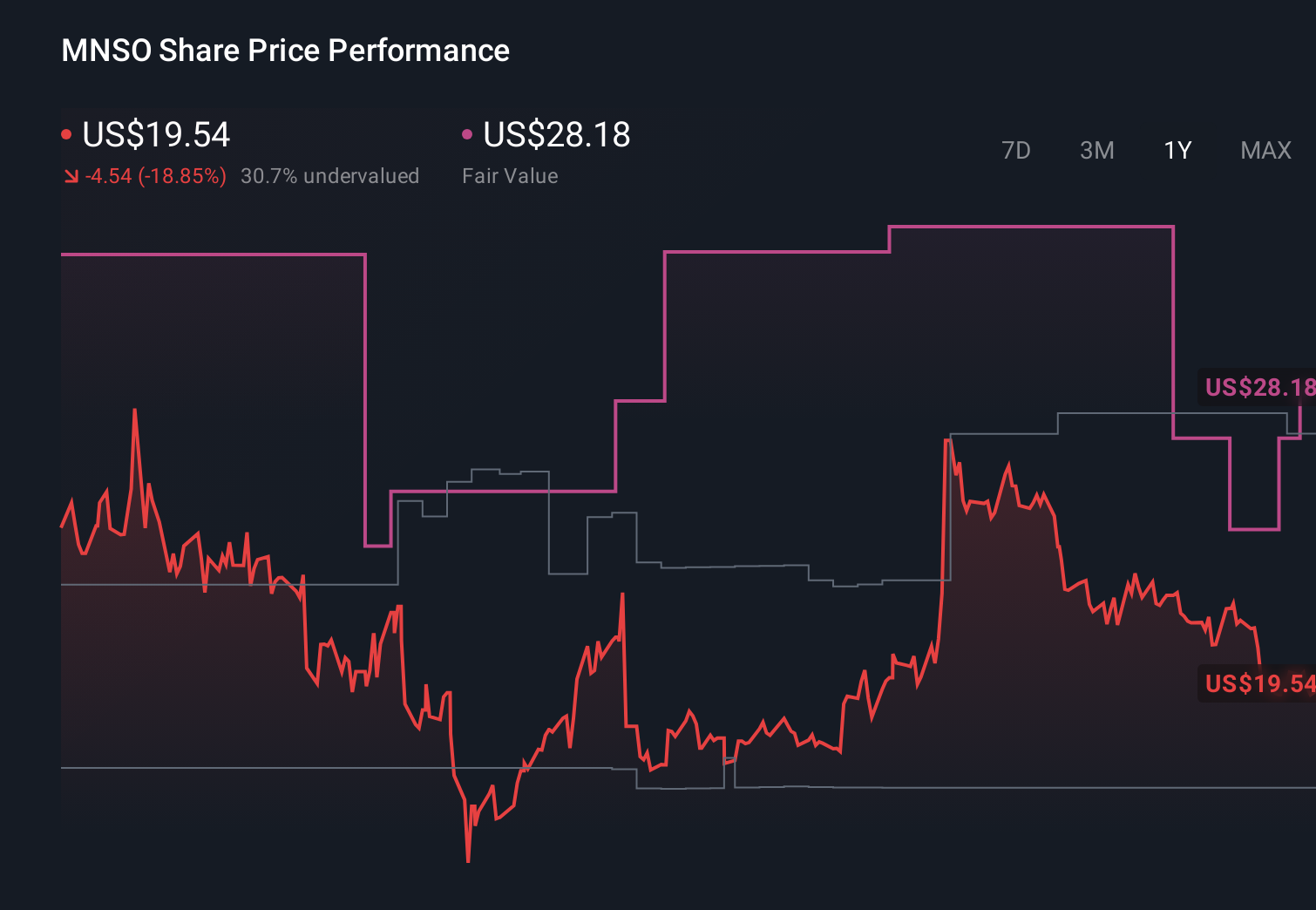

- In the past few days, MINISO Group Holding has drawn attention as valuation models suggest the stock trades well below estimated intrinsic value while analysts project double-digit year-over-year gains in earnings per share and revenue for the upcoming report.

- At the same time, the absence of recent insider transactions and the stock’s weaker recent performance versus both its sector and the broader market highlight a gap between analysts’ growth expectations and insider and market behavior that investors may want to scrutinize.

- We’ll now examine how analysts’ expectations for strong upcoming earnings and revenue growth may influence MINISO’s existing investment narrative.

Uncover the next big thing with 27 elite penny stocks that balance risk and reward.

MINISO Group Holding Investment Narrative Recap

To own MINISO today, you need to believe its IP-driven, value retail model can convert store expansion and overseas growth into durable earnings and cash flow, despite recent share price weakness. The latest news of the stock trading well below several intrinsic value estimates and consensus calls for double digit near term earnings and revenue growth do not materially change the core near term catalyst, which is delivery against upcoming earnings expectations, or the key risk of margin pressure from expansion and rising costs.

Against this backdrop, MINISO’s ongoing share buyback program, which has retired about 6.2% of shares for roughly HK$632.51 million since late 2024, stands out. While the stock has recently lagged both its sector and the broader market, this capital return, together with higher recent dividends, sits in tension with the lack of fresh insider buying and puts more focus on whether future earnings reports justify continued buybacks at current valuations.

Yet beneath the apparent discount, the risk that rising costs and store expansion could squeeze profits is something investors should be aware of...

Read the full narrative on MINISO Group Holding (it's free!)

MINISO Group Holding's narrative projects CN¥33.1 billion revenue and CN¥3.9 billion earnings by 2029. This requires 15.6% yearly revenue growth and about CN¥2.7 billion earnings increase from CN¥1.2 billion today.

Uncover how MINISO Group Holding's forecasts yield a $23.25 fair value, a 64% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts painted a far tougher picture, assuming revenue around CN¥32.3 billion and earnings near CN¥3.6 billion by 2029, so you should recognize that views on MINISO’s risks and upside can differ sharply and consider how this new earnings and valuation news might shift those expectations.

Explore 7 other fair value estimates on MINISO Group Holding - why the stock might be worth over 2x more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your MINISO Group Holding research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free MINISO Group Holding research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate MINISO Group Holding's overall financial health at a glance.

Curious About Other Options?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Outshine the giants: these 16 early-stage AI stocks could fund your retirement.

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 30 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com