- Warrior Met Coal recently reported past first-quarter results showing much higher revenue and adjusted EBITDA, as the Blue Creek mine completed major construction ahead of schedule and began meaningfully contributing to operations.

- At the same time, institutional investors reshuffled their positions while management reaffirmed full-year guidance, suggesting that the shift from heavy project spending to production at Blue Creek is materially changing the company’s risk and cash flow profile.

- Now we’ll examine how Blue Creek’s ahead-of-schedule ramp-up and growing contribution could reshape Warrior Met Coal’s investment narrative.

This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

Warrior Met Coal Investment Narrative Recap

To own Warrior Met Coal, you need to believe that the heavy lifting at Blue Creek is largely behind the company and that the mine’s higher quality, lower cost tons can offset pricing pressure in steelmaking coal. The latest results, with strong year over year revenue and adjusted EBITDA and Blue Creek already contributing, support that view and reduce near term project execution risk, though exposure to softer coal prices remains a key swing factor.

The most relevant recent development is management’s decision to reaffirm full year 2026 guidance for coal sales and production despite weaker volumes and pricing in Q1. That stance, alongside the completion of major Blue Creek construction ahead of schedule, ties directly into the core catalyst of shifting from capital spending to production-driven cash generation, while leaving investors to weigh how resilient those targets are if steel demand or met coal prices soften further.

Yet even with Blue Creek ramping, investors should be aware that concentrated exposure to Asian steel markets could quickly become a problem if...

Read the full narrative on Warrior Met Coal (it's free!)

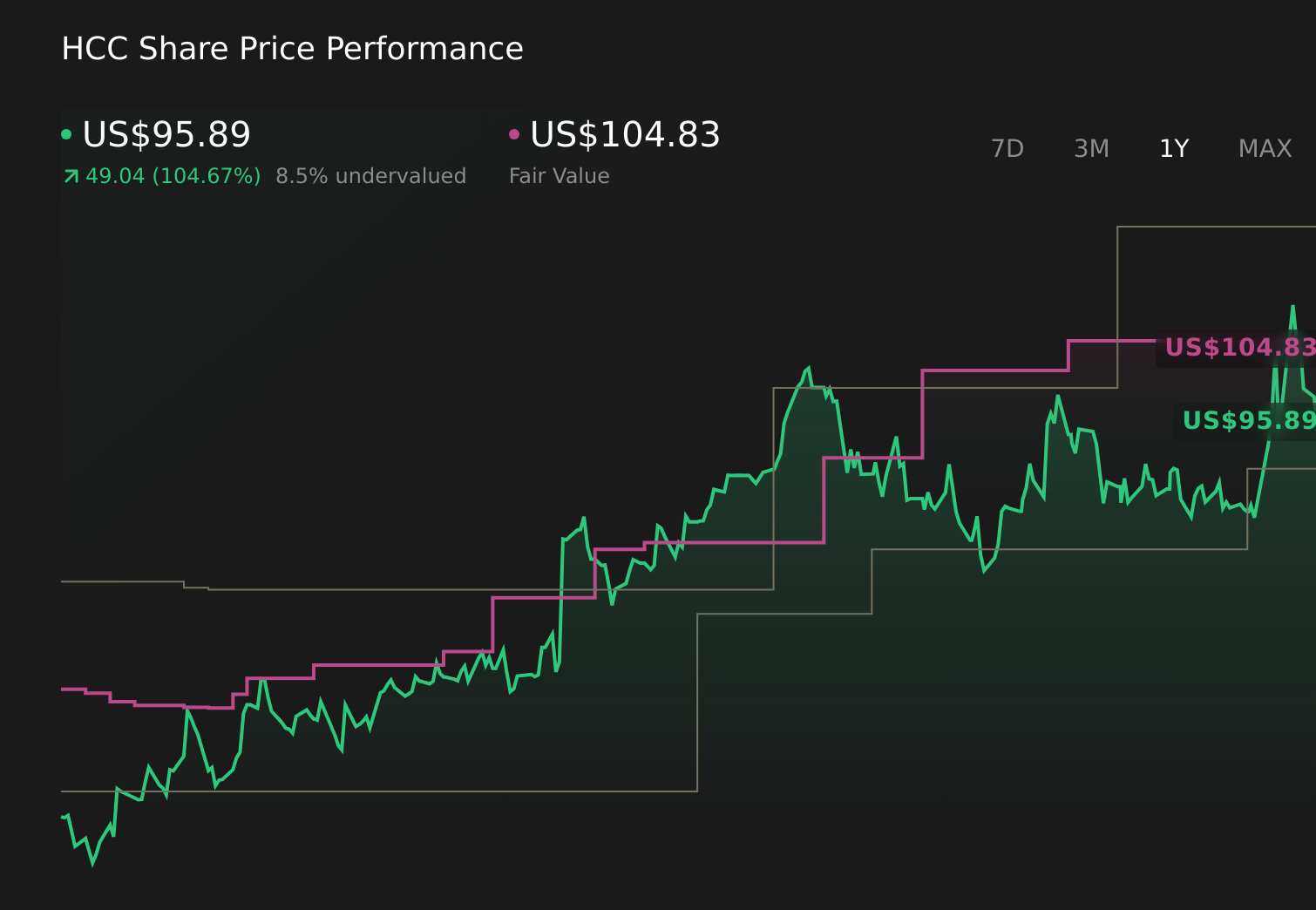

Warrior Met Coal's narrative projects $2.3 billion revenue and $472.1 million earnings by 2029.

Uncover how Warrior Met Coal's forecasts yield a $105.67 fair value, a 23% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already building in a harsher future, assuming revenue of about US$1.9 billion and earnings of roughly US$264.0 million by 2028, and they viewed Blue Creek’s ramp up as a double edged sword that might cap share upside if demand disappoints, which shows how differently you and other investors might interpret this latest news.

Explore 4 other fair value estimates on Warrior Met Coal - why the stock might be worth just $104.83!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Warrior Met Coal research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Warrior Met Coal research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Warrior Met Coal's overall financial health at a glance.

Interested In Other Possibilities?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- AI is about to change healthcare. These 31 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Outshine the giants: these 15 early-stage AI stocks could fund your retirement.

- The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com