Over the last 7 days, the United States market has experienced a slight dip of 1.0%, yet it has shown impressive growth of 23% over the past year, with earnings anticipated to increase by 17% annually in the coming years. In such dynamic conditions, identifying lesser-known stocks with strong fundamentals and growth potential can offer unique opportunities for investors seeking to diversify their portfolios.

Top 10 Undiscovered Gems With Strong Fundamentals In The United States

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| First Bancorp | 69.86% | 1.25% | -3.09% | ★★★★★★ |

| Bank of the James Financial Group | 10.74% | 5.28% | 3.68% | ★★★★★★ |

| New Peoples Bankshares | 22.84% | 4.06% | 9.72% | ★★★★★★ |

| Tri-County Financial Group | 54.21% | -0.70% | -10.52% | ★★★★★★ |

| ASA Gold and Precious Metals | NA | 12.65% | 41.20% | ★★★★★★ |

| Sound Financial Bancorp | 16.13% | 0.44% | -12.60% | ★★★★★★ |

| SIFCO Industries | 12.27% | -4.21% | -2.87% | ★★★★★★ |

| Anbio Biotechnology | NA | -30.09% | -3.45% | ★★★★★★ |

| Union Bankshares | 406.25% | 1.42% | -7.24% | ★★★★☆☆ |

| High Templar Tech | 13.55% | -66.76% | -26.62% | ★★★★☆☆ |

Below we spotlight a couple of our favorites from our exclusive screener.

First Bank (FRBA)

Simply Wall St Value Rating: ★★★★★★

Overview: First Bank offers a range of banking products and services tailored for small and mid-sized businesses as well as individuals, with a market cap of $381.19 million.

Operations: Revenue for FRBA primarily comes from its community banking segment, totaling $133.63 million.

