Stock performance snapshot

Whirlpool (WHR) has drawn investor attention after a steep share price slide, with the stock down about 6% over the past day, 11% over the past week, and 28% over the past month.

See our latest analysis for Whirlpool.

The recent slide adds to a wider retreat in Whirlpool’s stock, with the share price return down sharply over the past quarter and long term total shareholder returns also significantly weaker. This suggests that momentum has been fading for some time.

If this kind of abrupt reset has you thinking about where else value might emerge next, it could be a good time to scan 19 top founder-led companies

With Whirlpool stock falling hard while trading at an implied discount to some analyst targets and certain intrinsic estimates, the key question for you is simple: Is this a genuine value entry point, or is the market already factoring in the company’s future growth?

Most Popular Narrative: 41.8% Undervalued

Whirlpool’s most followed narrative pegs fair value at $68.73 per share, compared with the latest close at $39.99. This frames a sizeable valuation gap for investors to assess.

Recent and ongoing restructuring, cost takeout programs, and supply chain efficiencies are expected to deliver structural operating margin improvement, even as current headwinds fade. Strengthened domestic U.S. manufacturing footprint positions Whirlpool to be a primary beneficiary of forthcoming tariff implementation, which will improve competitive positioning, support pricing power, and drive margin recovery as imported inventory clears and trade policies take full effect.

Curious what kind of revenue run rate, profit margin lift, and future earnings multiple are baked into that fair value line? The full narrative spells out the growth path, the profitability reset, and the valuation hurdle analysts think Whirlpool needs to clear to justify a price meaningfully above today’s level.

Result: Fair Value of $68.73 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, softer appliance shipment data and trimmed long term earnings estimates could also signal that weaker demand or sustained margin pressure are challenging that undervalued thesis.

Find out about the key risks to this Whirlpool narrative.

Another Angle on Whirlpool’s Valuation

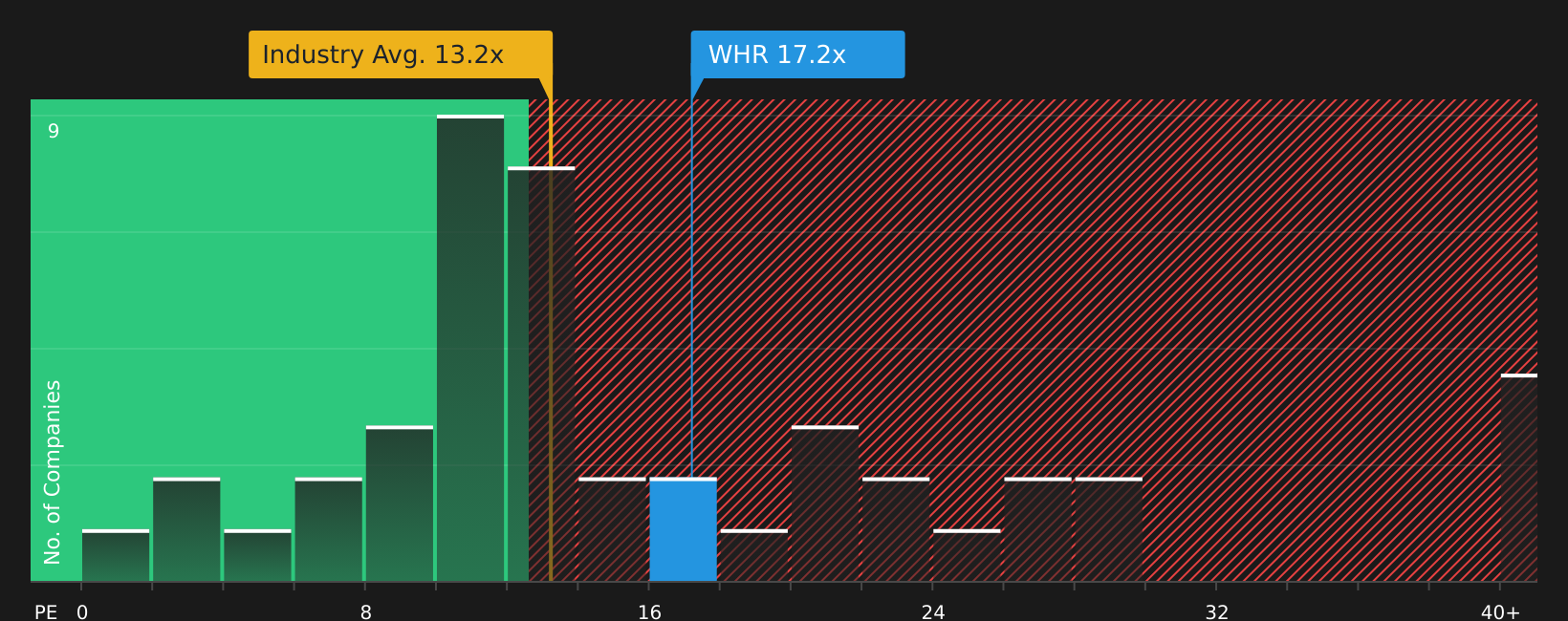

The fair value narrative presents Whirlpool as undervalued at $39.99. However, the current P/E of 16x is higher than both direct peers at 11.8x and the broader US Consumer Durables group at 11.7x, while the fair ratio is calculated at 27.2x. Is that a mispricing you want to lean into, or a sign that the first model may be too optimistic?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With all this mixed sentiment around Whirlpool, it makes sense to move quickly, review the data for yourself, and weigh both the upside and downside using 3 key rewards and 4 important warning signs

Looking for more investment ideas?

If Whirlpool has your attention, do not stop here. Fresh opportunities are always emerging, and skipping them could mean missing the setups that better fit your goals.

- Target potential value opportunities by scanning companies that our process tags as 49 high quality undervalued stocks to see which ones align with your risk and return expectations.

- Strengthen the quality of your watchlist by focusing on businesses highlighted in the solid balance sheet and fundamentals stocks screener (45 results) so you can prioritize financial resilience.

- Get ahead of the crowd by reviewing the screener containing 22 high quality undiscovered gems and spot stocks that are already backing strong fundamentals before they attract wider attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com