- Earlier this week, The Williams Companies, Inc. filed a shelf registration to offer up to US$4.22 billion in common stock, including 53,100,000 shares tied to an ESOP-related program.

- This potential capital-raising move comes as Williams is highlighted for its role in transporting a large portion of U.S. natural gas and its positioning to benefit from rising clean energy demand.

- We’ll now examine how this large shelf registration, aimed at potential future common stock issuance, may influence Williams’ investment narrative.

Uncover the next big thing with 27 elite penny stocks that balance risk and reward.

Williams Companies Investment Narrative Recap

To own Williams, you have to believe in the long-term relevance of U.S. natural gas infrastructure and its contracted cash flows. The new US$4.22 billion shelf registration, largely tied to ESOP-related shares, primarily affects how Williams might finance future needs rather than its core pipeline thesis. In the near term, the most important catalyst remains execution on its expansion projects, while elevated leverage and future capital needs continue to be a key risk.

The recent shelf filing sits alongside Williams’ continued capital and shareholder return activity, including its April decision to maintain a quarterly dividend of US$0.525 per share after a 5% increase earlier in 2026. That combination of potential equity issuance and ongoing dividends highlights the balance the company is trying to strike between funding large growth projects and managing financial risk. How well Williams maintains that balance will matter for how investors view this news.

Yet behind Williams’ growth story, investors should also be aware that accelerating decarbonization and policy shifts could eventually reduce natural gas volumes and leave some assets at risk of becoming...

Read the full narrative on Williams Companies (it's free!)

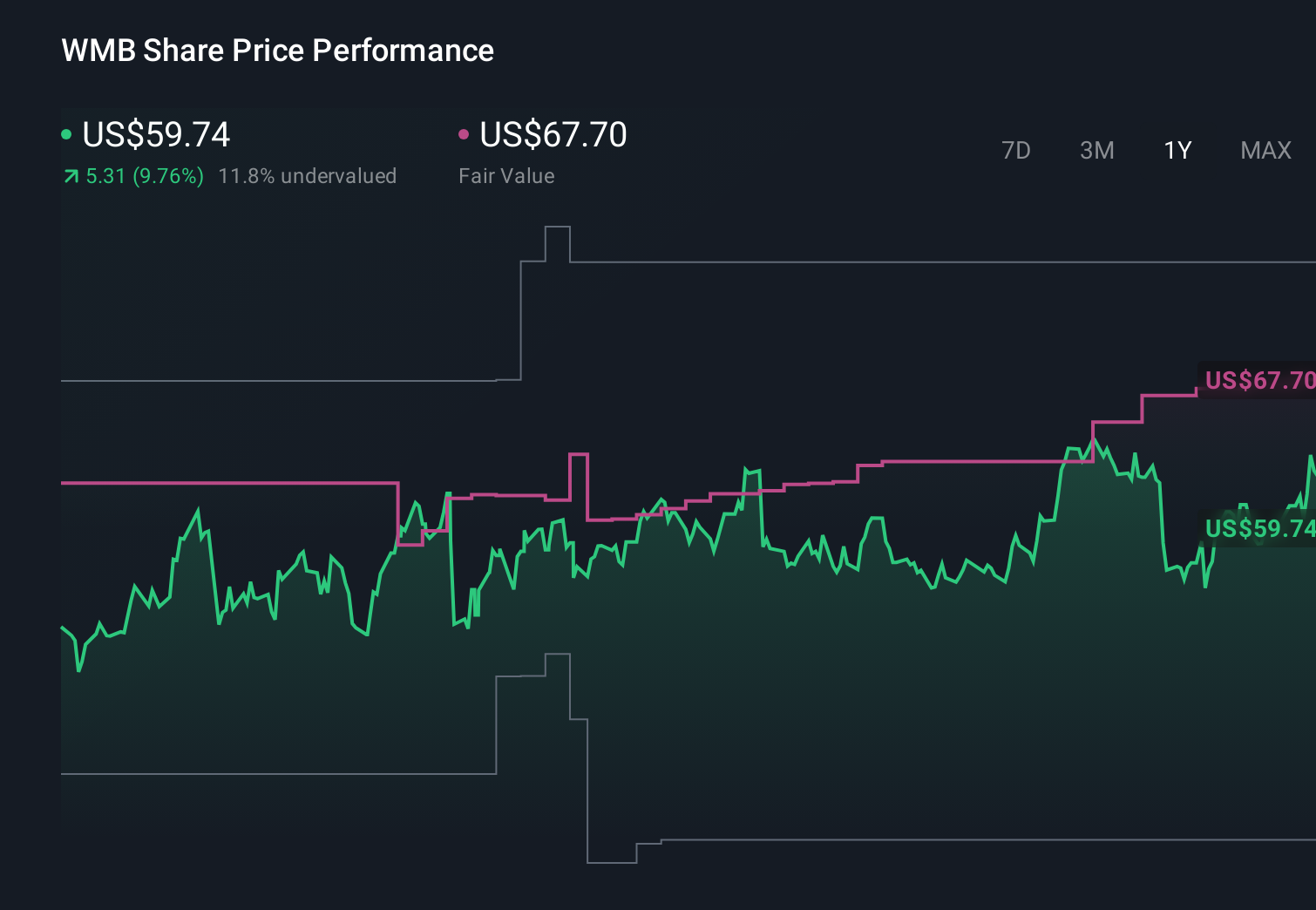

Williams Companies' narrative projects $16.3 billion revenue and $3.9 billion earnings by 2029. This requires 11.3% yearly revenue growth and a $1.3 billion earnings increase from $2.6 billion today.

Uncover how Williams Companies' forecasts yield a $80.07 fair value, a 3% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts expected Williams’ revenue to reach about US$18.1 billion and earnings US$4.4 billion, which is far more bullish on growth than the more cautious views tied to energy transition and ESG risks, and the new shelf registration could ultimately push either story closer to reality.

Explore 4 other fair value estimates on Williams Companies - why the stock might be worth as much as 98% more than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Williams Companies research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Williams Companies research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Williams Companies' overall financial health at a glance.

Curious About Other Options?

Our top stock finds are flying under the radar-for now. Get in early:

- We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Outshine the giants: these 14 early-stage AI stocks could fund your retirement.

- The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com