The United States market has experienced a notable upswing, rising 1.5% over the last week and climbing 26% in the past year, with earnings projected to grow by 17% annually. In this thriving environment, identifying stocks that are poised for growth yet remain underappreciated can offer intriguing opportunities for investors seeking to capitalize on emerging potential.

Top 10 Undiscovered Gems With Strong Fundamentals In The United States

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| New Peoples Bankshares | 22.84% | 4.06% | 9.72% | ★★★★★★ |

| Security Federal | 18.41% | 5.46% | -0.53% | ★★★★★★ |

| Tri-County Financial Group | 54.21% | -0.70% | -10.52% | ★★★★★★ |

| Cashmere Valley Bank | 31.63% | 5.07% | 1.43% | ★★★★★★ |

| ASA Gold and Precious Metals | NA | 12.65% | 41.20% | ★★★★★★ |

| First Northern Community Bancorp | NA | 7.26% | 11.00% | ★★★★★★ |

| Affinity Bancshares | 41.71% | 1.36% | -0.22% | ★★★★★★ |

| Winchester Bancorp | 123.28% | 9.14% | -54.82% | ★★★★★★ |

| Oxford Bank | 12.42% | 13.91% | 2.78% | ★★★★☆☆ |

| High Templar Tech | 13.55% | -66.76% | -26.62% | ★★★★☆☆ |

Let's explore several standout options from the results in the screener.

Artesian Resources (ARTN.A)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Artesian Resources Corporation offers water, wastewater, and related services in Delaware, Maryland, and Pennsylvania with a market capitalization of $333.03 million.

Operations: Artesian Resources generates revenue primarily from its water and wastewater services in Delaware, Maryland, and Pennsylvania. The company focuses on cost management to optimize its operations. Its net profit margin reflects the efficiency of its business model in managing expenses relative to revenue.

