Over the last 7 days, the United States market has experienced a slight decline of 1.0%, yet it remains robust with a 23% increase over the past year and an anticipated annual earnings growth of 17%. In this dynamic environment, identifying stocks that are not only resilient but also poised for growth can be key to uncovering hidden opportunities in the market.

Top 10 Undiscovered Gems With Strong Fundamentals In The United States

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| First Bancorp | 69.86% | 1.25% | -3.09% | ★★★★★★ |

| Bank of the James Financial Group | 10.74% | 5.28% | 3.68% | ★★★★★★ |

| New Peoples Bankshares | 22.84% | 4.06% | 9.72% | ★★★★★★ |

| Tri-County Financial Group | 54.21% | -0.70% | -10.52% | ★★★★★★ |

| ASA Gold and Precious Metals | NA | 12.65% | 41.20% | ★★★★★★ |

| SIFCO Industries | 12.27% | -4.21% | -2.87% | ★★★★★★ |

| Affinity Bancshares | 41.71% | 1.36% | -0.22% | ★★★★★★ |

| Winchester Bancorp | 123.28% | 9.14% | -54.82% | ★★★★★★ |

| Union Bankshares | 406.25% | 1.42% | -7.24% | ★★★★☆☆ |

| High Templar Tech | 13.55% | -66.76% | -26.62% | ★★★★☆☆ |

We'll examine a selection from our screener results.

Greenlight Capital Re (GLRE)

Simply Wall St Value Rating: ★★★★★★

Overview: Greenlight Capital Re, Ltd. operates as a property and casualty reinsurance company globally, with a market cap of $594.67 million.

Operations: The company's revenue streams include Corporate ($37.79 million), Innovations ($82.37 million), and Open Market ($586.77 million).

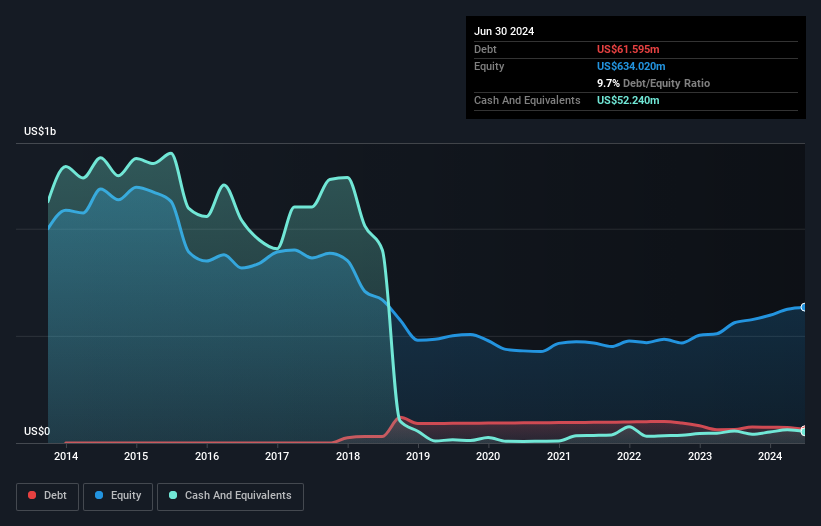

Greenlight Capital Re, a nimble player in the insurance industry, has shown robust financial health with earnings growth of 78.2% over the past year, outpacing the industry's 36.2%. The company is trading at a significant discount of 54.9% below its estimated fair value and has reduced its debt to equity ratio from 20.2% to just 0.6% over five years, indicating strong financial management. Recent buyback activities saw $14.49 million spent on repurchasing shares this year alone, reflecting confidence in its valuation and future prospects despite recent insider selling activity.

Rocky Brands (RCKY)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Rocky Brands, Inc. is a company that designs, manufactures, and markets footwear and apparel across multiple regions including the United States, Canada, and the United Kingdom with a market capitalization of $258.97 million.

Operations: Rocky Brands generates revenue primarily from wholesale ($320.17 million) and retail ($158.95 million) segments, with a smaller contribution from contract manufacturing ($13.19 million).

