Stellar Bancorp’s latest earnings snapshot

Stellar Bancorp (STEL) recently reported first quarter results, highlighting net interest income of US$105.93 million and net income of US$26.97 million compared with the same period last year, drawing fresh attention to the stock.

See our latest analysis for Stellar Bancorp.

At a share price of US$37.46, Stellar Bancorp has delivered a year to date share price return of 21.78% and a 1 year total shareholder return of 40.98%. However, the 90 day share price performance has eased 5.16%, which may suggest that enthusiasm has cooled after a period of strong performance that coincided with improving quarterly earnings.

If you are weighing bank stocks against other themes in your portfolio, it can be useful to broaden your search and look at 19 top founder-led companies

With earnings per share at US$0.53 and the stock trading just below a US$38 analyst target, the key question now is whether Stellar Bancorp still offers a buying opportunity or if the market is already pricing in future growth.

Most Popular Narrative: 1% Undervalued

With Stellar Bancorp trading at $37.46 against a narrative fair value of $38, the spread is small, yet the story behind that estimate is detailed.

The current valuation seems to assume continued organic loan growth and sustained market share gains, banking on robust Texas/Southwest economic trends and small business expansion, while underestimating risk from geographic concentration and potential regional economic downturns that could pressure loan growth and future earnings. Investors seem to discount the challenge of rising compliance, technology, and ESG-related costs, as increased regulatory and stakeholder requirements may outpace operational leverage improvements, resulting in longer-term net margin compression.

Curious what earnings path and margin profile sit behind that small gap to fair value? The narrative leans on detailed growth, profitability, and valuation assumptions that could reshape how you view the stock.

Result: Fair Value of $38 (ABOUT RIGHT)

Have a read of the narrative in full and understand what's behind the forecasts.

However, investors still need to factor in execution risk around merger synergies and the cost of keeping up with compliance and technology, which could challenge this fair value story.

Find out about the key risks to this Stellar Bancorp narrative.

Another Angle on Valuation

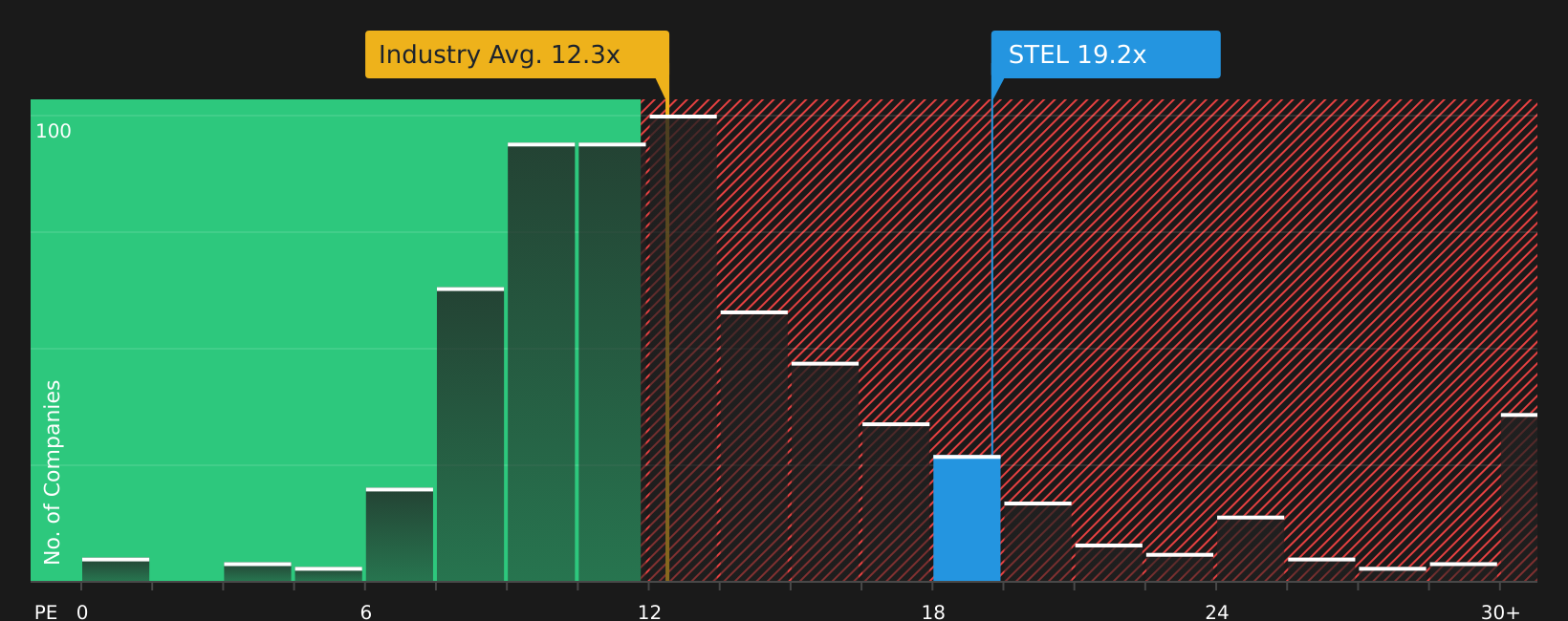

Analysts frame Stellar Bancorp around a fair value of $38, yet the current P/E of 18.1x sits well above both the US Banks industry at 11.4x and a fair ratio of 11.3x. That gap points to valuation risk rather than a clear bargain. How comfortable are you paying this kind of premium?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

If this mix of optimism and caution feels familiar, now may be a good time to review the numbers yourself and evaluate the story from both sides using the 2 key rewards and 1 important warning sign

Looking for more investment ideas?

If this analysis has sharpened your thinking, do not stop here. Use the tools available to line up your next potential opportunity with clear criteria.

- Target strong cash generation and quality balance sheets by scanning 49 high quality undervalued stocks that may warrant a closer look.

- Prioritize resilience and capital preservation by reviewing 71 resilient stocks with low risk scores that could help steady your overall portfolio.

- Spot potential early movers by checking screener containing 21 high quality undiscovered gems before they attract wider market attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com