Recent share performance puts W. P. Carey in focus

W. P. Carey (WPC) is drawing attention after a total return of 31.7% over the past year and 38.0% over five years, prompting investors to reassess the stock’s role in income-focused portfolios.

See our latest analysis for W. P. Carey.

The recent 1-month share price return of 4.34% and year-to-date share price return of 15.22% at a last close of US$74.73 suggest momentum has been building on top of the 31.66% 1-year total shareholder return.

If you are weighing W. P. Carey against other income ideas, it can help to see what else is working in listed real assets and related sectors via 20 top founder-led companies

With W. P. Carey trading near its analyst price target and flagged with a value score of 4, despite an indicated 52.6% intrinsic discount, the key question is whether there is still a buying opportunity or if the market is already pricing in future growth.

Most Popular Narrative: 10% Undervalued

The most followed narrative for W. P. Carey pegs fair value at about $74.83, almost level with the last close at $74.73, yet still framing the stock as modestly undervalued.

Sustained demand for distribution and logistics space, driven by continued e-commerce expansion and supply chain investments, is fueling strong investment in industrial and warehouse assets. This is reflected in W. P. Carey's pivot to close to 100% industrial in new investments and a pipeline that is predominantly industrial, supporting future revenue and NOI growth. Significant lease structures feature inflation-linked escalators (CPI-based) and higher fixed annual bumps (around 2.8% on recent deals), enabling robust same-store rent growth even in a stable inflation environment and directly enhancing rental revenues and overall earnings.

Curious how a portfolio tilt toward industrial assets, paired with inflation-linked rent bumps and higher fixed escalators, gets baked into that fair value story? The narrative focuses on earnings expansion, margin uplift, and a future earnings multiple that you can review in detail, tied to specific revenue and profit assumptions that are laid out in full.

Result: Fair Value of $74.83 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this story can shift quickly if tenant defaults rise on single-tenant properties or if property sales slow, which would limit capital for new, higher-yield deals.

Find out about the key risks to this W. P. Carey narrative.

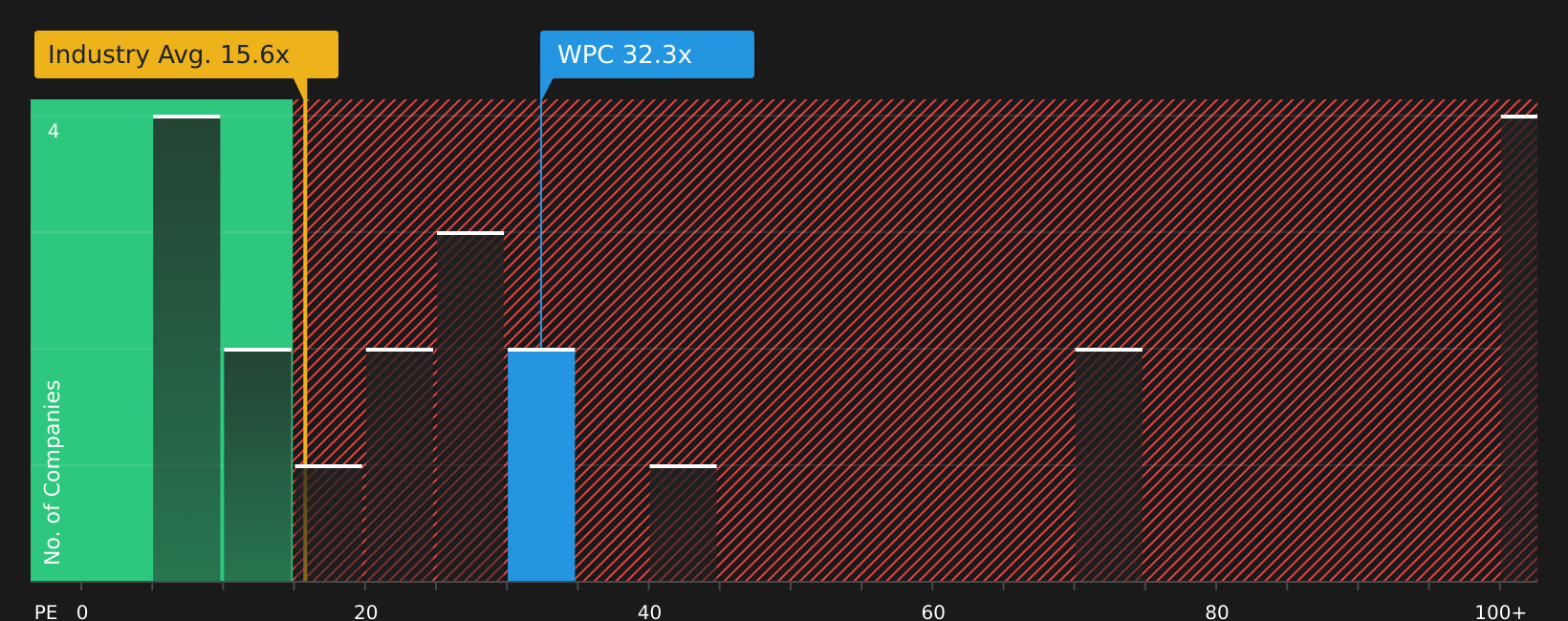

Another View: What Earnings Ratios Say

While analysts and the SWS fair value model point to W. P. Carey trading at a 52.6% discount to an intrinsic value of $157.56, the current P/E of 32.2x paints a more cautious picture against the global REITs average of 15.7x and a fair ratio of 36.9x. That combination of apparent discount and richer multiple versus the wider sector leaves you with a clear tension: is this a value opportunity or a valuation trap if sentiment shifts?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With that mix of optimism and caution in mind, move quickly to review the underlying data, stress test your thesis, and weigh the stock's 3 key rewards and 2 important warning signs.

Looking for more investment ideas?

If you stop with just one stock, you risk missing other opportunities that might suit your goals even better, so put a few more ideas on your radar.

- Target higher income potential with companies that appear built for steady cash returns by reviewing 13 dividend fortresses.

- Hunt for quality at sensible prices by scanning 45 high quality undervalued stocks where strong fundamentals and attractive valuations meet.

- Spot opportunities others may be overlooking by checking the screener containing 22 high quality undiscovered gems before they attract wider attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com