- Clearway Energy, Inc. recently reported mixed first-quarter 2026 results, with sales rising to US$354 million but a net loss of US$163 million, reaffirmed its full-year cash available for distribution guidance and long-term targets, and outlined multi-year investment plans in wind repowering, storage and acquisitions.

- Ahead of a June 2026 leadership change in the General Counsel role, the company is emphasizing continuity in governance as it pursues growth tied to rising power demand, including data center-related opportunities.

- We’ll now examine how reaffirmed CAFD guidance amid plans for over US$3 billion of energy investments could influence Clearway Energy’s investment narrative.

The future of work is here. Discover the 34 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Clearway Energy Investment Narrative Recap

To own Clearway Energy, you need to be comfortable with a capital intensive plan built around long term, contracted renewables and storage that targets growing cash available for distribution. The latest mixed quarter and reaffirmed CAFD guidance keep that cash flow story intact, while the biggest near term swing factor remains execution on the multi year US$3 billion investment pipeline. The recent General Counsel transition looks structured for continuity and does not materially change that near term catalyst or the key risks.

The most relevant recent update is management’s plan to invest over US$3 billion between 2026 and 2029 in wind repowering, storage and acquisitions, on top of fully commercialized 2026 and 2027 project vintages. For investors tracking catalysts, that spending program is central to whether Clearway can translate its late stage pipeline and data center linked demand into the CAFD growth needed to support its dividend ambitions and long term targets.

Yet investors should also be aware that if capital markets become less receptive or the cost of debt and equity rises, then...

Read the full narrative on Clearway Energy (it's free!)

Clearway Energy's narrative projects $2.0 billion revenue and $165.3 million earnings by 2029. This requires 12.4% yearly revenue growth and a $3.7 million earnings decrease from $169.0 million today.

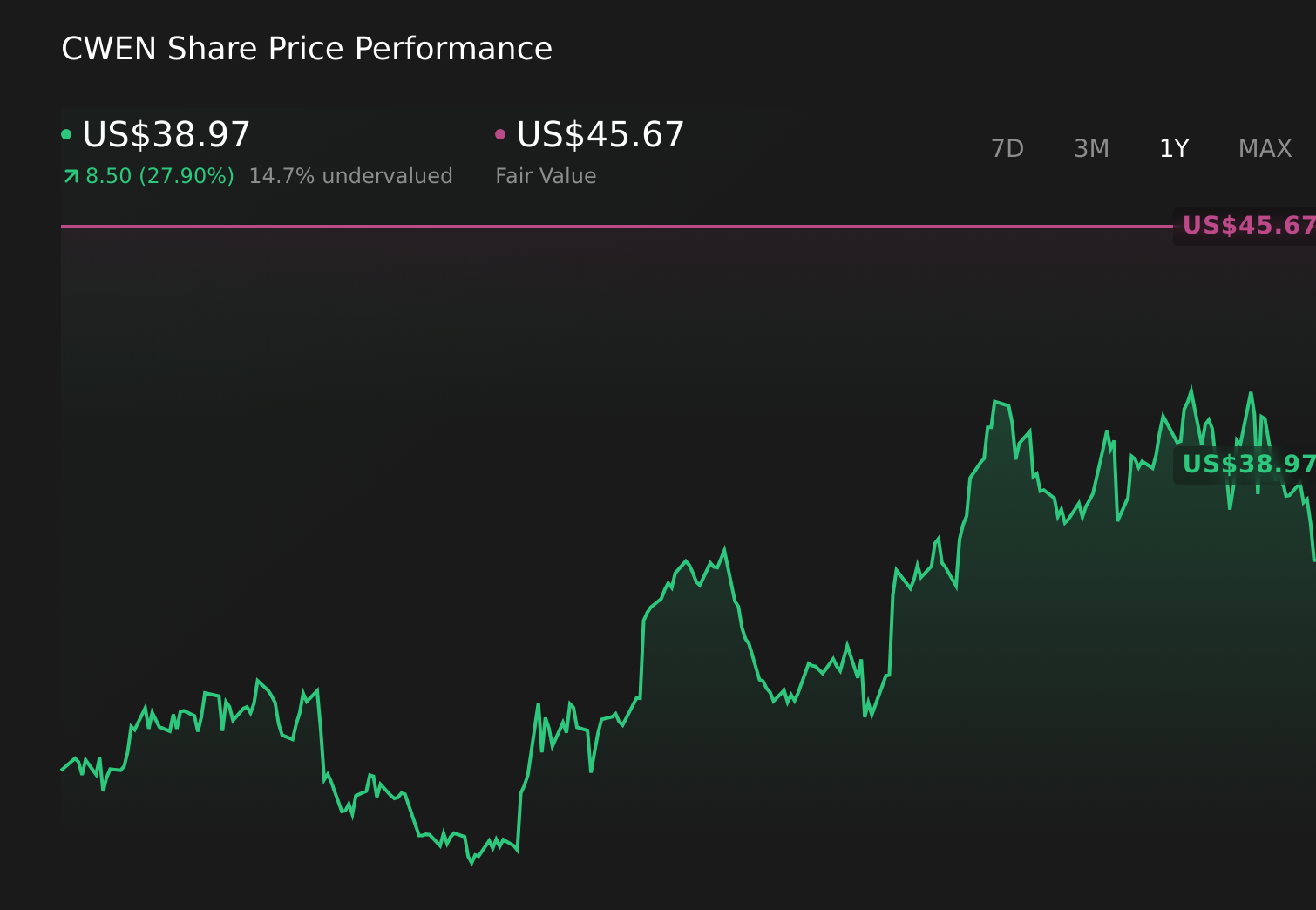

Uncover how Clearway Energy's forecasts yield a $45.67 fair value, a 22% upside to its current price.

Exploring Other Perspectives

Three fair value estimates from the Simply Wall St Community span roughly US$43 to US$129 per share, reflecting very different expectations. As you weigh those views, remember that Clearway’s plan depends heavily on funding multi billion dollar projects at targeted CAFD yields, which has important implications for future cash flows and dividend support.

Explore 3 other fair value estimates on Clearway Energy - why the stock might be worth just $43.09!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Clearway Energy research is our analysis highlighting 2 key rewards and 4 important warning signs that could impact your investment decision.

- Our free Clearway Energy research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Clearway Energy's overall financial health at a glance.

No Opportunity In Clearway Energy?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 28 companies in the world exploring or producing it. Find the list for free.

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com