- Tutor Perini Corporation recently reported first-quarter 2026 results, with sales rising to US$1,389.46 million from US$1,246.63 million a year earlier, while net income eased to US$25.7 million and diluted earnings per share from continuing operations slipped to US$0.48 from US$0.53.

- Alongside these mixed earnings trends, the company affirmed a quarterly dividend of US$0.06 per share payable on June 4, 2026, signaling an ongoing commitment to returning cash to shareholders despite lower profit.

- We’ll now explore how Tutor Perini’s higher quarterly sales but softer earnings and maintained dividend policy affect its existing investment narrative.

AI is about to change healthcare. These 32 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Tutor Perini Investment Narrative Recap

To own Tutor Perini today, you need to believe its large backlog and infrastructure exposure can translate into steadier profits despite ongoing project and cost risks. The latest quarter supports that basic thesis, with higher sales but slightly lower earnings, and does not materially change the near term focus on execution quality as the key catalyst and legacy contract issues as the main risk.

The most relevant recent announcement here is the reaffirmed US$0.06 quarterly dividend, which sits alongside earlier 2026 guidance that pointed to double digit revenue growth and “strong earnings.” Together, these updates frame a story where management is signalling confidence in cash generation, even as investors watch closely to see if growing revenues can translate into more consistent profitability.

Yet behind the higher sales, investors should be aware of the lingering risk that large, complex projects can still…

Read the full narrative on Tutor Perini (it's free!)

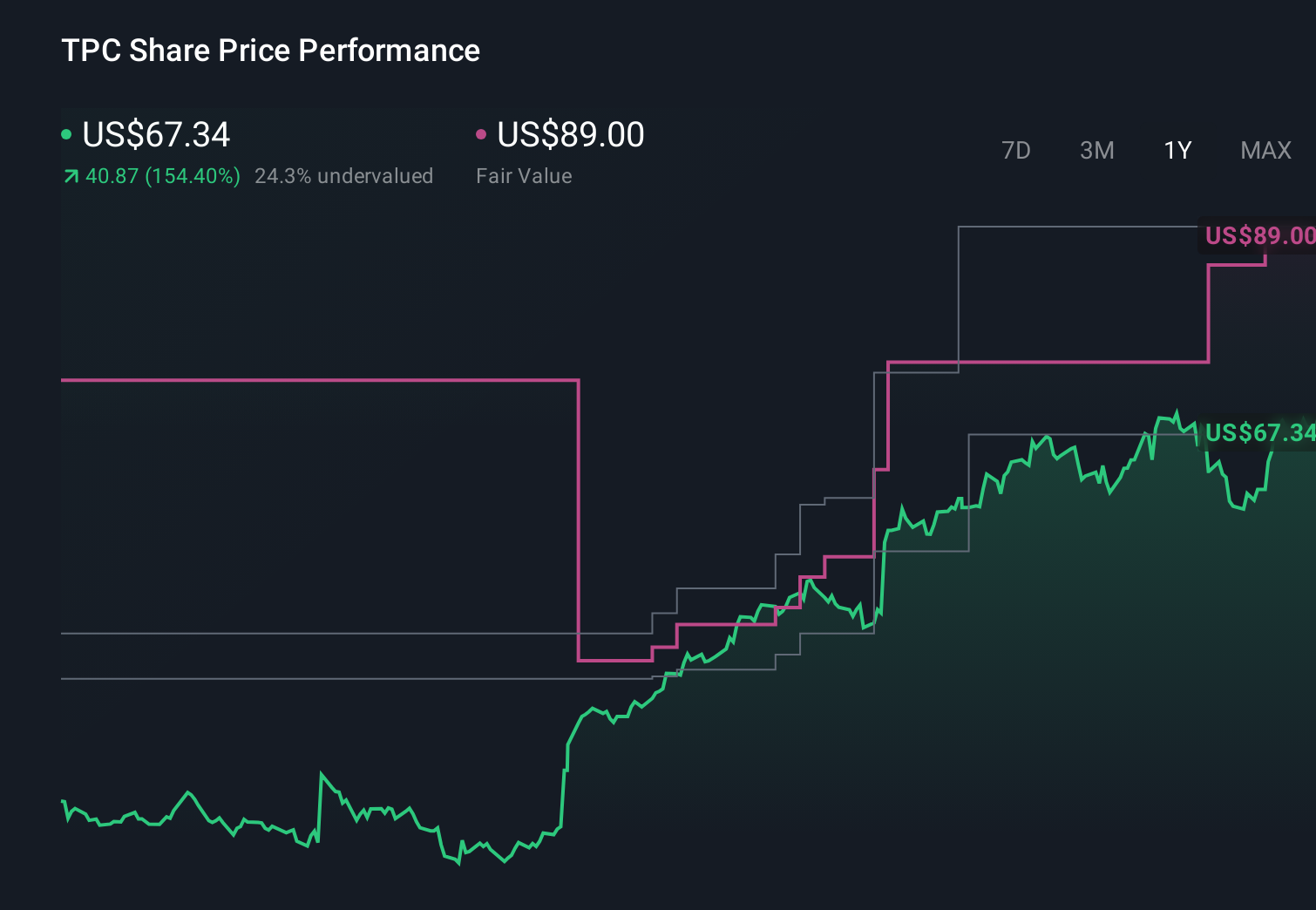

Tutor Perini's narrative projects $7.8 billion revenue and $428.4 million earnings by 2029. This requires 12.2% yearly revenue growth and an earnings increase of about $348 million from $80.4 million today.

Uncover how Tutor Perini's forecasts yield a $109.50 fair value, a 38% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already more cautious, assuming revenue of about US$7.9 billion and earnings of roughly US$300 million by 2029, so this mixed quarter could either soften or reinforce their view that rising costs and execution risks deserve more weight than the upbeat backlog story.

Explore 5 other fair value estimates on Tutor Perini - why the stock might be worth just $84.42!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Tutor Perini research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Tutor Perini research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Tutor Perini's overall financial health at a glance.

Searching For A Fresh Perspective?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Find 50 companies with promising cash flow potential yet trading below their fair value.

- The future of work is here. Discover the 30 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com