First quarter earnings spark fresh attention on NCR Atleos

NCR Atleos (NATL) has drawn fresh attention after reporting first quarter 2026 results, with revenue of US$1,043 million and net income of US$22 million, compared with US$979 million and US$14 million a year earlier.

See our latest analysis for NCR Atleos.

The earnings update appears to have supported sentiment, with a 7 day share price return of 2.24% and a year to date share price return of 20.31%. The 1 year total shareholder return of 63.53% points to strong momentum over a longer horizon.

If strong recent results have you rethinking your watchlist, this could be a useful moment to see how other payment and fintech related plays stack up using 21 cryptocurrency and blockchain stocks.

With NCR Atleos trading at US$44.79 alongside a 63.53% 1 year total return and sitting below the US$50.27 analyst price target, readers may wonder whether there is still a buying opportunity or whether markets are already pricing in future growth.

Most Popular Narrative: 10.9% Undervalued

With the shares last closing at $44.79 against a narrative fair value of $50.27, the widely followed view points to modest upside still on the table.

High recurring revenue mix (over 70% in Q2), significant productivity gains through AI-driven service optimization, and a rapidly scaling backlog are driving strong margin expansion and robust free cash flow, underpinning announced share buybacks and sustained EPS growth, suggesting current valuation does not reflect enhanced long-term earnings power.

Curious how recurring revenue, margin expansion and future earnings are stitched together into one price tag for NCR Atleos? The key assumptions sit in a tight balance between steady top line expectations, rising profitability and a lower future earnings multiple than many peers.

Result: Fair Value of $50.27 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the story can change if cash usage falls faster than expected, or if fintech and large tech competition starts to squeeze margins in ATM and payment services.

Find out about the key risks to this NCR Atleos narrative.

Another way to look at the valuation

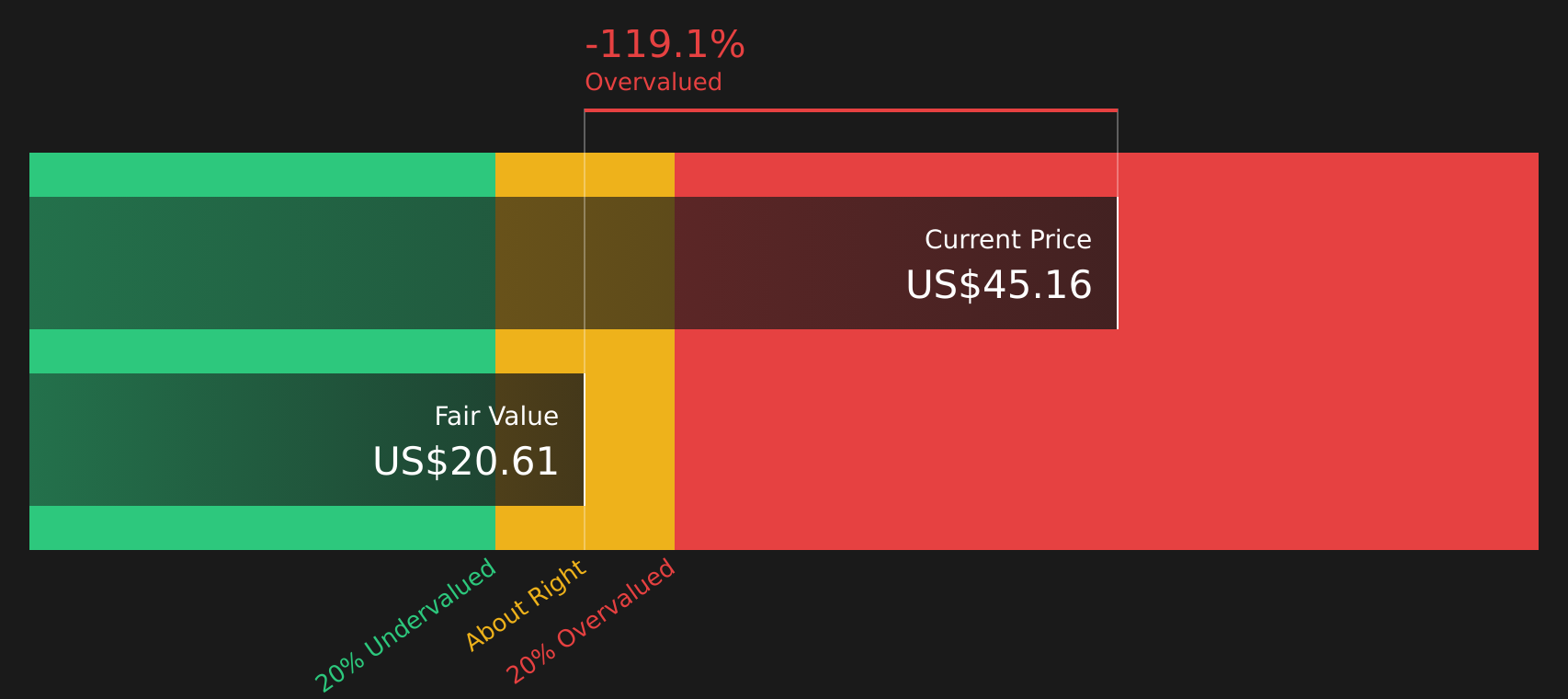

Analysts see NCR Atleos as 10.9% undervalued using their earnings based fair value of $50.27. However, the SWS DCF model paints a different picture, with a future cash flow value of $20.56 and the stock trading at $44.79. This raises the question of which set of assumptions you trust more.

Look into how the SWS DCF model arrives at its fair value.

Next Steps

Feeling mixed after weighing both the upside and the concerns around NCR Atleos? Act while the details are fresh and stress test the thesis against 2 key rewards and 2 important warning signs.

Looking for more investment ideas?

Do not stop your research with a single stock. Broaden your watchlist now so you are not scrambling for ideas when markets move fast.

- Target potential bargains with quality metrics on your side by scanning 51 high quality undervalued stocks that pair solid fundamentals with attractive pricing.

- Strengthen your income stream by reviewing 12 dividend fortresses focused on higher yielding companies that still aim to keep payouts supported.

- Lower portfolio stress by checking 65 resilient stocks with low risk scores featuring companies assessed for more resilient balance sheets and milder risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com