- Ternium S.A. previously approved at its May 12, 2026 AGM an annual dividend of US$2.20 per ADS (US$0.22 per share), including a US$0.90 per ADS interim payment, with a remaining net dividend of US$1.30 per ADS payable on May 15, 2026 to shareholders of record on May 14, 2026.

- This dividend decision, including the balance between interim and final payouts, offers investors a window into how management is currently prioritizing cash returns versus reinvestment.

- We will now examine how this latest dividend approval, and the cash it returns to shareholders, could reshape Ternium’s broader investment narrative.

Uncover the next big thing with 27 elite penny stocks that balance risk and reward.

Ternium Investment Narrative Recap

To own Ternium, you need to believe in its ability to turn Latin American steel exposure and heavy capex into durable, cash-generating capacity. The AGM-approved annual dividend of US$2.20 per ADS, and the reduced final payout versus prior years, does not materially change the short term earnings catalyst, but it does slightly sharpen the focus on free cash flow strain from large projects as the key risk right now.

The most relevant recent announcement here is the April 15, 2026 board decision to cut the proposed 2025 dividend to US$2.20 per ADS, down from US$2.70. Together with the May 12 AGM approval, it underlines that supporting the balance sheet during a heavy US$4 billion investment cycle is taking precedence, which interacts directly with Ternium’s near term earnings trajectory and its exposure to global overcapacity.

Yet beneath the dividend cut, investors should be aware of how ongoing high capex and potential project delays could...

Read the full narrative on Ternium (it's free!)

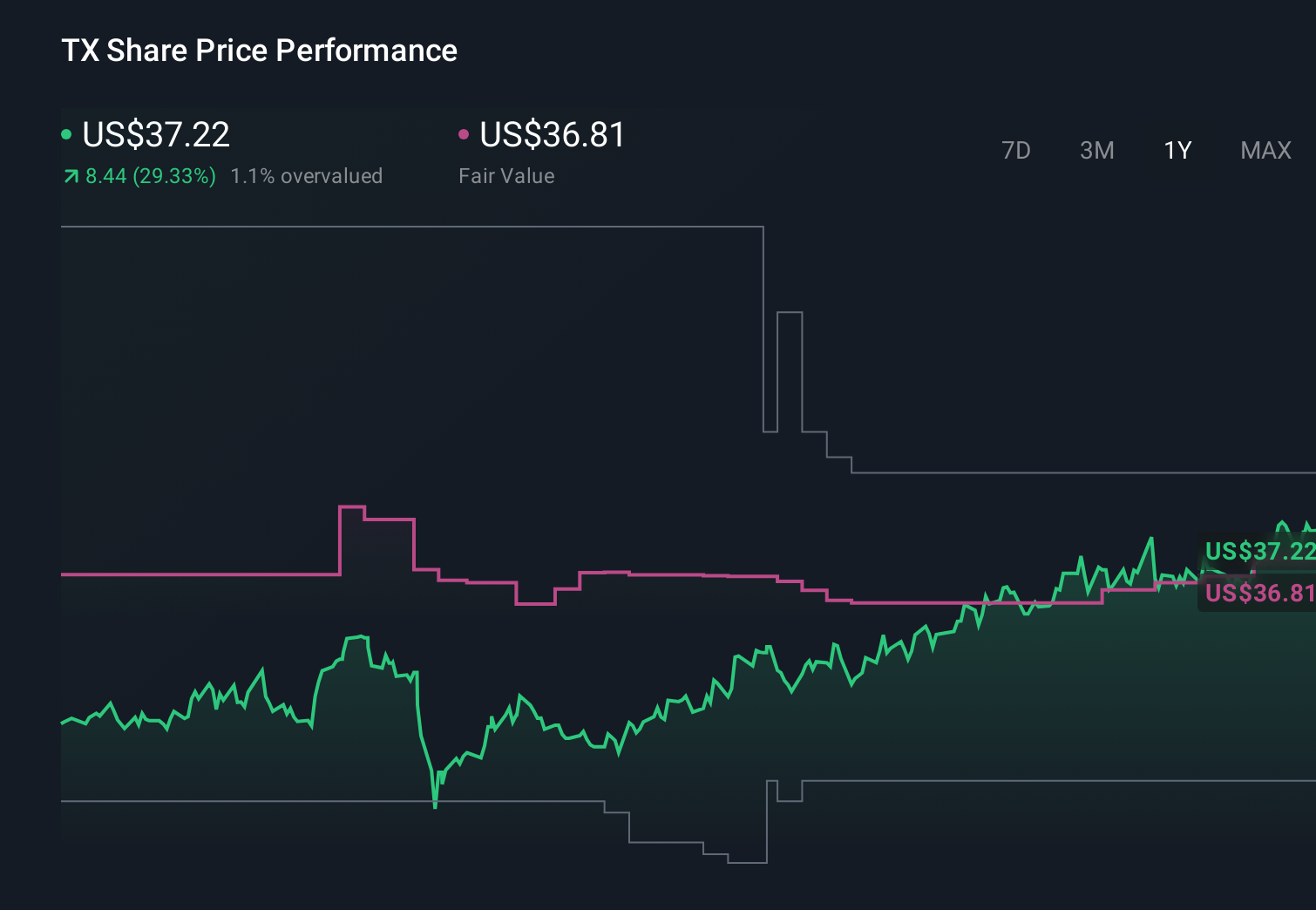

Ternium's narrative projects $18.1 billion revenue and $1.0 billion earnings by 2029. This requires 5.0% yearly revenue growth and a $574.8 million earnings increase from $425.2 million today.

Uncover how Ternium's forecasts yield a $43.46 fair value, in line with its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were previously assuming Ternium could lift earnings toward about US$1.1 billion over time, which is far above consensus, so if you see dividends tightening just as others expect green steel and regionalization to transform margins, it is a reminder that credible opinions on Ternium’s risks and upside can differ sharply and the latest payout decision may eventually shift how those stories evolve.

Explore 3 other fair value estimates on Ternium - why the stock might be worth as much as 76% more than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Ternium research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Ternium research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Ternium's overall financial health at a glance.

Interested In Other Possibilities?

Our top stock finds are flying under the radar-for now. Get in early:

- Outshine the giants: these 14 early-stage AI stocks could fund your retirement.

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com