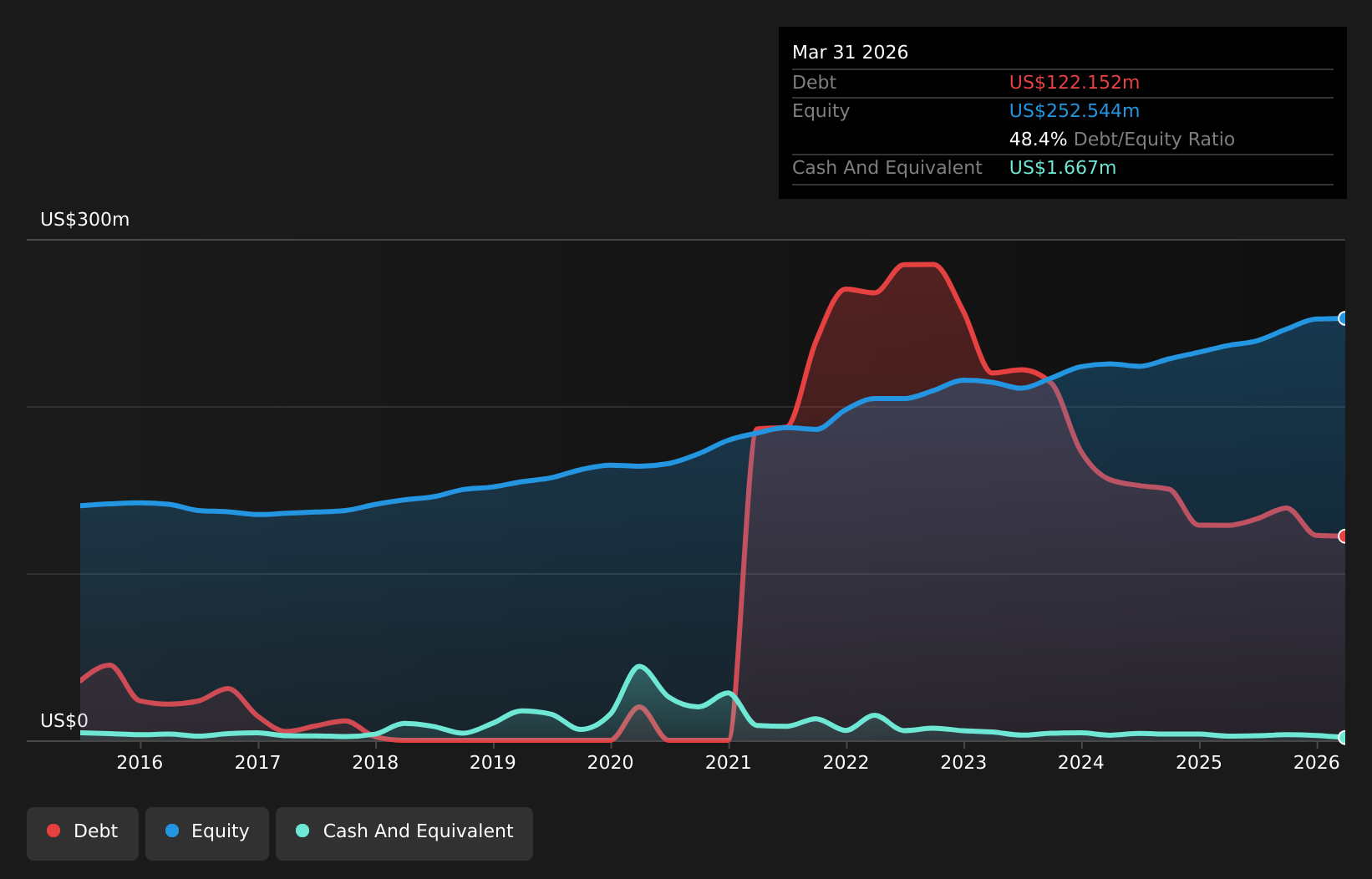

Rocky Brands, a notable player in the footwear industry, has shown resilience with its debt to equity ratio dropping from 101.3% to 48.4% over five years. Despite a high net debt to equity ratio of 47.7%, earnings surged by 34.9% last year, outpacing the luxury sector's growth of 17.2%. However, earnings have dipped by an average of 7.4% annually over five years, reflecting volatility in performance. The price-to-earnings ratio stands at a favorable 14x against the US market's average of 18x, hinting at potential value for investors seeking opportunities in this dynamic yet challenging landscape.

- Take a closer look at Rocky Brands' potential here in our health report.

Evaluate Rocky Brands' historical performance by accessing our past performance report.

South Plains Financial (SPFI)

Simply Wall St Value Rating: ★★★★★★

Overview: South Plains Financial, Inc. is a bank holding company for City Bank, offering commercial and consumer financial services to small and medium-sized businesses and individuals, with a market cap of $764.68 million.

Operations: South Plains Financial generates revenue primarily from its banking segment, totaling $211.85 million. The company's financial performance is influenced by its net profit margin, which has shown variability over recent periods.

