- In April 2026, EMCOR Group reported first‑quarter 2026 results showing sales of US$4,628.23 million, net income of US$305.48 million, and diluted EPS of US$6.84, and it raised full‑year 2026 revenue guidance to US$18.50–US$19.25 billion with diluted EPS guidance of US$28.25–US$29.75.

- These results were supported by strong demand across data center, healthcare, and institutional projects, contributing to record remaining performance obligations and reinforcing EMCOR’s position in complex, mission‑critical construction and services work.

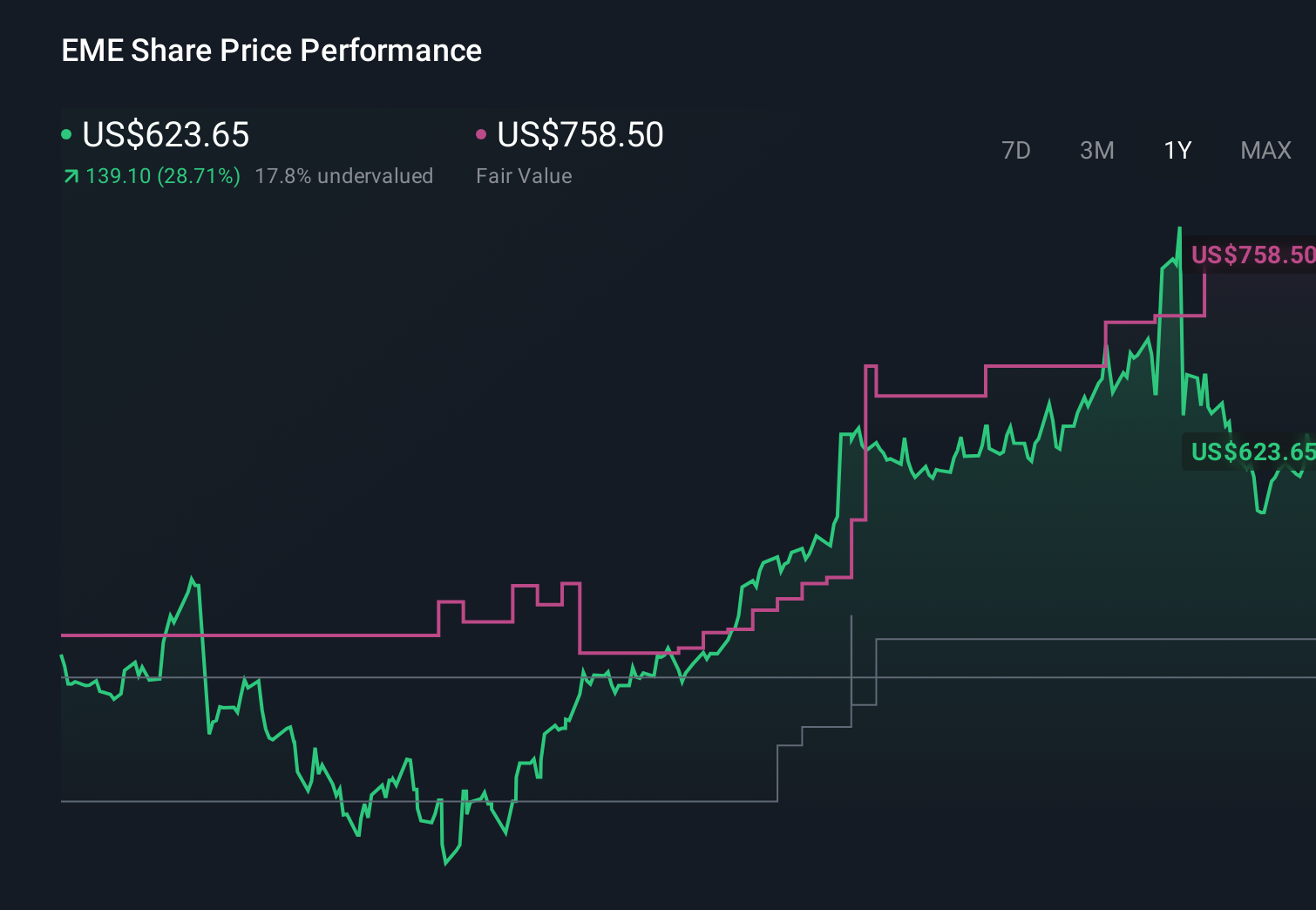

- We’ll now examine how EMCOR’s raised 2026 revenue and earnings guidance may influence the existing investment narrative and risk balance.

The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

EMCOR Group Investment Narrative Recap

To own EMCOR Group, you need to believe that its strength in complex, mission‑critical projects can convert today’s record remaining performance obligations into durable earnings, while controlling labor and integration costs. The raised 2026 guidance, supported by data center, healthcare, and institutional demand, reinforces the near‑term catalyst of converting backlog into revenue, but it does not remove the key risks around labor availability, wage inflation, and exposure to cyclical industrial and oil and gas end markets.

Against this backdrop, EMCOR’s decision to raise full‑year 2026 revenue guidance to US$18.50–US$19.25 billion and diluted EPS guidance to US$28.25–US$29.75 is particularly relevant. It directly ties the current earnings beat and record RPOs to the existing catalyst of large project execution, while leaving longer‑term questions about labor costs, high‑tech manufacturing volatility, and integration of acquisitions such as Miller Electric very much in focus.

Yet even with higher 2026 guidance, investors should be aware that EMCOR’s reliance on cyclical end markets could still...

Read the full narrative on EMCOR Group (it's free!)

EMCOR Group's narrative projects $20.6 billion revenue and $1.5 billion earnings by 2029.

Uncover how EMCOR Group's forecasts yield a $887.00 fair value, a 5% downside to its current price.

Exploring Other Perspectives

Before this update, the most optimistic analysts were already modeling about US$21.2 billion of revenue and US$1.4 billion of earnings by 2028, so if you lean toward that more bullish view of EMCOR’s ability to turn complex data center and institutional demand into sustained profit growth, this latest guidance raise may either support your thesis or prompt you to rethink how much execution and cyclicality risk you are really comfortable with.

Explore 5 other fair value estimates on EMCOR Group - why the stock might be worth 29% less than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your EMCOR Group research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free EMCOR Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate EMCOR Group's overall financial health at a glance.

Searching For A Fresh Perspective?

Our top stock finds are flying under the radar-for now. Get in early:

- Find 48 companies with promising cash flow potential yet trading below their fair value.

- Uncover the next big thing with 26 elite penny stocks that balance risk and reward.

- AI is about to change healthcare. These 32 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com