- In early May 2026, Avista Corporation reported first-quarter 2026 earnings with net income of US$92 million on revenue of US$570 million, affirmed a quarterly dividend of US$0.4925 per share payable June 12, 2026, and outlined a US$3.40 billions 2026–2030 capital plan alongside updated utility earnings guidance.

- These updates, combined with clean energy and wildfire mitigation investments, regulatory progress, and insider share purchases, underline how Avista is tying long-term infrastructure spending to reliability, decarbonization, and a continued focus on dividends.

- Now we will explore how Avista’s US$3.40 billions capital expenditure and clean energy plan could influence its existing investment narrative.

The future of work is here. Discover the 34 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Avista Investment Narrative Recap

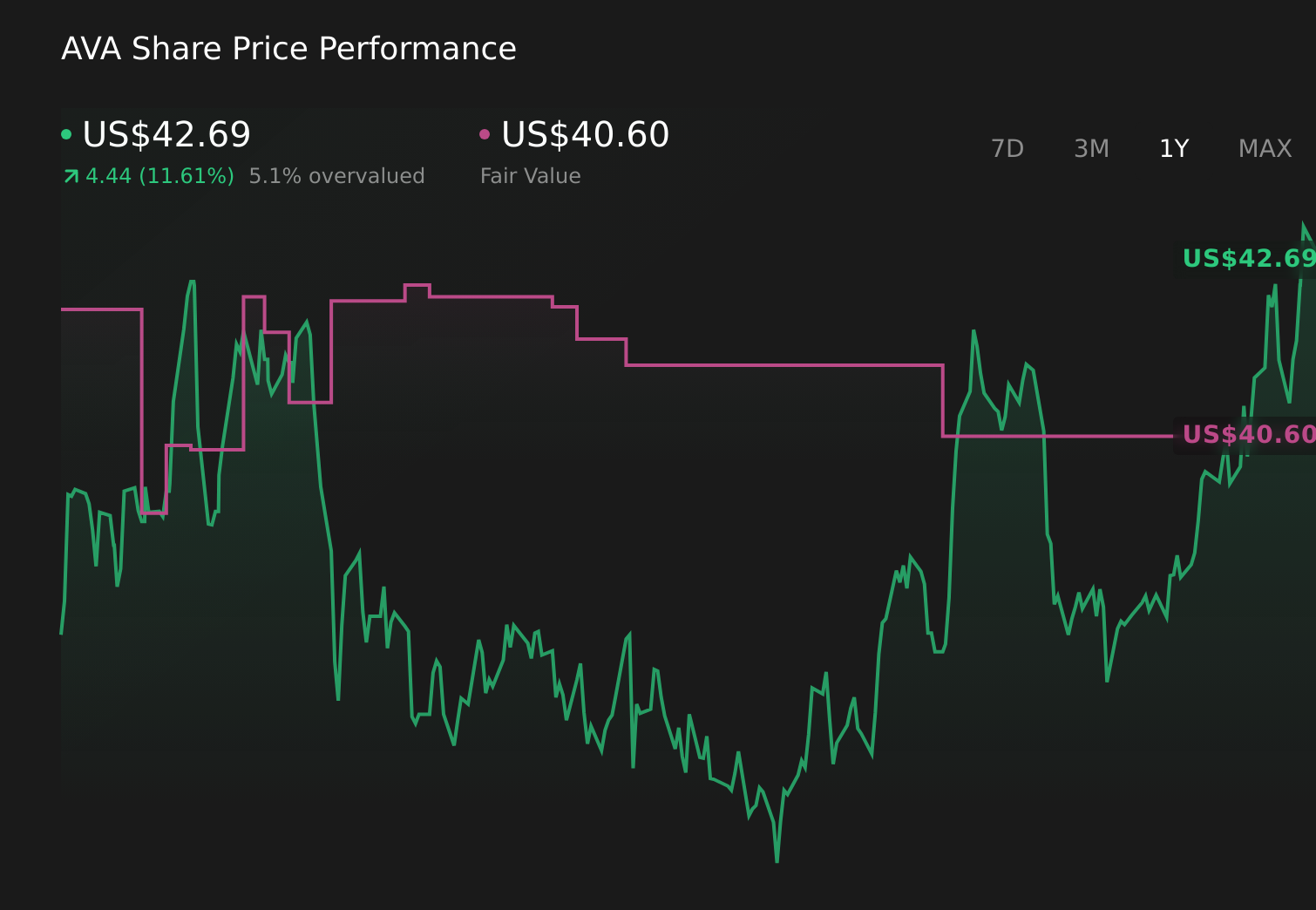

To own Avista, you need to believe that a regulated utility focused on the Pacific Northwest can steadily earn its allowed returns while managing wildfire, regulatory, and capital-intensity risks. The Q1 2026 earnings beat on net income, reaffirmed dividend, and US$3.40 billion capital plan reinforce the near term catalyst of constructive rate recovery, but they do not fundamentally change the key risk that rising grid and wildfire spending may outpace what regulators will allow into rates.

The updated 2026 non GAAP utility earnings guidance of US$2.52 to US$2.72 per diluted share is especially relevant here, because it connects Avista’s capital and clean energy spending to near term earnings expectations and dividend support. For investors tracking catalysts, this guidance bracket helps frame how much of the planned wildfire mitigation, microgrid projects, and broader 2026–2030 capex might realistically be recovered through existing and upcoming rate cases.

Yet investors should be aware that if rising grid and wildfire costs are not fully recovered through rates...

Read the full narrative on Avista (it's free!)

Avista's narrative projects $2.2 billion revenue and $253.4 million earnings by 2029. This requires 3.3% yearly revenue growth and about a $60 million earnings increase from $193.0 million today.

Uncover how Avista's forecasts yield a $42.80 fair value, a 6% upside to its current price.

Exploring Other Perspectives

Members of the Simply Wall St Community currently see Avista’s fair value between US$35.94 and US$42.80 across 2 independent views, underscoring how far opinions can spread. Set against this, Avista’s sizeable US$3.40 billion 2026 to 2030 capital plan highlights how much its longer term performance hinges on constructive regulatory outcomes and cost recovery, so it is worth exploring several of these perspectives side by side.

Explore 2 other fair value estimates on Avista - why the stock might be worth 11% less than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Avista research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Avista research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Avista's overall financial health at a glance.

Contemplating Other Strategies?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- AI is about to change healthcare. These 32 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com