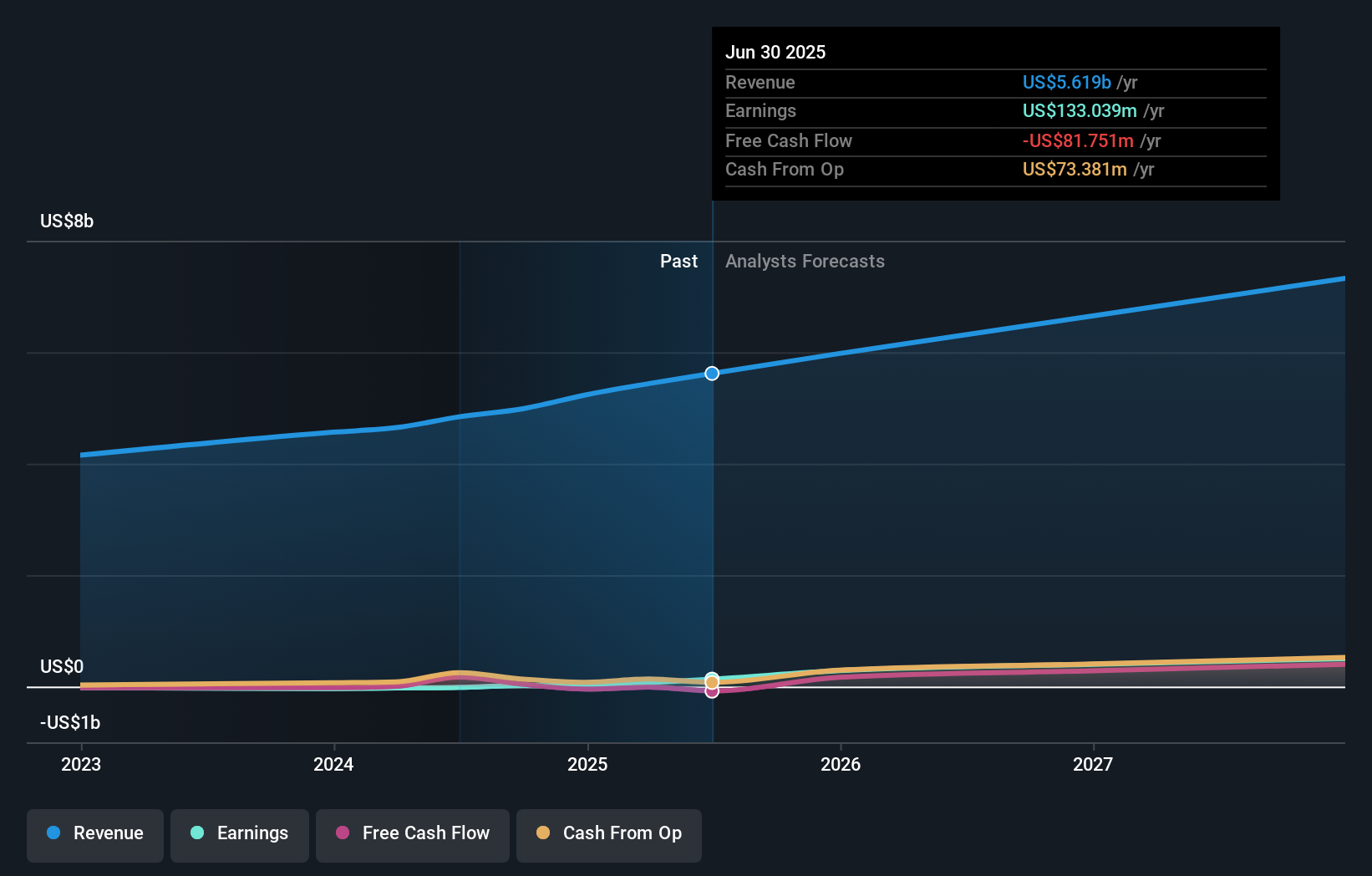

- In early May 2026, StandardAero, Inc. reported first-quarter 2026 results showing sales of US$1,626.86 million and net income of US$79.93 million, alongside raised full-year revenue guidance of US$6.33 billion to US$6.45 billion that reflects the planned removal of US$300 million to US$400 million in pass-through material revenue.

- Management also highlighted ongoing M&A activity, including the Unified Turbines acquisition, and reiterated its intent to balance organic investment, license expansions and opportunistic share repurchases under a disciplined capital allocation framework.

- Next, we’ll examine how the upgraded guidance, underpinned by margin expansion and M&A, affects StandardAero’s longer-term investment narrative.

The future of work is here. Discover the 30 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

StandardAero Investment Narrative Recap

To stay invested in StandardAero, you need to believe in a long runway of recurring engine MRO demand, improving margins and disciplined capital deployment. The latest results and guidance upgrade support that thesis, and appear to reinforce the near term catalyst of margin expansion rather than change it, while the key risk remains whether supply chain constraints and program learning curves can sustain recent profitability improvements.

The raised 2026 revenue guidance to US$6.325 billion to US$6.450 billion, even after removing US$300 million to US$400 million of pass through material revenue, is the clearest link to the story here, because it directly ties to the short term catalyst of cleaner, higher quality margins and the risk that softer demand or pricing could make slower headline growth more visible.

Yet investors should still be aware that if structural contract changes coincide with any cooling in end market demand, then...

Read the full narrative on StandardAero (it's free!)

StandardAero's narrative projects $7.3 billion revenue and $549.2 million earnings by 2028. This requires 7.4% yearly revenue growth and a $364.5 million earnings increase from $184.7 million today.

Uncover how StandardAero's forecasts yield a $35.50 fair value, a 33% upside to its current price.

Exploring Other Perspectives

Four Simply Wall St Community fair value estimates for StandardAero cluster tightly between US$33.70 and US$35.89, signaling relatively aligned expectations among private investors. You should weigh these against the current focus on higher margin LEAP and CFM56 work, which could be tested if supply chain issues or learning curve delays alter the earnings mix.

Explore 4 other fair value estimates on StandardAero - why the stock might be worth just $33.70!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your StandardAero research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free StandardAero research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate StandardAero's overall financial health at a glance.

Seeking Other Investments?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- This technology could replace computers: discover 27 stocks that are working to make quantum computing a reality.

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com