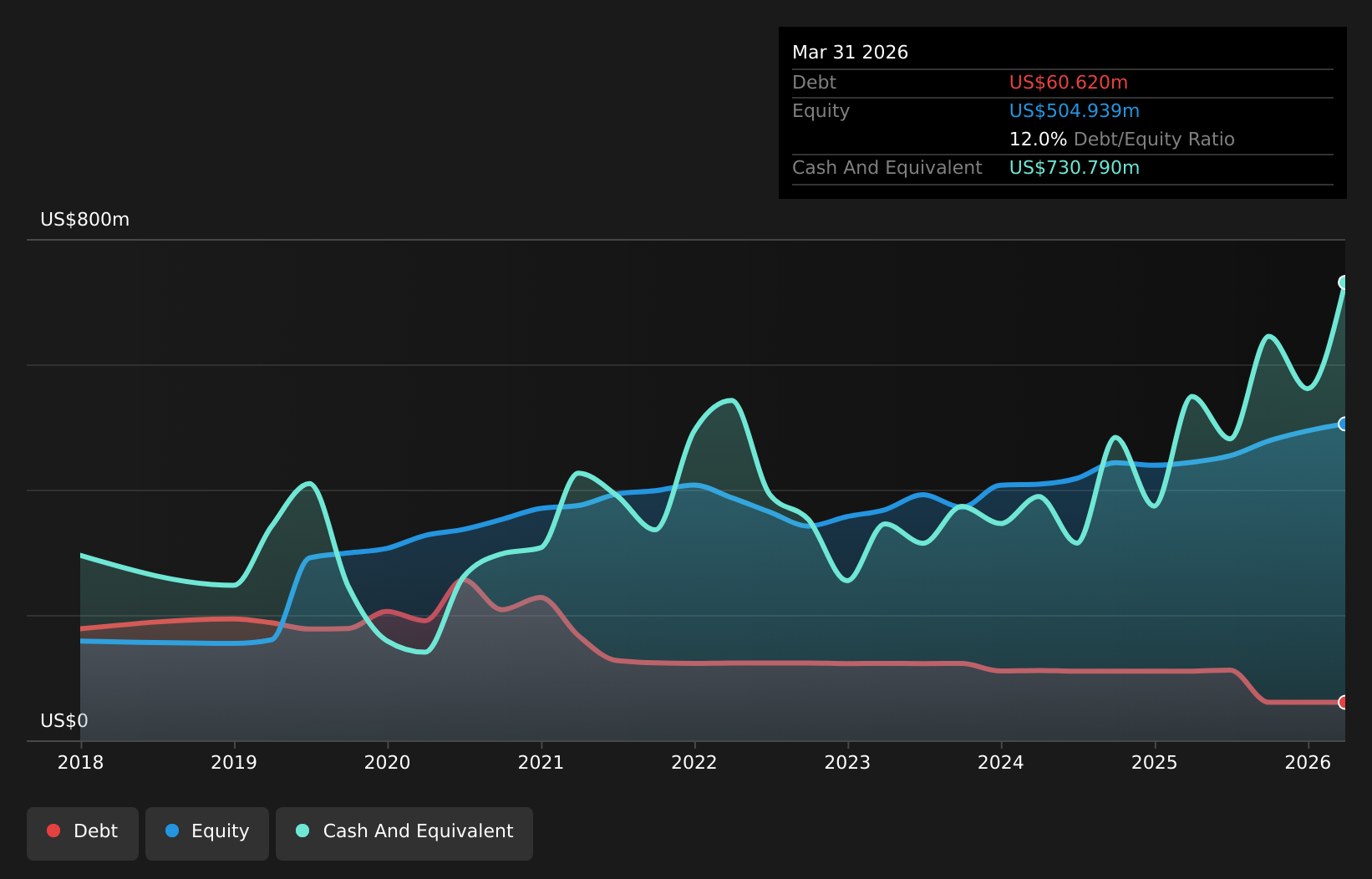

South Plains Financial, with assets totaling $4.6 billion and equity of $504.9 million, is making strides in the Texas market by expanding its lending team and pursuing strategic acquisitions. The company boasts a net interest margin of 4% and maintains a solid allowance for bad loans at 0.2% of total loans, indicating robust risk management practices. While trading at 59.5% below estimated fair value suggests potential upside, shareholders experienced dilution last year. Despite these challenges, South Plains remains focused on leveraging its primarily low-risk funding sources to drive sustainable growth in the competitive banking landscape.

Taking Advantage

- Delve into our full catalog of 337 US Undiscovered Gems With Strong Fundamentals here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com