- At its Annual Meeting held on May 12, 2026, Centene appointed Daniel Finke as Group President of Medicaid and Marketplace and Michael Carson as Group President of Medicare and Specialty to oversee its core government and specialty businesses.

- These leadership appointments underline Centene’s effort to sharpen operational efficiency across Medicaid, Marketplace, Medicare and specialty lines, potentially influencing how it executes on its existing growth and margin recovery plans.

- We’ll now examine how placing Daniel Finke over Medicaid and Marketplace could influence Centene’s existing investment narrative and future execution.

Outshine the giants: these 14 early-stage AI stocks could fund your retirement.

Centene Investment Narrative Recap

To own Centene, you have to believe its scale in Medicaid, Marketplace and Medicare can translate into steadier margins despite policy and cost pressures. The new appointments of Daniel Finke and Michael Carson look incremental rather than transformative for the near term, so the key catalyst remains how quickly Medicaid and Marketplace margins stabilize, while the biggest risk is still policy or rate decisions that fail to fully reflect rising medical and drug costs.

The most relevant recent announcement alongside these leadership changes is Centene’s April 2026 guidance update, which reiterated 2026 revenue expectations of US$187.5 billion to US$191.5 billion and GAAP diluted EPS above US$2.37. How effectively Finke and Carson execute across Medicaid, Marketplace, Medicare and specialty will influence whether Centene can move from simply meeting this guidance to improving its margin profile in the face of inflation in care delivery and specialty drugs.

But against this improving operational story, investors should be aware of the persistent risk that government reimbursement and medical cost trends...

Read the full narrative on Centene (it's free!)

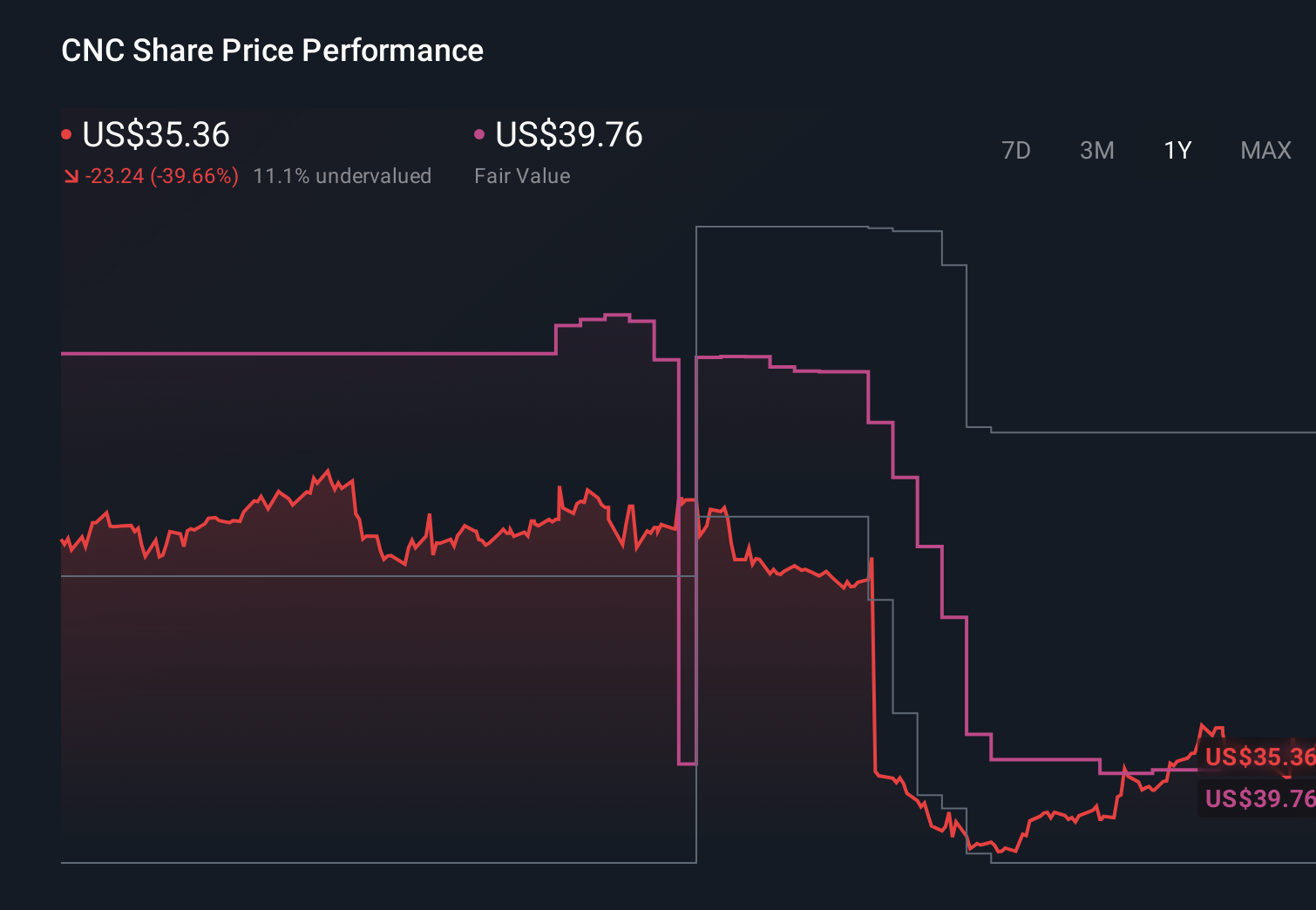

Centene's narrative projects $199.9 billion revenue and $2.7 billion earnings by 2029.

Uncover how Centene's forecasts yield a $54.94 fair value, a 6% downside to its current price.

Exploring Other Perspectives

Compared with the baseline, the most optimistic analysts were already assuming revenues of about US$205.6 billion and earnings of roughly US$3.0 billion by 2029, so these leadership changes could either reinforce or challenge that faster Medicaid margin rebound story, which is why it helps to compare several viewpoints before deciding what you believe.

Explore 16 other fair value estimates on Centene - why the stock might be worth over 3x more than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Centene research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Centene research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Centene's overall financial health at a glance.

Contemplating Other Strategies?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- AI is about to change healthcare. These 29 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com