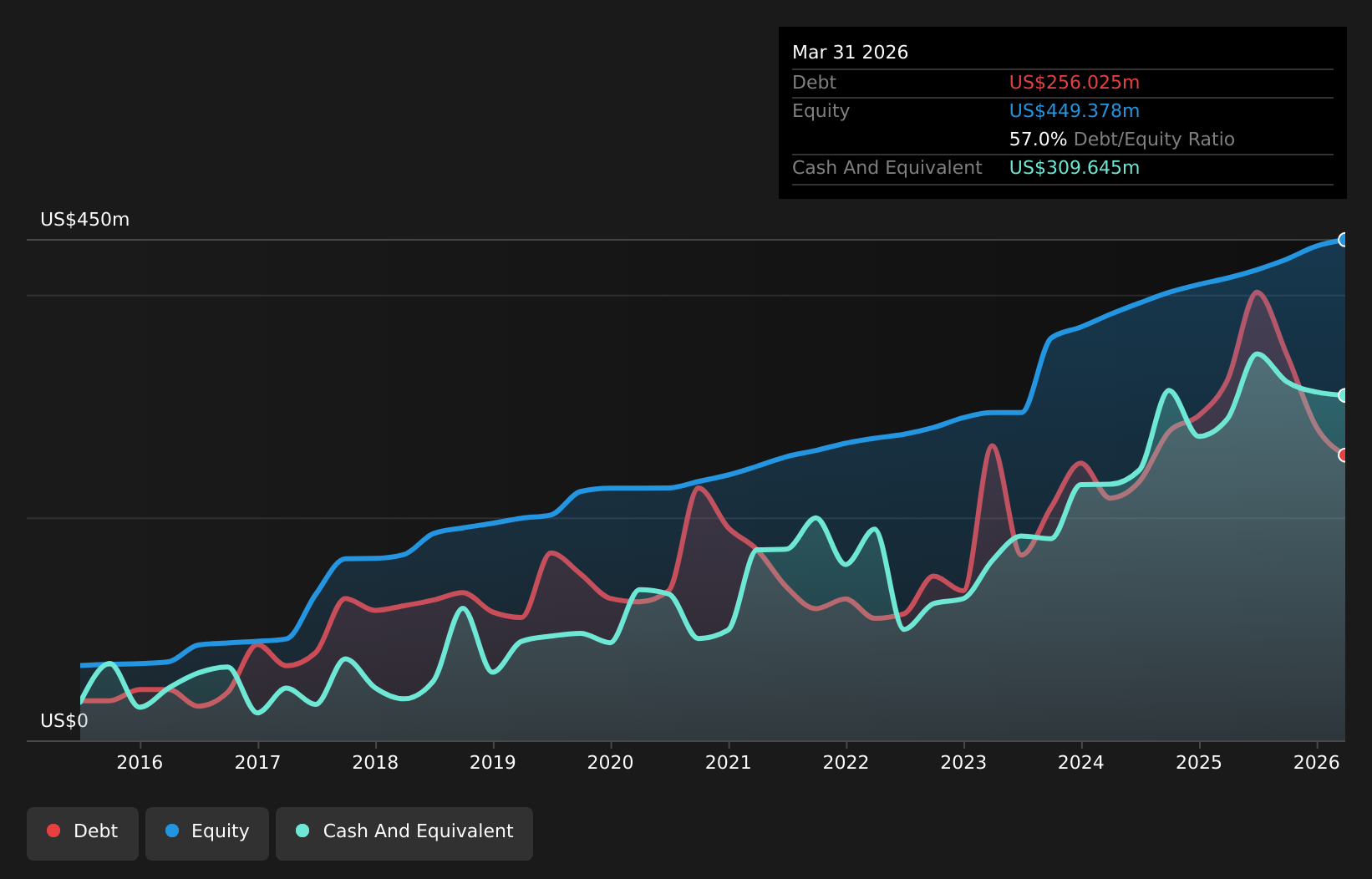

First Bank, with total assets of US$4.0 billion and equity of US$449.4 million, offers a compelling profile in the financial sector. It has total deposits of US$3.2 billion against loans totaling US$3.3 billion, demonstrating robust balance sheet management with a net interest margin standing at 3.7%. The bank's allowance for bad loans is sufficient at 175%, covering non-performing loans that are just 0.8% of its total loan portfolio, showcasing prudent risk management practices. Recently, the company repurchased 33,619 shares for about US$0.52 million and announced a quarterly dividend of US$0.09 per share payable on May 22, 2026.

- Delve into the full analysis health report here for a deeper understanding of First Bank.

Review our historical performance report to gain insights into First Bank's's past performance.

PCB Bancorp (PCB)

Simply Wall St Value Rating: ★★★★★★

Overview: PCB Bancorp is a bank holding company for PCB Bank, offering a range of banking products and services to small and middle-market businesses and individuals in the United States, with a market cap of $337.45 million.

Operations: PCB Bancorp generates revenue primarily from its banking industry operations, totaling $116.14 million.

PCB Bancorp, with assets totaling $3.4 billion and equity of $396.7 million, seems to be an intriguing player in the financial landscape. Its earnings growth of 42.5% last year outpaced the industry average of 22.8%, showcasing robust performance. The company's allowance for bad loans stands at a healthy 366%, while non-performing loans are just 0.3% of total loans, indicating strong risk management practices. Trading nearly 20% below its estimated fair value, PCB offers a compelling valuation compared to peers and the broader industry context, suggesting potential upside for those keeping an eye on smaller financial entities like this one.

- Click here and access our complete health analysis report to understand the dynamics of PCB Bancorp.

Gain insights into PCB Bancorp's past trends and performance with our Past report.

High Templar Tech (HTT)

Simply Wall St Value Rating: ★★★★☆☆

Overview: High Templar Tech Limited is a consumer-oriented financial technology service company based in the People’s Republic of China, with a market cap of approximately CN¥338.52 million.

Operations: HTT generates revenue primarily from installment credit services, totaling CN¥40.96 million. The company's net profit margin is 12.5%.

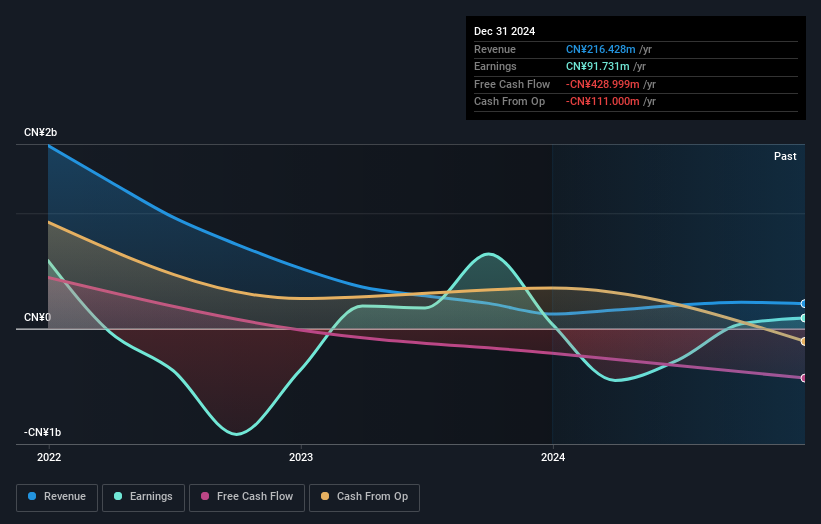

High Templar Tech, a small cap entity, has demonstrated remarkable earnings growth of 672.5% over the past year, outpacing the Consumer Finance industry at 28.9%. Despite this surge, its debt to equity ratio increased from 7.8% to 13.5% over five years, indicating rising leverage concerns. The company repurchased nearly 16% of its shares for US$77.7 million by March 2026, suggesting confidence in future prospects despite recent challenges like a net loss of CNY163 million in Q4 and declining sales from CNY216 million to CNY41 million annually. Its price-to-earnings ratio stands attractively low at 3.3x against the broader market's average of 18.5x.

- Navigate through the intricacies of High Templar Tech with our comprehensive health report here.

Assess High Templar Tech's past performance with our detailed historical performance reports.

Key Takeaways

- Get an in-depth perspective on all 337 US Undiscovered Gems With Strong Fundamentals by using our screener here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com