Watts Water Technologies (WTS) is back in focus after recent analyst upgrades and a Q1 earnings beat highlighted solid organic sales growth, stronger data center demand, and better free cash flow margins.

See our latest analysis for Watts Water Technologies.

Despite the recent Q1 beat and M&A commentary, short term momentum has been mixed, with a 1 day share price return of 1.04% but a 90 day share price return down 9.16%, while the 1 year total shareholder return of 26.62% and 5 year total shareholder return of 129.21% point to stronger long term compounding.

If Watts Water’s performance has you watching infrastructure and building technology trends, it can be useful to widen your search and check out 34 power grid technology and infrastructure stocks

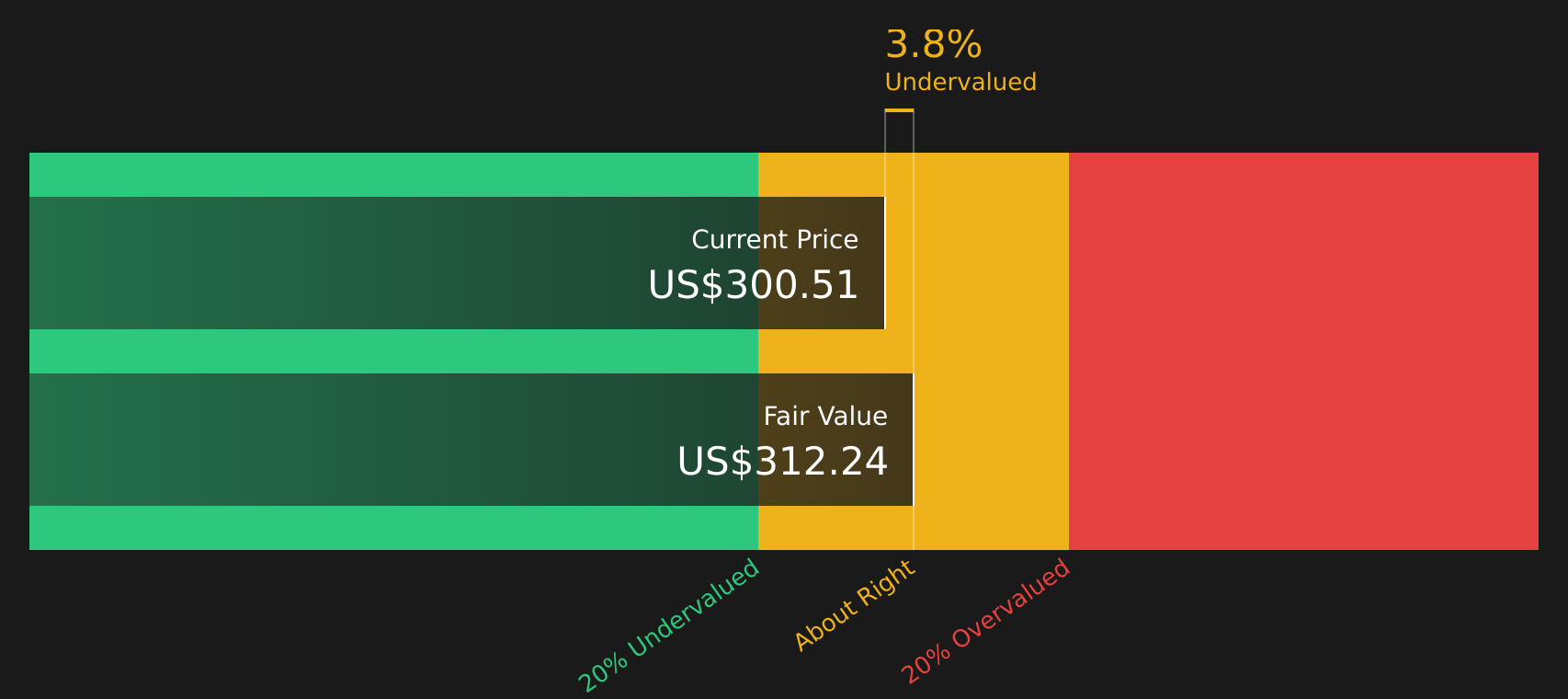

With Watts Water trading at US$299.15 against an analyst price target of US$333.11 and an estimated 4.37% intrinsic discount, investors may ask whether there is still a buying opportunity or whether future growth is already priced in.

Most Popular Narrative: 11% Undervalued

At a last close of $299.15 versus a narrative fair value of $336.11, Watts Water Technologies is framed as undervalued, with that view built on specific growth, margin and valuation assumptions.

The accelerating rollout and success of Nexa, Watts' intelligent water management platform, positions the company to capture the growing demand for advanced, data-driven water conservation, efficiency, and regulatory compliance solutions, expected to drive higher-margin, recurring revenue and support long-term earnings and margin expansion.

Want to see what kind of revenue trajectory, margin profile and future earnings multiple need to line up for that fair value to hold? The story links projected top line growth, fatter profit margins and a premium P/E to justify today’s price gap, but the exact mix of assumptions may surprise you.

Result: Fair Value of $336.11 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, European softness and tariff volatility could pressure volumes and margins and may challenge the idea that current pricing power and earnings assumptions hold up over time.

Find out about the key risks to this Watts Water Technologies narrative.

Another Angle on Valuation

The analyst narrative and our cash flow work suggest Watts Water is trading about 4.4% below an estimated fair value of $312.83, which lines up with the idea of mild undervaluation. That is a relatively small gap, so the real question is whether the cash flow assumptions feel conservative enough for you.

For a closer look at how those cash flows are modeled and discounted in practice, it helps to walk through the SWS DCF model step by step, starting with revenue forecasts and margin assumptions, then checking the terminal value and discount rate choices against your own expectations, Look into how the SWS DCF model arrives at its fair value.

Next Steps

With a mix of potential upside and clear risks across this story, it makes sense to move fast, review the full picture, and weigh the 3 key rewards and 1 important warning sign.

Looking for more investment ideas?

If Watts Water is on your radar, do not stop here. Use the screener to surface fresh opportunities that match your style before the crowd focuses on them.

- Target potential mispricings by scanning for companies that combine quality with value through the 51 high quality undervalued stocks.

- Prioritize resilience by filtering for companies with robust finances using the solid balance sheet and fundamentals stocks screener (46 results).

- Hunt for underfollowed opportunities with strong fundamentals by checking the screener containing 21 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com