivity gains through AI-driven service optimization, and a rapidly scaling backlog are driving strong margin expansion and robust free cash flow, underpinning announced share buybacks and sustained EPS growth, suggesting current valuation does not reflect enhanced long-term earnings power.

Want to see how recurring revenue, margin ambitions and a lower future P/E all feed into that fair value? The key assumptions sit inside this narrative, including how earnings and cash flow are expected to evolve and what sort of valuation multiple has to hold up to make $50.27 stack up.

Result: Fair Value of $50.27 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, you still need to weigh up the risk that faster digital banking adoption and rising fintech competition will chip away at ATM demand and pressure margins.

Find out about the key risks to this NCR Atleos narrative.

Another Angle On Valuation

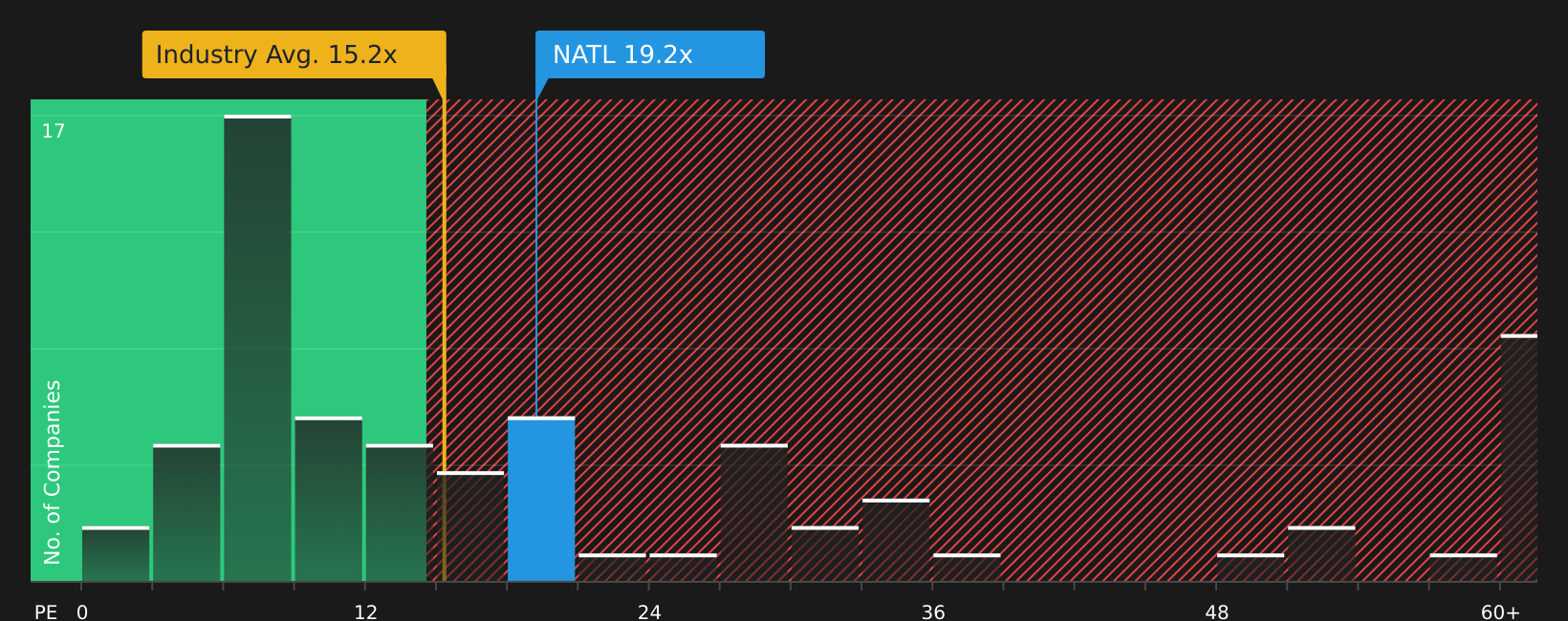

The narrative fair value of about $50.27 paints NCR Atleos as undervalued, but the price tag looks different once earnings multiples are brought into the picture. At a P/E of 19.2x, the stock sits slightly above the US Diversified Financial industry at 18.5x and well above its peer average of 6.9x.

Compared with an estimated fair ratio of 20.8x, the current 19.2x does not appear stretched. However, the wide gap to peers suggests limited room for error if growth or margins fall short. With those cross currents in mind, which signal feels more useful to you right now: the story or the sticker price?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Mixed messages or clear opportunity? With both risks and rewards in play, it makes sense to look through the data yourself and move quickly to form your own view. You can start with 2 key rewards and 2 important warning signs

Looking for more investment ideas?

If NCR Atleos has sharpened your focus, do not stop here. Use carefully filtered stock ideas to broaden your watchlist and sharpen your next move.

- Target higher potential returns with steady fundamentals by scanning a curated set of screener containing 23 high quality undiscovered gems before others catch on.

- Prioritize resilience by reviewing 71 resilient stocks with low risk scores that aim to keep volatility and balance sheet concerns in check.

- Balance offense and defense by using the 12 dividend fortresses to spot income ideas that could complement more growth focused positions.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com