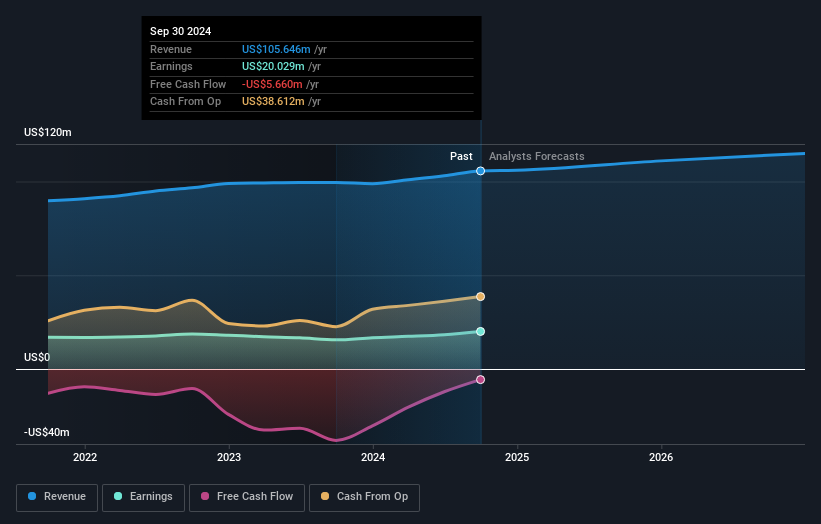

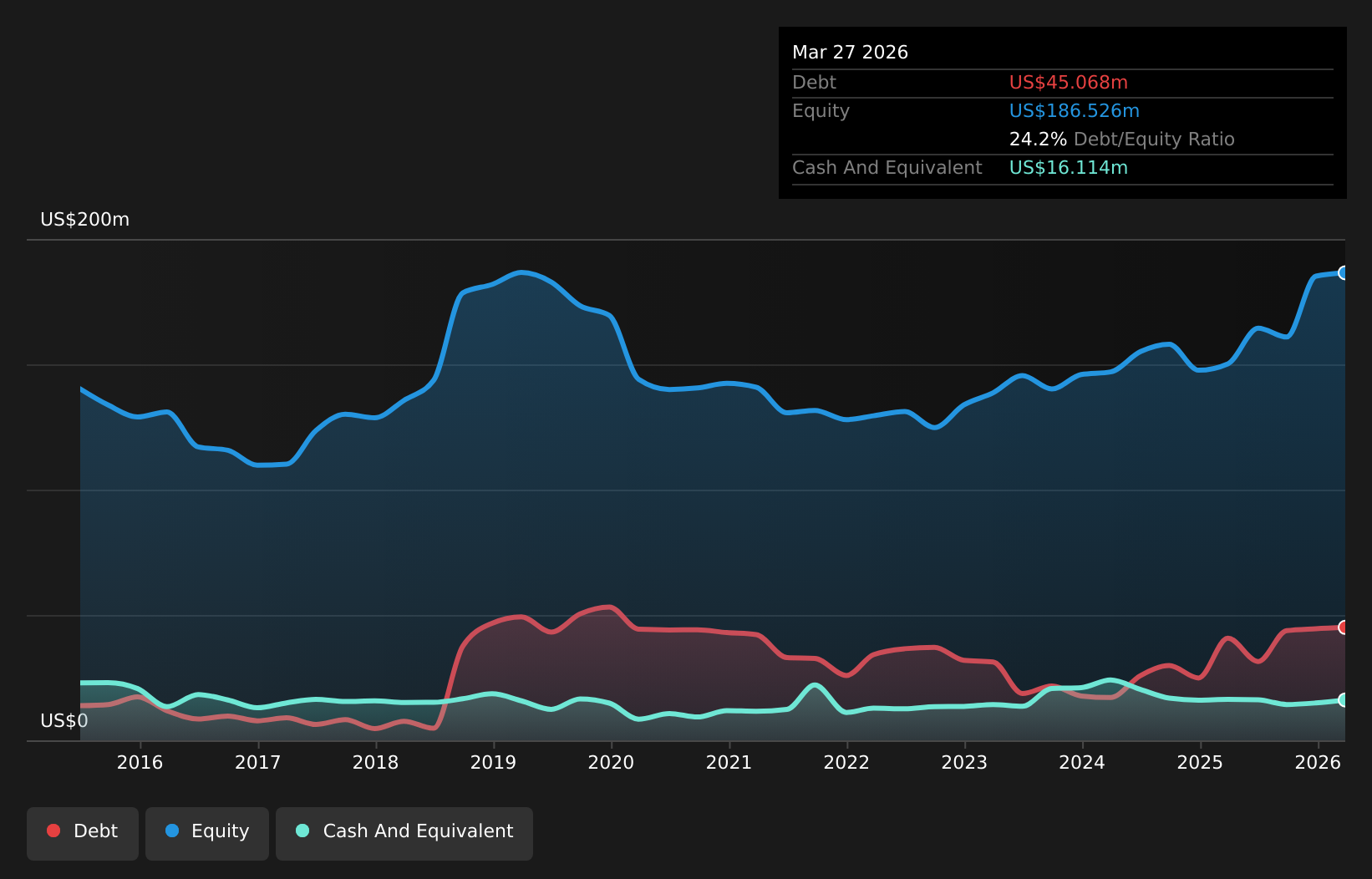

Artesian Resources, a modestly sized player in the water utilities sector, has been making waves with its impressive financial performance. The company's earnings grew by 8.9% over the past year, outpacing the industry average of 2.9%. This growth is supported by a solid net income increase to US$5.93 million in Q1 2026 from US$5.44 million a year ago and an elevated basic earnings per share of US$0.58 compared to US$0.53 previously. Despite its high net debt to equity ratio at 72.5%, Artesian's interest payments are well-covered with EBIT at 4.2x coverage, showcasing robust financial management amidst insider selling concerns.

TrustCo Bank Corp NY (TRST)

Simply Wall St Value Rating: ★★★★★★

Overview: TrustCo Bank Corp NY, with a market cap of $847.70 million, operates as the holding company for Trustco Bank, offering personal and business banking services to individuals and businesses.

Operations: TrustCo Bank Corp NY generates revenue primarily through its community banking segment, which accounted for $189.87 million. The company's net profit margin is a key financial metric to consider when evaluating its profitability.

TrustCo Bank Corp NY, a smaller financial entity, showcases robust financial health with $6.5 billion in total assets and $670.9 million in equity. It holds $5.7 billion in deposits against $5.2 billion in loans, reflecting its strong deposit base as a primary funding source—97% of liabilities are low-risk customer deposits. The bank's allowance for bad loans is ample at 247%, with non-performing loans at just 0.4%. Earnings surged by 23.9% last year, outpacing industry growth of 22.6%. Recently, the company repurchased shares worth $22.82 million, indicating confidence in its valuation strategy.

Twin Disc (TWIN)

Simply Wall St Value Rating: ★★★★★★

Overview: Twin Disc, Incorporated specializes in designing, manufacturing, and selling marine and heavy-duty off-highway power transmission equipment across various international markets with a market cap of $266.80 million.

Operations: Twin Disc generates revenue primarily through the sale of marine and heavy-duty off-highway power transmission equipment across multiple international markets. The company's cost structure includes manufacturing expenses, which significantly impact its profitability. It has a market capitalization of $266.80 million.

Twin Disc, a nimble player in the machinery sector, showcases robust financial health with a net debt to equity ratio of 15.5%, indicating prudent management of leverage. Its earnings have surged by an impressive 541% over the past year, far outpacing industry growth. The company’s EBIT covers interest payments 4.6 times over, reflecting solid operational performance. Recent results highlight sales climbing to US$96.69 million for Q3 compared to US$81.24 million last year and net income swinging from a loss of US$1.47 million to a profit of US$3.33 million, signaling strong recovery and potential for future gains in profitability amidst competitive pressures and economic cycles.

Seize The Opportunity

- Click here to access our complete index of 340 US Undiscovered Gems With Strong Fundamentals.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com